You might also like

- Financial Analyst CFA Study Notes: Economics Level 1Document9 pagesFinancial Analyst CFA Study Notes: Economics Level 1Andy Solnik0% (2)

- Ninja Study Plan: The Definitive Guide to Learning, Taking, and Passing the CFA® ExaminationsFrom EverandNinja Study Plan: The Definitive Guide to Learning, Taking, and Passing the CFA® ExaminationsRating: 4 out of 5 stars4/5 (13)

- CFA L1 3 Month ScheduleDocument9 pagesCFA L1 3 Month ScheduleSakura2709No ratings yet

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Cfa Level 2 - Test Bank With SolutionsDocument14 pagesCfa Level 2 - Test Bank With SolutionsAditya BajoriaNo ratings yet

- CFA Level 1 Ethical Standards NotesDocument23 pagesCFA Level 1 Ethical Standards NotesAndy Solnik100% (7)

- Economics for CFA level 1 in just one week: CFA level 1, #4From EverandEconomics for CFA level 1 in just one week: CFA level 1, #4Rating: 4.5 out of 5 stars4.5/5 (2)

- TimePrep Guide For The CFA ExamDocument101 pagesTimePrep Guide For The CFA ExamCris Cris100% (8)

- CFA 2012: Exams L1 : How to Pass the CFA Exams After Studying for Two Weeks Without AnxietyFrom EverandCFA 2012: Exams L1 : How to Pass the CFA Exams After Studying for Two Weeks Without AnxietyRating: 3 out of 5 stars3/5 (2)

- CFA Level 2 FSADocument3 pagesCFA Level 2 FSA素直和夫No ratings yet

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsFrom EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsNo ratings yet

- CFA Level I NotesDocument42 pagesCFA Level I NotesMSA-ACCA100% (6)

- Equity Investment for CFA level 1: CFA level 1, #2From EverandEquity Investment for CFA level 1: CFA level 1, #2Rating: 5 out of 5 stars5/5 (1)

- DA4387 Level I CFA Mock Exam 2018 Morning ADocument37 pagesDA4387 Level I CFA Mock Exam 2018 Morning AAisyah Amatul GhinaNo ratings yet

- Corporate Finance: A Beginner's Guide: Investment series, #1From EverandCorporate Finance: A Beginner's Guide: Investment series, #1No ratings yet

- CFA 2017 Level III - Study Guide Vol 5Document121 pagesCFA 2017 Level III - Study Guide Vol 5Umair Ashraf100% (5)

- Corporate Finance for CFA level 1: CFA level 1, #1From EverandCorporate Finance for CFA level 1: CFA level 1, #1Rating: 3.5 out of 5 stars3.5/5 (3)

- Test Collections CFA-Level-I Question Bank PDFDocument1,568 pagesTest Collections CFA-Level-I Question Bank PDFsaurabh100% (1)

- CFA Level 1 - Section 2 QuantitativeDocument81 pagesCFA Level 1 - Section 2 Quantitativeapi-376313867% (3)

- Free CFA Level 2 Mock Exam (300hours)Document20 pagesFree CFA Level 2 Mock Exam (300hours)ShrutiNo ratings yet

- Cfa Ques AnswerDocument542 pagesCfa Ques AnswerAbid Waheed100% (4)

- Morningstar Guide to Mutual Funds: Five-Star Strategies for SuccessFrom EverandMorningstar Guide to Mutual Funds: Five-Star Strategies for SuccessNo ratings yet

- Cfa Level 2 冲刺班讲义Document100 pagesCfa Level 2 冲刺班讲义Nicholas H. WuNo ratings yet

- SERIES 79 EXAM STUDY GUIDE 2022 + TEST BANKFrom EverandSERIES 79 EXAM STUDY GUIDE 2022 + TEST BANKNo ratings yet

- CFA I Study Plan 12weeksDocument1 pageCFA I Study Plan 12weeksconnectshyamNo ratings yet

- GoStudy - CFA L1 Guided Notes 2018Document545 pagesGoStudy - CFA L1 Guided Notes 2018Mani Manandhar100% (9)

- CFA Level 1Document90 pagesCFA Level 1imran0104100% (2)

- CFA Revision NotesDocument18 pagesCFA Revision NotesklkjlkjlkjlkjlNo ratings yet

- How Do I Prepare For CFA Level 1 in 60 DaysDocument2 pagesHow Do I Prepare For CFA Level 1 in 60 DaysLallan singhNo ratings yet

