You might also like

- Consolidated Accounts June-2011Document17 pagesConsolidated Accounts June-2011Syed Aoun MuhammadNo ratings yet

- Consolidated First Page To 11.2 Property and EquipmentDocument18 pagesConsolidated First Page To 11.2 Property and EquipmentAsif_Ali_1564No ratings yet

- MCB Bank Limited Consolidated Financial Statements SummaryDocument93 pagesMCB Bank Limited Consolidated Financial Statements SummaryUmair NasirNo ratings yet

- MCB Consolidated For Year Ended Dec 2011Document87 pagesMCB Consolidated For Year Ended Dec 2011shoaibjeeNo ratings yet

- Summit Bank Annual Report 2012Document200 pagesSummit Bank Annual Report 2012AAqsam0% (1)

- Desco Final Account AnalysisDocument26 pagesDesco Final Account AnalysiskmsakibNo ratings yet

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Document32 pages4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiNo ratings yet

- Balance Sheet2006Document50 pagesBalance Sheet2006malikzai777No ratings yet

- 2010Document51 pages2010Mahmood KhanNo ratings yet

- 2011 Consolidated All SamsungDocument43 pages2011 Consolidated All SamsungGurpreet Singh SainiNo ratings yet

- United Bank Limited: Consolidated Condensed Interim Financial StatementsDocument19 pagesUnited Bank Limited: Consolidated Condensed Interim Financial StatementsMuhammad HassanNo ratings yet

- Vertical and Horizontal Analysis of PidiliteDocument12 pagesVertical and Horizontal Analysis of PidiliteAnuj AgarwalNo ratings yet

- Ar 11 pt03Document112 pagesAr 11 pt03Muneeb ShahidNo ratings yet

- Analyze Dell's FinancialsDocument18 pagesAnalyze Dell's FinancialsSaema JessyNo ratings yet

- Myer AR10 Financial ReportDocument50 pagesMyer AR10 Financial ReportMitchell HughesNo ratings yet

- National Bank of Pakistan: Standalone Financial Statements For The Quarter Ended September 30, 2010Document36 pagesNational Bank of Pakistan: Standalone Financial Statements For The Quarter Ended September 30, 2010Ghulam AkbarNo ratings yet

- Financial StatementDocument115 pagesFinancial Statementammar123No ratings yet

- ZTBL 2008Document62 pagesZTBL 2008Mahmood KhanNo ratings yet

- Bank's Annual Balance Sheets and Income StatementsDocument6 pagesBank's Annual Balance Sheets and Income StatementsHassaan AhmadNo ratings yet

- TCS Ifrs Q3 13 Usd PDFDocument23 pagesTCS Ifrs Q3 13 Usd PDFSubhasish GoswamiNo ratings yet

- ICI Pakistan Limited: Balance SheetDocument28 pagesICI Pakistan Limited: Balance SheetArsalan KhanNo ratings yet

- Assets: Balance Sheet 2009 2010Document21 pagesAssets: Balance Sheet 2009 2010raohasanNo ratings yet

- Auditors' Report To The MembersDocument59 pagesAuditors' Report To The MembersAleem BayarNo ratings yet

- Six Years Financial SummaryDocument133 pagesSix Years Financial Summarywaqas_haider_1No ratings yet

- Al-Noor Sugar Mills Limited: Balance Sheet As at 31St December, 2006Document6 pagesAl-Noor Sugar Mills Limited: Balance Sheet As at 31St December, 2006Umair KhanNo ratings yet

- Chap-6 Financial AnalysisDocument15 pagesChap-6 Financial Analysis✬ SHANZA MALIK ✬No ratings yet

- Ual Jun2011Document10 pagesUal Jun2011asankajNo ratings yet

- 1.accounts 2012 AcnabinDocument66 pages1.accounts 2012 AcnabinArman Hossain WarsiNo ratings yet

- Final Accounts 2005Document44 pagesFinal Accounts 2005Mahmood KhanNo ratings yet

- Assignment: Topic: Financial Statement Analysis of National Bank of PakistanDocument28 pagesAssignment: Topic: Financial Statement Analysis of National Bank of PakistanSadaf AliNo ratings yet

