You might also like

- Income Taxation Chapter on Compensation IncomeDocument17 pagesIncome Taxation Chapter on Compensation IncomeSheilamae Sernadilla GregorioNo ratings yet

- Ramo 1-98Document8 pagesRamo 1-98abi_demdamNo ratings yet

- Ramo 1-2019Document74 pagesRamo 1-2019Donato Vergara IIINo ratings yet

- TO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedDocument4 pagesTO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedLudica OjaNo ratings yet

- (2015) 55 Taxmann - Com 40 (Article) Demystifying The Indian Advance Pricing Agreement ProgramDocument10 pages(2015) 55 Taxmann - Com 40 (Article) Demystifying The Indian Advance Pricing Agreement Programsuraj gulipalliNo ratings yet

- RR 2-2013 PDFDocument23 pagesRR 2-2013 PDFnaldsdomingoNo ratings yet

- Article TPDocument3 pagesArticle TPpawanagrawal83No ratings yet

- Transfer Pricing Audit Guidelines, Revenue Audit Memorandum Order No. 001-19, (August 20, 2019) PDFDocument49 pagesTransfer Pricing Audit Guidelines, Revenue Audit Memorandum Order No. 001-19, (August 20, 2019) PDFKriszan ManiponNo ratings yet

- Managing TransferPricing Risk in ChinaDocument3 pagesManaging TransferPricing Risk in ChinadreampursuerNo ratings yet

- 49.transfer PricingDocument4 pages49.transfer PricingmercatuzNo ratings yet

- Transfer PricingDocument13 pagesTransfer PricingRaj Kumar Chakraborty100% (2)

- Transfer Pricing:: Governments Are Tightening Transfer Pricing Regulations and Strengthening Enforcement in OrderDocument2 pagesTransfer Pricing:: Governments Are Tightening Transfer Pricing Regulations and Strengthening Enforcement in OrderzaniNo ratings yet

- Transfer PricingDocument47 pagesTransfer Pricingkanabaramit100% (2)

- Tax Practitioners: Advocates of Compliance or Avoidance?: Conference PaperDocument23 pagesTax Practitioners: Advocates of Compliance or Avoidance?: Conference PaperKristy Dela CernaNo ratings yet

- International Transfer PricingDocument21 pagesInternational Transfer PricingAtia IbnatNo ratings yet

- Minimize Tax Risk With Transfer Pricing StrategiesDocument5 pagesMinimize Tax Risk With Transfer Pricing Strategiesstuddude88No ratings yet

- VodafoneDocument5 pagesVodafoneSash Dhoni7No ratings yet

- Related Party TransactionDocument3 pagesRelated Party TransactionzaniNo ratings yet

- Philippines Transfer Pricing RulesDocument5 pagesPhilippines Transfer Pricing RulesJade BautistaNo ratings yet

- Acct391 Ep3Document3 pagesAcct391 Ep3arijana.dulovicNo ratings yet

- New Focus on Transfer Pricing in IndiaDocument9 pagesNew Focus on Transfer Pricing in IndiaPareshBhangaleNo ratings yet

- pricing regulationDocument3 pagespricing regulationagubamamarvelousNo ratings yet

- Transfer Pricing Regulations Take Off in GhanaDocument5 pagesTransfer Pricing Regulations Take Off in GhanafbuameNo ratings yet

- Due Diligence-Tax Due DilDocument4 pagesDue Diligence-Tax Due DilEljoe VinluanNo ratings yet

- Discussion Draft Transfer Pricing DocumentationDocument21 pagesDiscussion Draft Transfer Pricing DocumentationCA Sagar WaghNo ratings yet

- India: Type of Transactions CoveredDocument27 pagesIndia: Type of Transactions CoveredPadmanabha NarayanNo ratings yet

- Literature Review TAXDocument5 pagesLiterature Review TAXSucheta SahaNo ratings yet

- Transfer Pricing' - An International Taxation Issue Concerning The Balance of Interest Between The Tax Payer and Tax AdministratorDocument8 pagesTransfer Pricing' - An International Taxation Issue Concerning The Balance of Interest Between The Tax Payer and Tax AdministratorchristianNo ratings yet

- TP Rules BaladadDocument3 pagesTP Rules BaladadJomel ManaigNo ratings yet

- Best Practices For Maintaining Compliance With Evolving Tax and Regulatory RequirementsDocument5 pagesBest Practices For Maintaining Compliance With Evolving Tax and Regulatory RequirementsJoshua OmacheNo ratings yet

