You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- SIP Presentation PDFDocument21 pagesSIP Presentation PDFSheikh AaishanNo ratings yet

- Accountancy Ebook - Class 12 - Part 2 PDFDocument110 pagesAccountancy Ebook - Class 12 - Part 2 PDFkapurrohit489145% (44)

- SIP PresentationDocument21 pagesSIP PresentationSheikh AaishanNo ratings yet

- Std11 Acct EMDocument159 pagesStd11 Acct EMniaz1788100% (1)

- Chapter 9 Ratio Analysis PDFDocument65 pagesChapter 9 Ratio Analysis PDFahmadfaiq01No ratings yet

- Advanced Bank Management: IntroductiontopartnershipDocument18 pagesAdvanced Bank Management: IntroductiontopartnershipSheikh AaishanNo ratings yet

- KASDocument1 pageKASSheikh AaishanNo ratings yet

- Trigonometry Basic IdentityDocument2 pagesTrigonometry Basic IdentitySheikh AaishanNo ratings yet

- How To Write A Business PlanDocument37 pagesHow To Write A Business Planapi-309082881No ratings yet

- CV SampleDocument2 pagesCV Sampleanand906No ratings yet

- There Are 5 RedDocument2 pagesThere Are 5 RedSheikh AaishanNo ratings yet

- Simplification Techniques and TricksDocument45 pagesSimplification Techniques and TricksSheikh AaishanNo ratings yet

- Consumerism in IndiaDocument32 pagesConsumerism in IndiaSheikh AaishanNo ratings yet

- ProjectDocument3 pagesProjectSheikh AaishanNo ratings yet

- CIMA 2015 Professional Qualification SyllabusDocument51 pagesCIMA 2015 Professional Qualification SyllabusLuzuko Terence Nelani0% (1)

- Core Indicators - UNDP VersionDocument12 pagesCore Indicators - UNDP VersionRaghav RaghunathanNo ratings yet

- Synopsis FormatDocument3 pagesSynopsis Formatbkunal685% (34)

- Bull Spread With European Call Options: Inputs Bought Call Sold CallDocument9 pagesBull Spread With European Call Options: Inputs Bought Call Sold CallSheikh AaishanNo ratings yet

- Business Law Self-Learning ManualDocument218 pagesBusiness Law Self-Learning ManualSheikh AaishanNo ratings yet

- Operation PlanDocument4 pagesOperation PlanSheikh AaishanNo ratings yet

- DMCH15Document30 pagesDMCH15Sheikh AaishanNo ratings yet

- Case Law in MGT 518Document18 pagesCase Law in MGT 518Sheikh AaishanNo ratings yet

- Sample Questions For SWAPDocument4 pagesSample Questions For SWAPKarthik Nandula100% (1)

- Introduction 000Document8 pagesIntroduction 000Sheikh AaishanNo ratings yet

- ANALYSIS of Comperative Balance SheetDocument1 pageANALYSIS of Comperative Balance SheetSheikh AaishanNo ratings yet

- FactorDocument10 pagesFactorSheikh AaishanNo ratings yet

- New Financial Ratios For Microfinance Reporting: I'm Standar Ds Compliant I'm Standar Ds CompliantDocument10 pagesNew Financial Ratios For Microfinance Reporting: I'm Standar Ds Compliant I'm Standar Ds CompliantSheikh AaishanNo ratings yet

- ANALYSIS of Comperative Balance SheetDocument1 pageANALYSIS of Comperative Balance SheetSheikh AaishanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Pemetaan BDDocument17 pagesPemetaan BDNaurelNo ratings yet

- MOS GameDocument13 pagesMOS GameNuhtimNo ratings yet

- Benefits of EDocument4 pagesBenefits of EMeenakshiParasharNo ratings yet

- Model AGM Notice of Sarswat PDFDocument56 pagesModel AGM Notice of Sarswat PDFMandar Kadam100% (1)