- ASX Appendix 4E Results For Announcement To The Market: Ilh Group LimitedDocument14 pagesASX Appendix 4E Results For Announcement To The Market: Ilh Group LimitedASX:ILH (ILH Group)No ratings yet

- Infosys Balance SheetDocument28 pagesInfosys Balance SheetMM_AKSINo ratings yet

- Infosys Consolidated Financial Statements ReviewDocument13 pagesInfosys Consolidated Financial Statements ReviewLalith RajuNo ratings yet

- JansevaDocument21 pagesJansevaHarshil KoushikNo ratings yet

- System LimitedDocument11 pagesSystem LimitedNabeel AhmadNo ratings yet

- Profit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Document11 pagesProfit and Loss Account For The Year Ended March 31, 2010: Column1 Column2Karishma JaisinghaniNo ratings yet

- Company Name HBL Annual Data FY 2009 Quarter Figures 000: Mark-Up / Return / Interest EarnedDocument6 pagesCompany Name HBL Annual Data FY 2009 Quarter Figures 000: Mark-Up / Return / Interest EarnedCherry SprinkleNo ratings yet

- Consolidated Accounts December 31 2011 For Web (Revised) PDFDocument93 pagesConsolidated Accounts December 31 2011 For Web (Revised) PDFElegant EmeraldNo ratings yet

- Negros Navigation Co., Inc. and SubsidiariesDocument48 pagesNegros Navigation Co., Inc. and SubsidiarieskgaviolaNo ratings yet

- Notes SAR'000 (Unaudited) 14,482,456 6,998,836 34,094,654 115,286,635 399,756 411,761 1,749,778 3,671,357Document10 pagesNotes SAR'000 (Unaudited) 14,482,456 6,998,836 34,094,654 115,286,635 399,756 411,761 1,749,778 3,671,357Arafath CholasseryNo ratings yet

- USD $ in MillionsDocument8 pagesUSD $ in MillionsAnkita ShettyNo ratings yet

- Banking System of Japan Financial DataDocument44 pagesBanking System of Japan Financial Datapsu0168No ratings yet

- Accounts AssignmentDocument7 pagesAccounts AssignmentHari PrasaadhNo ratings yet

- ConsolidatedReport08 (BAHL)Document87 pagesConsolidatedReport08 (BAHL)Muhammad UsmanNo ratings yet

- NTB - 1H2013 Earnings Note - BUY - 27 August 2013Document4 pagesNTB - 1H2013 Earnings Note - BUY - 27 August 2013Randora LkNo ratings yet

- Financial Statements For The Year Ended 31 December 2009Document64 pagesFinancial Statements For The Year Ended 31 December 2009AyeshaJangdaNo ratings yet

- Financial Report H1 2009 enDocument27 pagesFinancial Report H1 2009 eniramkkNo ratings yet

- Pyrogenesis Canada Inc.: Financial StatementsDocument43 pagesPyrogenesis Canada Inc.: Financial StatementsJing SunNo ratings yet

- Balance sheet and cash flow analysisDocument1,832 pagesBalance sheet and cash flow analysisjadhavshankar100% (1)

- HKSE Announcement of 2011 ResultsDocument29 pagesHKSE Announcement of 2011 ResultsHenry KwongNo ratings yet

- Wipro Financial StatementsDocument37 pagesWipro Financial StatementssumitpankajNo ratings yet

- FS Final March31 2009Document29 pagesFS Final March31 2009beehajiNo ratings yet

- Cash Flow Statement: For The Year Ended March 31, 2013Document2 pagesCash Flow Statement: For The Year Ended March 31, 2013malynellaNo ratings yet

- 4.JBSL AccountsDocument8 pages4.JBSL AccountsArman Hossain WarsiNo ratings yet

- Balance Sheet: Lending To Financial InstitutionsDocument10 pagesBalance Sheet: Lending To Financial InstitutionsAlonewith BrokenheartNo ratings yet

- Hyundai Motor Company Financial Statements and Auditors' Report 2011-2010Document65 pagesHyundai Motor Company Financial Statements and Auditors' Report 2011-2010ৰিতুপর্ণ HazarikaNo ratings yet

- Ratio CalculationsDocument59 pagesRatio CalculationsMayesha MehnazNo ratings yet