- IFRS-Basic Principles, Assumptions, Importance, Advantages and DisadvantagesDocument32 pagesIFRS-Basic Principles, Assumptions, Importance, Advantages and DisadvantagesPRINCESS PlayZNo ratings yet

- Fin 48 Tax Penalty StandardDocument9 pagesFin 48 Tax Penalty StandardEduardo Fernandes ArandasNo ratings yet

- PH TP Audit GuidelinesDocument3 pagesPH TP Audit GuidelinesClarence Joy Amistoso OlaritaNo ratings yet

- EY Transfer Pricing Global Reference Guide 2013Document236 pagesEY Transfer Pricing Global Reference Guide 2013davidwijaya1986No ratings yet

- OECD Discussion Draft Implementation Guidance On HTVIDocument8 pagesOECD Discussion Draft Implementation Guidance On HTVIMario AlfaroNo ratings yet

- IFRS Adoption in Nigeria - Tax ImplicationsDocument33 pagesIFRS Adoption in Nigeria - Tax ImplicationsEjiemen OkunegaNo ratings yet

- Key Words: Compliance, Enforcement, Compliance ProgramDocument12 pagesKey Words: Compliance, Enforcement, Compliance ProgramawokedeNo ratings yet

- Chapter 9Document19 pagesChapter 9Nigussie BerhanuNo ratings yet

- Transfer Pricing: Headache To Corporate Governance : AbstractDocument5 pagesTransfer Pricing: Headache To Corporate Governance : AbstractShelviDyanPrastiwiNo ratings yet

- Uae Corporate Tax Transfer Pricing GuideDocument7 pagesUae Corporate Tax Transfer Pricing GuideMuhammad UmarNo ratings yet

- Babcock University Acct 534 Lecture 5 Transfer PricingDocument28 pagesBabcock University Acct 534 Lecture 5 Transfer Pricingamehdebby1410No ratings yet

- Income Tax (TP) Regulation Presentation Slide For InductionDocument41 pagesIncome Tax (TP) Regulation Presentation Slide For InductionUmar AbdulkabirNo ratings yet

- Due Diligence-Tax Due Dil - FinalDocument6 pagesDue Diligence-Tax Due Dil - FinalEljoe VinluanNo ratings yet

- Aktin PresentDocument12 pagesAktin PresentErin SinagaNo ratings yet

- Transfer Pricing authority tax law MalaysiaDocument9 pagesTransfer Pricing authority tax law MalaysiaazshamNo ratings yet

- TaxFlash 2011 01.unlockedDocument7 pagesTaxFlash 2011 01.unlockedDamian DeoNo ratings yet

- What Is Transfer Pricing PolicyDocument18 pagesWhat Is Transfer Pricing Policybinnykaur100% (1)

- M1 TaxmanDocument13 pagesM1 TaxmanIris GamiaoNo ratings yet

- FRS 18, Accounting PoliciesDocument8 pagesFRS 18, Accounting PoliciesveemaswNo ratings yet

- Mas Research PaperDocument7 pagesMas Research Paperdiane camansagNo ratings yet

- United Arab Emirates - Corporate - Group TaxationDocument5 pagesUnited Arab Emirates - Corporate - Group TaxationMuhammad UmarNo ratings yet

- Tax Bites September 2010Document2 pagesTax Bites September 2010JayjayNo ratings yet

- TransferpricingDocument24 pagesTransferpricingollieNo ratings yet

- Global Transfer Pricing Review: PanamaDocument5 pagesGlobal Transfer Pricing Review: PanamaCharu SinghNo ratings yet

- Profits Tax IX Transfer PricingDocument49 pagesProfits Tax IX Transfer Pricinggary_nggNo ratings yet

- Impact of Transfer Pricing On Tax PlanningDocument5 pagesImpact of Transfer Pricing On Tax PlanningDaisy AnitaNo ratings yet

- Critical Impact and Analysis of Action Plan 12 On India's Tax Regime: Mandatory Disclosure StandardsDocument6 pagesCritical Impact and Analysis of Action Plan 12 On India's Tax Regime: Mandatory Disclosure StandardsKunwarbir Singh lohatNo ratings yet

- International TP Handbook 2011Document0 pagesInternational TP Handbook 2011Kolawole AkinmojiNo ratings yet

- Itp 2015 2016 Final PDFDocument1,162 pagesItp 2015 2016 Final PDFht1234222No ratings yet

- Basics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.From EverandBasics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.No ratings yet

- Group 3 - History of Science (Reflection)Document7 pagesGroup 3 - History of Science (Reflection)Jayson Berja de LeonNo ratings yet