- Jade McCarneyDocument4 pagesJade McCarneyjademariemccarneyNo ratings yet

- Paper 1 Business Studies Grde 12 Preliminary Examination Revision StrategyDocument10 pagesPaper 1 Business Studies Grde 12 Preliminary Examination Revision Strategycianjacob46No ratings yet

- Questionnaire On ParleDocument3 pagesQuestionnaire On ParleKaustubh ShindeNo ratings yet

- NHA Notes To FS 2012Document28 pagesNHA Notes To FS 2012Jay Bryson RuizNo ratings yet

- A Study On Customer Satisfaction Towards Departmental Stored in Raipur City Satyajit SarkarDocument55 pagesA Study On Customer Satisfaction Towards Departmental Stored in Raipur City Satyajit SarkarSATYA07100% (1)

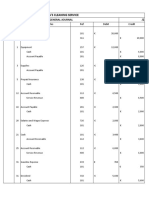

- Anya's Cleaning ServiceDocument22 pagesAnya's Cleaning ServiceArya HerdiansyahNo ratings yet

- GMAT - Math (19.5.2023)Document17 pagesGMAT - Math (19.5.2023)thelkokomg_294988315No ratings yet

- Part Ii Insight March 2018Document121 pagesPart Ii Insight March 2018Islamiat PopoolaNo ratings yet

- 4-1 The Responsibilities and AccountabilitiesDocument39 pages4-1 The Responsibilities and AccountabilitiesAlvin Reynoso LumabanNo ratings yet

- BabygarmentsDocument20 pagesBabygarmentsMSM HUBNo ratings yet

- Mapping Customer Journeys in Multichannel Decision-Making: DR Julia Wolny and Nipawan CharoensuksaiDocument10 pagesMapping Customer Journeys in Multichannel Decision-Making: DR Julia Wolny and Nipawan Charoensuksaisita deliyana FirmialyNo ratings yet

- Oracle Inventory and Costing Cloud EbookDocument11 pagesOracle Inventory and Costing Cloud Ebooksingh_indrajeetkumarNo ratings yet

- Test Bank For Forensic Accounting and Fraud Examination 2nd Edition Mary Jo Kranacher Richard Riley 417Document8 pagesTest Bank For Forensic Accounting and Fraud Examination 2nd Edition Mary Jo Kranacher Richard Riley 417melissaandersenbgkxmfzyrj100% (24)

- NSCC International Business Internship - FlyerDocument2 pagesNSCC International Business Internship - FlyerNSCC International BusinessNo ratings yet

- The Impact of IFRS On Financial StatementsDocument84 pagesThe Impact of IFRS On Financial StatementsPrithviNo ratings yet

- How To Write A Sewing Business PlanDocument13 pagesHow To Write A Sewing Business PlanAshenafi DressNo ratings yet

- Fabm2 - Q2 - M10Document13 pagesFabm2 - Q2 - M10Ryza Mae AbabaoNo ratings yet

- Value Proposition Apollo HospitalsDocument2 pagesValue Proposition Apollo Hospitalsakashkr619No ratings yet

- Silk ProductsDocument77 pagesSilk ProductsHimanshu PandeyNo ratings yet

- of DettolDocument15 pagesof DettolFerdows Abid ChowdhuryNo ratings yet

- May 2011Document43 pagesMay 2011rgsr2008No ratings yet

- CH 4Document21 pagesCH 4Amir HussainNo ratings yet

- Account TitlesDocument28 pagesAccount TitlesTom FernandoNo ratings yet

- 2.1c Business Finance Test Review Class 2020 With AnswersDocument4 pages2.1c Business Finance Test Review Class 2020 With Answersbobhamilton3489No ratings yet

- Intermediate Accounting Practice HandoutsDocument8 pagesIntermediate Accounting Practice HandoutspolxrixNo ratings yet

- Sales Letter Template 07Document10 pagesSales Letter Template 07Nurulsyahirah NasirNo ratings yet