You might also like

- Measuring Customer Satisfaction - HDFCDocument66 pagesMeasuring Customer Satisfaction - HDFCNaval ChadhaNo ratings yet

- Project Report On Custmer Satisfaction Regarding HDFC BANKDocument68 pagesProject Report On Custmer Satisfaction Regarding HDFC BANKabhi7219No ratings yet

- A Study On Customer SatisfactionDocument89 pagesA Study On Customer SatisfactionAman KhanNo ratings yet

- Summer Internship Report - HDFC Digital BankingDocument32 pagesSummer Internship Report - HDFC Digital BankingMantosh SinghNo ratings yet

- Summer Training HDFC BankDocument98 pagesSummer Training HDFC BankGurpreet Singh100% (1)

- Mobile Banking SynopsisDocument4 pagesMobile Banking Synopsisujwaljaiswal33% (3)

- A Study On Customer Satisfaction HDFC HOJKJDocument79 pagesA Study On Customer Satisfaction HDFC HOJKJsakshi tomarNo ratings yet

- Review of LiteratureDocument4 pagesReview of Literaturemaha lakshmiNo ratings yet

- A Study On Customer Relationship Management Practices in Banking SectorDocument11 pagesA Study On Customer Relationship Management Practices in Banking SectorFathimaNo ratings yet

- Bhavna Gaikwad Project of SbiDocument80 pagesBhavna Gaikwad Project of SbiAkshay BoteNo ratings yet

- Plastic Money Word FileDocument60 pagesPlastic Money Word Fileshah sanket100% (1)

- Ranson Dantis Project Black Book TybmsDocument87 pagesRanson Dantis Project Black Book Tybmsranson dantisNo ratings yet

- "Service Quality of HDFC Bank": Project Report ONDocument75 pages"Service Quality of HDFC Bank": Project Report ONKRISHNANo ratings yet

- HDFC Bank's Plastic Money ReportDocument37 pagesHDFC Bank's Plastic Money ReportankushbabbarbcomNo ratings yet

- Customer Satisfaction of ATM Services inDocument11 pagesCustomer Satisfaction of ATM Services inEswari GkNo ratings yet

- Customer Satisfaction at HDFC BankDocument104 pagesCustomer Satisfaction at HDFC BankAmarkant0% (1)

- "Service Quality of HDFC Bank" AT HDFC Bank Ambala: Final Research Project ReportDocument57 pages"Service Quality of HDFC Bank" AT HDFC Bank Ambala: Final Research Project Reportedward100% (1)

- Service Quality Analysis of SBIDocument38 pagesService Quality Analysis of SBIAkhil BhatiaNo ratings yet

- CRM in Icici BankDocument21 pagesCRM in Icici BankSudil Reddy100% (5)

- Innovation in Banking SectorDocument21 pagesInnovation in Banking Sectoruma2k10No ratings yet

- Himanshu PalDocument71 pagesHimanshu PalChandan SrivastavaNo ratings yet

- THEJASWINI ProjectDocument112 pagesTHEJASWINI Projectswamy yashuNo ratings yet

- CRM in ICICI.Document17 pagesCRM in ICICI.Vicky DaswaniNo ratings yet

- Arkay IndustriesDocument2 pagesArkay IndustriesVishal PandeyNo ratings yet

- HDFC Online BankingDocument24 pagesHDFC Online BankingAmardeep SinghNo ratings yet

- Establishing A Strong Digital FootprintDocument10 pagesEstablishing A Strong Digital FootprintTANVINo ratings yet

- Customer Relationship Management: Group - 3 Anesha Sharma Anurag Mathur Bharat Kalra Mansi Saluja Shashank SharmaDocument8 pagesCustomer Relationship Management: Group - 3 Anesha Sharma Anurag Mathur Bharat Kalra Mansi Saluja Shashank SharmaAnurag MathurNo ratings yet

- CRM Project Word DocumentDocument17 pagesCRM Project Word DocumentMohan Mahato100% (1)

- A Comparative Study On Customer Satisfaction Towards Online Banking Services With Reference To Icici and HDFC Bank in LucknowDocument7 pagesA Comparative Study On Customer Satisfaction Towards Online Banking Services With Reference To Icici and HDFC Bank in LucknowChandan Srivastava100% (1)

- My3 Final Report BSNLDocument38 pagesMy3 Final Report BSNLPavan PaviNo ratings yet