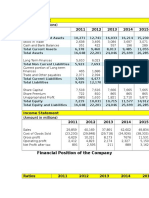

- Financial Position of The Engro FoodsDocument2 pagesFinancial Position of The Engro FoodsJaveriarehanNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Corporate Governance and Firm PerformanceDocument21 pagesCorporate Governance and Firm PerformanceJamal GillNo ratings yet

- HR Analysis of HBLDocument15 pagesHR Analysis of HBLMuhammad tahir100% (1)

- Levying of Additional Development ChargesDocument1 pageLevying of Additional Development ChargesJamal GillNo ratings yet

- Corporate Governance and Firm PerformanceDocument21 pagesCorporate Governance and Firm PerformanceJamal GillNo ratings yet

- Currency exchange calculatorDocument3 pagesCurrency exchange calculatorJamal GillNo ratings yet

- ResignationDocument1 pageResignationJamal GillNo ratings yet

- Service Manual: Wireless Type ModelsDocument24 pagesService Manual: Wireless Type ModelsJamal GillNo ratings yet

- Research Question:: Status of IT Use in Retail Sector of Pakistan: Problems and PossibilitiesDocument12 pagesResearch Question:: Status of IT Use in Retail Sector of Pakistan: Problems and PossibilitiesJamal GillNo ratings yet

- Interest RateDocument2 pagesInterest RateJamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- Certificate of Internship: Ref No. 316/14 Date: 07/09/14Document1 pageCertificate of Internship: Ref No. 316/14 Date: 07/09/14Jamal GillNo ratings yet

- Research Question:: Status of IT Use in Retail Sector of Pakistan: Problems and PossibilitiesDocument12 pagesResearch Question:: Status of IT Use in Retail Sector of Pakistan: Problems and PossibilitiesJamal GillNo ratings yet

- Advt - No - 10-2013Document6 pagesAdvt - No - 10-2013Jamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- Jamal Gill CVDocument2 pagesJamal Gill CVJamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- Jamal Anwer Gill: Curriculam VitaeDocument2 pagesJamal Anwer Gill: Curriculam VitaeJamal GillNo ratings yet

- A Gold Medalist Has Always Been A Valuable Asset For The Organizations Like You..so Add One More Gold Medalist To Your HR Profile by Recruiting MeDocument1 pageA Gold Medalist Has Always Been A Valuable Asset For The Organizations Like You..so Add One More Gold Medalist To Your HR Profile by Recruiting MeJamal GillNo ratings yet

- Advt - No - 10-2013Document6 pagesAdvt - No - 10-2013Jamal GillNo ratings yet

- Bs (C0Mmerce) : Ahmad Usman KhanDocument2 pagesBs (C0Mmerce) : Ahmad Usman KhanJamal GillNo ratings yet

- A Gold Medalist Has Always Been A Valuable Asset For The Organizations Like You..so Add One More Gold Medalist To Your HR Profile by Recruiting MeDocument1 pageA Gold Medalist Has Always Been A Valuable Asset For The Organizations Like You..so Add One More Gold Medalist To Your HR Profile by Recruiting MeJamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- Marshall School of Business University of Southern California)Document7 pagesMarshall School of Business University of Southern California)Jamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- Jamal CV SimpleDocument2 pagesJamal CV SimpleJamal GillNo ratings yet

- ItDocument2 pagesItJamal GillNo ratings yet

- Exploratory Research - PDF TWDocument12 pagesExploratory Research - PDF TWTen WangNo ratings yet

- Model Test 2Document19 pagesModel Test 2Jamal GillNo ratings yet

- Candidate Information Form (CD - 1) : H01-FM006-02 Page 1 of 2Document2 pagesCandidate Information Form (CD - 1) : H01-FM006-02 Page 1 of 2mahmoodanwar34No ratings yet

- Jamal Gill CVDocument2 pagesJamal Gill CVJamal GillNo ratings yet

- Problem Set Capital StructureDocument2 pagesProblem Set Capital StructureBaba Nyonya0% (1)

- Title of Module: Intermediate Accounting 3 Topic: I. Book Value Per Share Learning ObjectivesDocument19 pagesTitle of Module: Intermediate Accounting 3 Topic: I. Book Value Per Share Learning ObjectivesDenmark CabadduNo ratings yet