- Pupsmbaai Non - Stock - Articles - of - IncorporationDocument6 pagesPupsmbaai Non - Stock - Articles - of - IncorporationJayson Berja de LeonNo ratings yet

- Despabiladeras, Jelo (Reflection)Document1 pageDespabiladeras, Jelo (Reflection)Jayson Berja de LeonNo ratings yet

- Pupsmbaai Non - Stock - Articles - of - IncorporationDocument6 pagesPupsmbaai Non - Stock - Articles - of - IncorporationJayson Berja de LeonNo ratings yet

- Cruz, Aiyanna Gabrielle (Reflection)Document1 pageCruz, Aiyanna Gabrielle (Reflection)Jayson Berja de LeonNo ratings yet

- Microsoft Dynamics 365 For Property Management ScriptDocument4 pagesMicrosoft Dynamics 365 For Property Management ScriptJayson Berja de LeonNo ratings yet

- YAYADocument2 pagesYAYAJayson Berja de LeonNo ratings yet

- De Leon, Misha Laine (Reflection)Document1 pageDe Leon, Misha Laine (Reflection)Jayson Berja de LeonNo ratings yet

- July 2020 - ACCTG CEP 24362280Document2 pagesJuly 2020 - ACCTG CEP 24362280Jayson Berja de LeonNo ratings yet

- DelRosario, Kenneth (Reflection)Document1 pageDelRosario, Kenneth (Reflection)Jayson Berja de LeonNo ratings yet

- Microsoft Dynamics 365 For Property Management ScriptDocument4 pagesMicrosoft Dynamics 365 For Property Management ScriptJayson Berja de LeonNo ratings yet

- DE LEON, MISHA LAINE (Activity)Document7 pagesDE LEON, MISHA LAINE (Activity)Jayson Berja de LeonNo ratings yet

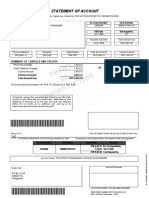

- Statement of Account: Summary of Charges and CreditsDocument4 pagesStatement of Account: Summary of Charges and CreditsJayson Berja de LeonNo ratings yet

- Setting up Eight Work AreasDocument2 pagesSetting up Eight Work AreasJayson Berja de LeonNo ratings yet

- July 2020 - ACCTG CEP 24362280Document2 pagesJuly 2020 - ACCTG CEP 24362280Jayson Berja de LeonNo ratings yet

- July 2020 - ACCTG CEP 24362280Document2 pagesJuly 2020 - ACCTG CEP 24362280Jayson Berja de LeonNo ratings yet

- Cronus International Ltd. Coolwood TechnologiesDocument1 pageCronus International Ltd. Coolwood TechnologiesJayson Berja de LeonNo ratings yet

- July 2020 - ACCTG CEP 24362280Document2 pagesJuly 2020 - ACCTG CEP 24362280Jayson Berja de LeonNo ratings yet

- INVOICE I-99999: CRONUS International Ltd. 5 The Ring Westminster W2 8HG London Electronics LTDDocument1 pageINVOICE I-99999: CRONUS International Ltd. 5 The Ring Westminster W2 8HG London Electronics LTDJayson Berja de LeonNo ratings yet

- Statement of Account: 688329167 09-Jul-2020 2,998.00 PDocument2 pagesStatement of Account: 688329167 09-Jul-2020 2,998.00 PJayson Berja de LeonNo ratings yet

- Certificate of Employment: To Whom It May ConcernDocument1 pageCertificate of Employment: To Whom It May ConcernJayson Berja de Leon0% (1)

- CRONUS International Ltd. warehouse restructure planning invoiceDocument1 pageCRONUS International Ltd. warehouse restructure planning invoiceJayson Berja de LeonNo ratings yet

- CRONUS International LTDDocument1 pageCRONUS International LTDJayson Berja de LeonNo ratings yet

- CRONUS International Ltd Invoice I-77777 to Electronics LtdDocument1 pageCRONUS International Ltd Invoice I-77777 to Electronics LtdJayson Berja de LeonNo ratings yet

- CRONUS International Ltd. 5 The Ring Westminster W2 8HG LondonDocument1 pageCRONUS International Ltd. 5 The Ring Westminster W2 8HG LondonJayson Berja de LeonNo ratings yet

- CRONUS International LTDDocument1 pageCRONUS International LTDJayson Berja de LeonNo ratings yet

- CRONUS International Ltd Invoice I-88888Document1 pageCRONUS International Ltd Invoice I-88888Jayson Berja de LeonNo ratings yet