- CFA Level2 FormulaDocument34 pagesCFA Level2 FormulaRoy Tan100% (3)

- Notes Cfa SummaryDocument336 pagesNotes Cfa SummaryForis Lee33% (3)

- Financial Analyst CFA Study Notes: Quantitative Methods Level 1Document8 pagesFinancial Analyst CFA Study Notes: Quantitative Methods Level 1Andy Solnik33% (3)

- CFA Level 2 Exam Preparation Strategy TipsDocument2 pagesCFA Level 2 Exam Preparation Strategy TipsgregdebickiNo ratings yet

- 2019 CFA Ethics L1-2-3 PDFDocument511 pages2019 CFA Ethics L1-2-3 PDFKathy Ho100% (1)

- CFA Level I - Financial Reporting and Analysis - SMG PDFDocument38 pagesCFA Level I - Financial Reporting and Analysis - SMG PDFFinTree Education Pvt Ltd94% (17)

- Derivatives CfaDocument3 pagesDerivatives CfavNo ratings yet

- CFA Level III FormulaDocument39 pagesCFA Level III Formulammqasmi100% (1)

- CFA Level 2 NotesDocument21 pagesCFA Level 2 NotesFarhan Tariq100% (2)

- CFA Level I Formula SheetDocument27 pagesCFA Level I Formula SheetAnonymous P1xUTHstHT100% (4)

- CFA 2 NotesDocument44 pagesCFA 2 NotesEdmundSiauNo ratings yet

- Financial Analyst CFA Study Notes: Derivatives Level 1Document33 pagesFinancial Analyst CFA Study Notes: Derivatives Level 1Andy Solnik100% (7)

- Free CFA Mind Maps Level 1 - 2015Document18 pagesFree CFA Mind Maps Level 1 - 2015Jaco Greeff100% (6)

- CFA QuestionsDocument42 pagesCFA Questionspuntanalyst100% (2)

- CFA Level 1, June, 2016 - Study PlanDocument3 pagesCFA Level 1, June, 2016 - Study PlanWilliam KentNo ratings yet

- CFA Ethics and Professional Standards EnforcementDocument98 pagesCFA Ethics and Professional Standards EnforcementHongjun Yin92% (12)

- FinTree - FRA Sixty Minute Guide PDFDocument38 pagesFinTree - FRA Sixty Minute Guide PDFkamleshNo ratings yet

- Far Chapter 1Document4 pagesFar Chapter 1Pedro CorreiaNo ratings yet

- Aom AssignmentDocument7 pagesAom AssignmentAkanksha PalNo ratings yet

- Module Fs AnalysisDocument12 pagesModule Fs AnalysisCeejay RoblesNo ratings yet

- LM01 Introduction To Financial Statement Analysis IFT NotesDocument11 pagesLM01 Introduction To Financial Statement Analysis IFT NotesClaptrapjackNo ratings yet

- Financial Statement Analysis for Management DecisionsDocument27 pagesFinancial Statement Analysis for Management DecisionsKitheia Ostrava Reisenchauer100% (1)

- MODULE 1 Lesson 2 and 3Document22 pagesMODULE 1 Lesson 2 and 3Annabeth BrionNo ratings yet

- Financial+Statement++Analysis+Week+4aDocument20 pagesFinancial+Statement++Analysis+Week+4ahezilgonzaga25No ratings yet

- Jann Bushra PDFDocument27 pagesJann Bushra PDFtanvir aliNo ratings yet

- Financial Statement Analysis TechniquesDocument24 pagesFinancial Statement Analysis TechniquesMarjon DimafilisNo ratings yet

- Business Plan PT. Unicom Muda Utama (USD)Document32 pagesBusiness Plan PT. Unicom Muda Utama (USD)Dendy WisanaNo ratings yet

- Plastic Money: An Introduction to Credit and Debit CardsDocument20 pagesPlastic Money: An Introduction to Credit and Debit CardsJeetu VermaNo ratings yet

- AcademyCloudFoundations Module 01Document47 pagesAcademyCloudFoundations Module 01Dhivya rajanNo ratings yet

- Minicase (Chapter 3) Marketing Dịch Vụ: Tên Thành ViênDocument2 pagesMinicase (Chapter 3) Marketing Dịch Vụ: Tên Thành ViênNguyễn Thị Kiều DiễmNo ratings yet