- Module 1 Current LiabilitiesDocument13 pagesModule 1 Current LiabilitiesLea Yvette SaladinoNo ratings yet

- Standalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Document6 pagesStandalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Multiples Choice Questions With AnswersDocument60 pagesMultiples Choice Questions With AnswersVaibhav Rusia100% (2)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErine ContranoNo ratings yet

- Worldwide Paper Company Woodyard Investment AnalysisDocument1 pageWorldwide Paper Company Woodyard Investment AnalysisKritikaPandeyNo ratings yet

- 1.1.1partnership FormationDocument12 pages1.1.1partnership FormationCundangan, Denzel Erick S.No ratings yet

- Financial Statement Analysis: Fundamentals of Corporate FinanceDocument23 pagesFinancial Statement Analysis: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Chapter - 6 - Bases For Comparison of Alternatives - 3Document38 pagesChapter - 6 - Bases For Comparison of Alternatives - 3Ahmed freshekNo ratings yet

- Write - Off Sample CasesDocument16 pagesWrite - Off Sample CasesLiDdy Cebrero BelenNo ratings yet

- LEMBAR KERJA Laporan Keuangan 1thnDocument19 pagesLEMBAR KERJA Laporan Keuangan 1thnCool ThryNo ratings yet

- !!!!!!!!!!balance SheetDocument1 page!!!!!!!!!!balance Sheetquickoffice_sqaNo ratings yet

- Test Bank Accounting Management 11e Chapter 03 Cost Volume Profit AnalysisDocument23 pagesTest Bank Accounting Management 11e Chapter 03 Cost Volume Profit AnalysisMahmoud AhmedNo ratings yet

- Accounting Changes//: Accounting Estimate Accounting PolicyDocument2 pagesAccounting Changes//: Accounting Estimate Accounting PolicyFaye RagosNo ratings yet

- 3int - 2008 - Jun - Ans CAT T3Document6 pages3int - 2008 - Jun - Ans CAT T3asad19No ratings yet

- Additional Consolidation Reporting IssuesDocument61 pagesAdditional Consolidation Reporting IssuesDifaNo ratings yet

- Managerial Accounting Sem 1Document556 pagesManagerial Accounting Sem 1Rakesh Singh100% (1)

- Discussion QuestionsDocument34 pagesDiscussion QuestionsCarlos arnaldo lavadoNo ratings yet

- Accounting Review QuestionsDocument34 pagesAccounting Review Questionsjoyce KimNo ratings yet

- Accounting 1 Module 3Document20 pagesAccounting 1 Module 3Rose Marie Recorte100% (1)

- Tugas Kelompok 03 (Tugas Sesi 7)Document3 pagesTugas Kelompok 03 (Tugas Sesi 7)MUHAMMAD RAKA SIGIT AYUGHANo ratings yet

- ACCO 20043 Financial Accounting and Reporting 2 FinalsDocument16 pagesACCO 20043 Financial Accounting and Reporting 2 FinalsPaul BandolaNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- VSI ABC Analysis for CA Final FR Dec 2021Document4 pagesVSI ABC Analysis for CA Final FR Dec 2021Keerthan GowdaNo ratings yet

- Cash Conversion CycleDocument18 pagesCash Conversion CycleRashidul HasanNo ratings yet

- Written By: Unknown: Yardsticks To Value Stocks in Different SectorsDocument5 pagesWritten By: Unknown: Yardsticks To Value Stocks in Different SectorsKrs_Rs_4407No ratings yet

- SG 4 - Moms - Com Negotiation Result Form-Hasil DiskusiDocument23 pagesSG 4 - Moms - Com Negotiation Result Form-Hasil DiskusiFadhila Hanif100% (1)

- Team Project 2: Chapter 8: Investment Decision Rules Fundamentals of Capital BudgetingDocument61 pagesTeam Project 2: Chapter 8: Investment Decision Rules Fundamentals of Capital BudgetingБекФорд ЗакNo ratings yet

- Business combination equipment valuationDocument3 pagesBusiness combination equipment valuationJohn Philip L ConcepcionNo ratings yet