- Turnover - DennisDocument16 pagesTurnover - DennisJayson Berja de LeonNo ratings yet

- BOOKSPH Scholarship Registration (1-466)Document51 pagesBOOKSPH Scholarship Registration (1-466)Jayson Berja de LeonNo ratings yet

- Mtap by SkillDocument10 pagesMtap by SkillJulie IsmaelNo ratings yet

- Jurnal PajakDocument43 pagesJurnal PajakIndahNo ratings yet

- Myvhi Policy Document 29976414Document3 pagesMyvhi Policy Document 29976414pat oneillNo ratings yet

- Tax Clearance Certificate RequirementsDocument2 pagesTax Clearance Certificate RequirementsKamaraj NatarajanNo ratings yet

- Naib Tehsildaar HPSC Answer Key 2019Document4 pagesNaib Tehsildaar HPSC Answer Key 2019Ravinder YadavNo ratings yet

- Module 3 PDFDocument16 pagesModule 3 PDFJennifer AdvientoNo ratings yet

- US Internal Revenue Service: p3381Document3 pagesUS Internal Revenue Service: p3381IRSNo ratings yet

- "Foreign Currency Deposit Unit" or "FCDU" Shall Refer To That Unit of A Local BankDocument3 pages"Foreign Currency Deposit Unit" or "FCDU" Shall Refer To That Unit of A Local Bankalimoya13No ratings yet

- Income Tax Law - Basic Concepts For B.com 3rd SemesterDocument12 pagesIncome Tax Law - Basic Concepts For B.com 3rd SemesterBharat GaikwadNo ratings yet

- Capital Gains Tax Return BIR Form No 1706Document1 pageCapital Gains Tax Return BIR Form No 1706NGITPANo ratings yet

- Fiscal AdministrationDocument34 pagesFiscal AdministrationRaymond Besorio GadaisNo ratings yet

- Chapter 4Document11 pagesChapter 4yosef mechalNo ratings yet

- Subject To Kolkata Jurisdication - 3 PDFDocument1 pageSubject To Kolkata Jurisdication - 3 PDFD CostaNo ratings yet

- Taxation Powerpoint ShengDocument17 pagesTaxation Powerpoint ShengannabelNo ratings yet

- VAT Guide: Rates, Returns, Filing ProceduresDocument33 pagesVAT Guide: Rates, Returns, Filing ProceduresvicsNo ratings yet

- What Is Public FinanceDocument5 pagesWhat Is Public FinanceanneNo ratings yet

- CIR v. LA TONDENADocument1 pageCIR v. LA TONDENAMyrahNo ratings yet

- Taxation 1Document11 pagesTaxation 1graciaNo ratings yet

- Final Notice Real Property TaxDocument4 pagesFinal Notice Real Property TaxJanMichaelSuanColladoNo ratings yet

- Surfside Beach PPP DataDocument4 pagesSurfside Beach PPP DataWMBF NewsNo ratings yet

- Partnership OperationsDocument4 pagesPartnership OperationsApple Joy YutaNo ratings yet

- May 2023 PayslipDocument1 pageMay 2023 Payslipdorcas baduNo ratings yet

- FATCA Presentation - KhaledDocument42 pagesFATCA Presentation - KhaledMd.Aminul Islam BhuiyanNo ratings yet

- SHORT ANSWERS ChaurasiaDocument22 pagesSHORT ANSWERS ChaurasiaSatvik MishraNo ratings yet

- Taxmannsfinanceact 2023 IncometaxpublicationcompDocument32 pagesTaxmannsfinanceact 2023 Incometaxpublicationcompmirzapur.upsarkarNo ratings yet

- Indirect Taxation (Section B) : The Institute of Cost Accountants of IndiaDocument344 pagesIndirect Taxation (Section B) : The Institute of Cost Accountants of IndiaSagar Verma100% (1)

- Mahendra Patil AckDocument6 pagesMahendra Patil AckMahendra PatilNo ratings yet

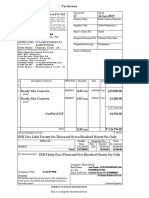

- Tax Invoice for Ready Mix ConcreteDocument1 pageTax Invoice for Ready Mix ConcreteFSPL HSENo ratings yet

- AFA1-3C - Assignment 2Document10 pagesAFA1-3C - Assignment 2Segarambal MasilamoneyNo ratings yet

- G.R. No. L-19727Document14 pagesG.R. No. L-19727Amicus CuriaeNo ratings yet