- DDDDDocument7 pagesDDDDShrajith A NatarajanNo ratings yet

- Alm - IciciDocument6 pagesAlm - IciciKhaisarKhaisarNo ratings yet

- ACCTG 102 Practice Sets Quizzes ExamsDocument25 pagesACCTG 102 Practice Sets Quizzes ExamsheythereitsclaireNo ratings yet

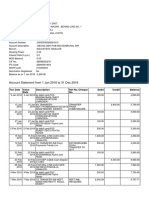

- 20240329-statements-0699-Document8 pages20240329-statements-0699-LuisitoNo ratings yet

- Acct Statement - XX2482 - 04032023 PDFDocument13 pagesAcct Statement - XX2482 - 04032023 PDFKoushik ChakrabortyNo ratings yet

- E-Bill Zuku 2Document2 pagesE-Bill Zuku 2alex67% (3)

- Data Aadt Car 2018Document5 pagesData Aadt Car 2018HUBERT FILOGNo ratings yet

- Financial Reporting and AnalysisDocument50 pagesFinancial Reporting and AnalysisGeorge Shevtsov83% (6)

- Ar 42152: Urban Design StudioDocument14 pagesAr 42152: Urban Design Studiosaurav kumarNo ratings yet

- Computer Network NotesDocument4 pagesComputer Network NotesDevika DakhoreNo ratings yet

- 12969-Cbe Jaipur Exp Third Ac (3A) : Start Date 22-Dec-2023 Arrival 06:45 24-Dec-2023Document1 page12969-Cbe Jaipur Exp Third Ac (3A) : Start Date 22-Dec-2023 Arrival 06:45 24-Dec-2023sharesth sharmaNo ratings yet

- 2018 Accepted Students List Batch 2Document136 pages2018 Accepted Students List Batch 2psiziba6702100% (2)

- Accounts RTP CA Foundation May 2020Document31 pagesAccounts RTP CA Foundation May 2020YashNo ratings yet

- Installation Guide Tata FiberDocument2 pagesInstallation Guide Tata Fiberabhi tNo ratings yet

- Emory Cover Letter1Document1 pageEmory Cover Letter1api-280998981No ratings yet

- Debt Reduction Calculator - Credit Repair Edition: Monthly Payment Initial Snowball StrategyDocument11 pagesDebt Reduction Calculator - Credit Repair Edition: Monthly Payment Initial Snowball StrategyLittlebeeNo ratings yet

- Objectives and Sample QuestionnaireDocument4 pagesObjectives and Sample QuestionnaireShamel MundethNo ratings yet

- L1-History of RadioDocument11 pagesL1-History of RadioTai SankioNo ratings yet

- AcademyCloudArchitecting Module 01Document36 pagesAcademyCloudArchitecting Module 01Kaichun YauNo ratings yet

- Account Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManishDikshitNo ratings yet

- The Communication Media ChannelDocument27 pagesThe Communication Media ChannelElmer Lumague100% (1)

- Statement of Financial Position or Balance SheetDocument3 pagesStatement of Financial Position or Balance SheetLouiseNo ratings yet

- ENTREPRENEURSHIP QUARTER 2 MODULE 11 BusinessimplementationDocument7 pagesENTREPRENEURSHIP QUARTER 2 MODULE 11 Businessimplementationrichard reyesNo ratings yet

- Guest Lecture 3Document3 pagesGuest Lecture 3Jim XieNo ratings yet

- GS - Latin America Internet - E-Commerce - Shopee's Push Into LatAm Ecommerce Expands The Pie Buy SEA, MELI and MGLUDocument24 pagesGS - Latin America Internet - E-Commerce - Shopee's Push Into LatAm Ecommerce Expands The Pie Buy SEA, MELI and MGLURojana ChareonwongsakNo ratings yet

- Czarcie Kopyto®: Purchase Order FormDocument1 pageCzarcie Kopyto®: Purchase Order Formandre nusaNo ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- Electronic Health Records: An Audit and Internal Control GuideFrom EverandElectronic Health Records: An Audit and Internal Control GuideNo ratings yet

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Audit and Assurance Essentials: For Professional Accountancy ExamsFrom EverandAudit and Assurance Essentials: For Professional Accountancy ExamsNo ratings yet

- Lean Auditing: Driving Added Value and Efficiency in Internal AuditFrom EverandLean Auditing: Driving Added Value and Efficiency in Internal AuditRating: 5 out of 5 stars5/5 (1)

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Fraud 101: Techniques and Strategies for Understanding FraudFrom EverandFraud 101: Techniques and Strategies for Understanding FraudNo ratings yet