- A Comparative Study On SBI and HDFC in Ambala City Ijariie5997Document11 pagesA Comparative Study On SBI and HDFC in Ambala City Ijariie5997vinayNo ratings yet

- Customer Perception Towards Internet Banking PDFDocument17 pagesCustomer Perception Towards Internet Banking PDFarpita waruleNo ratings yet

- E Banking Consumer BehaviourDocument116 pagesE Banking Consumer Behaviourrevahykrish93No ratings yet

- Icici Bank Case CRMDocument28 pagesIcici Bank Case CRMRohit SemlaniNo ratings yet

- Customer Satisfaction Study at HDFC BankDocument104 pagesCustomer Satisfaction Study at HDFC Bankbb9780No ratings yet

- Comparison of Sbi Yono With Other Banking AppsDocument16 pagesComparison of Sbi Yono With Other Banking AppsgaganpreetNo ratings yet

- Icici Bank: A CRM Project Report ONDocument17 pagesIcici Bank: A CRM Project Report ONSudhir KumarNo ratings yet

- A Study of Credit Cards in Indian ScenarioDocument11 pagesA Study of Credit Cards in Indian ScenarioWifi Internet Cafe & Multi ServicesNo ratings yet

- Corporate Identificatio and Competition Analysis: A Project Report ONDocument77 pagesCorporate Identificatio and Competition Analysis: A Project Report ONmustkeem_qureshi7089No ratings yet

- LRPDocument29 pagesLRPvarshapadiharNo ratings yet

- Customer Relationship Management Is The Strongest and The Most Efficient Approach in Maintaining and Creating Relationships With CustomersDocument2 pagesCustomer Relationship Management Is The Strongest and The Most Efficient Approach in Maintaining and Creating Relationships With CustomersHimanshu YadavNo ratings yet

- Customer Satisfaction with ATM Services in SolanDocument75 pagesCustomer Satisfaction with ATM Services in Solandinesh_v_0076945100% (2)

- Launch Brand Campaign "I am the T in SBIDocument5 pagesLaunch Brand Campaign "I am the T in SBIpraveenaNo ratings yet

- Digitalization and Security of Online Banking in J&K BankDocument80 pagesDigitalization and Security of Online Banking in J&K BankSyed Mehrooj QadriNo ratings yet

- Questionnaire of Bank Account Holder's Satisfaction On Internet BankingDocument5 pagesQuestionnaire of Bank Account Holder's Satisfaction On Internet BankingVikas Vatsyan100% (1)

- ProjectDocument50 pagesProjectPavan KumarNo ratings yet

- Black Book ProjectDocument23 pagesBlack Book ProjectAtharv KoyandeNo ratings yet

- Summer Training Project ReportDocument66 pagesSummer Training Project ReportJimmy GoelNo ratings yet

- Customer Loan Preferences at Co-op BanksDocument13 pagesCustomer Loan Preferences at Co-op BanksAJAY SHAHNo ratings yet

- Summer Training Report Trends and Practices of HDFC Bank:-Retail Abnking Conducted at HDFC BANK, Ambala CityDocument104 pagesSummer Training Report Trends and Practices of HDFC Bank:-Retail Abnking Conducted at HDFC BANK, Ambala Cityjs60564No ratings yet

- Mumbai University BBI SyllabusDocument3 pagesMumbai University BBI Syllabussameer_kiniNo ratings yet

- Research ProposalDocument3 pagesResearch ProposalAniket GangurdeNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- HDFC BankDocument79 pagesHDFC BankAnkit YadavNo ratings yet

- SynopsisDocument11 pagesSynopsiskrishna bajait100% (1)

- A Study On Level of Customer Satisfaction Towards Maruti Suzuki Baleno in Lucknow CityDocument104 pagesA Study On Level of Customer Satisfaction Towards Maruti Suzuki Baleno in Lucknow CityHarshit KashyapNo ratings yet

- Fyp-importance-Aspects-overall Satisfaction - Buying Behavior and LoyaltyDocument98 pagesFyp-importance-Aspects-overall Satisfaction - Buying Behavior and LoyaltyMelissa HewNo ratings yet

- Axis Bank - FINANCIAL OVERVIEW OF AXIS BANK & COMPARATIVE STUDY OF CURRENT ACCOUNT AND SAVING ACCDocument93 pagesAxis Bank - FINANCIAL OVERVIEW OF AXIS BANK & COMPARATIVE STUDY OF CURRENT ACCOUNT AND SAVING ACCAmol Sinha56% (9)

- Jaffar and Musa (2013) PDFDocument10 pagesJaffar and Musa (2013) PDFMohamed FAKHFEKHNo ratings yet

- SEPCODocument84 pagesSEPCOAvijoy GuptaNo ratings yet

- Maintain Data Origin TypeDocument6 pagesMaintain Data Origin Typeshiva_1912-1No ratings yet

- Cs White Paper Family Office Dynamic Pathway To Successful Family and Wealth Management Part 2 - enDocument36 pagesCs White Paper Family Office Dynamic Pathway To Successful Family and Wealth Management Part 2 - enKrishna PrasadNo ratings yet

- 23 RD Jan 17 Synergies Dooray AutomativeDocument6 pages23 RD Jan 17 Synergies Dooray AutomativeTarun ParasharNo ratings yet

- Nomad Capitalist Free Guide Banking PDFDocument11 pagesNomad Capitalist Free Guide Banking PDFnsajkoviNo ratings yet

- TAX of PinalizeDocument19 pagesTAX of PinalizeDennis IsananNo ratings yet

- Oct 3rd Week Details (Eng) by AffairsCloudDocument27 pagesOct 3rd Week Details (Eng) by AffairsCloudAniket ZunkeNo ratings yet

- Municipal BondDocument5 pagesMunicipal Bondashish_20kNo ratings yet

- A12 - KolkataDocument2 pagesA12 - KolkataVbs ReddyNo ratings yet

- R. E. L. Finley v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Jerline Dick Finley, 255 F.2d 128, 10th Cir. (1958)Document9 pagesR. E. L. Finley v. Commissioner of Internal Revenue, Commissioner of Internal Revenue v. Jerline Dick Finley, 255 F.2d 128, 10th Cir. (1958)Scribd Government DocsNo ratings yet

- Appsc CBRT Aee Mains 1st Feb 2017 Shift 1Document21 pagesAppsc CBRT Aee Mains 1st Feb 2017 Shift 1Charan ReddyNo ratings yet

- BLCTE - MOCK EXAM I Updated With Answer Key PDFDocument27 pagesBLCTE - MOCK EXAM I Updated With Answer Key PDFmcnavarro100% (2)

- CLTD - Training - Quiz Questions - Module 1 - DoneDocument32 pagesCLTD - Training - Quiz Questions - Module 1 - DoneTringa0% (1)

- The Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07Document2 pagesThe Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07akasaka99No ratings yet

- Error Correction (Part 2) - Suspense Accounts (Including RQS)Document6 pagesError Correction (Part 2) - Suspense Accounts (Including RQS)King JulianNo ratings yet

- Case Study MMDocument4 pagesCase Study MMMehdi TaseerNo ratings yet

- Eurobonds: Euro BondsDocument5 pagesEurobonds: Euro BondssuperjagdishNo ratings yet

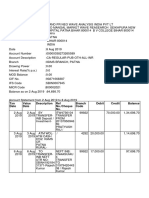

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- Philippine Taxation History and SystemDocument58 pagesPhilippine Taxation History and SystemThea MallariNo ratings yet

- Valuation Workbook QuestionsDocument200 pagesValuation Workbook QuestionsAugusto César0% (1)

- 02 Phi LarpDocument133 pages02 Phi LarpSteven Joseph IncioNo ratings yet

- Manoj Maheshrao Khandare Project ReportDocument40 pagesManoj Maheshrao Khandare Project Reportshubham moonNo ratings yet

- Aeropostale Checkout ConfirmationDocument3 pagesAeropostale Checkout ConfirmationBladimilPujOlsChalasNo ratings yet

- Accounting Principles Question Paper, Answers and Examiners CommentsDocument24 pagesAccounting Principles Question Paper, Answers and Examiners CommentsRyanNo ratings yet

- Change Management EssayDocument5 pagesChange Management EssayAvinashNo ratings yet

- Induction Training Report - Planning Division: AcknowledgementDocument44 pagesInduction Training Report - Planning Division: AcknowledgementasamselaseNo ratings yet

- 9 Factors To Consider When Comparing McKinsey - Bain - BCG - Management ConsultedDocument7 pages9 Factors To Consider When Comparing McKinsey - Bain - BCG - Management ConsultedTarekNo ratings yet