You might also like

- Problem Set 2 International Finance SolutionsDocument9 pagesProblem Set 2 International Finance SolutionsSourav NandyNo ratings yet

- Alsha YaDocument1 pageAlsha YaAtul MittalNo ratings yet

- Quotation: Vat/Tin: 29471119182 CST No: 29471119182 PannoDocument1 pageQuotation: Vat/Tin: 29471119182 CST No: 29471119182 PannoAtul MittalNo ratings yet

- Capital BudgettingDocument31 pagesCapital Budgettingkataruka123No ratings yet

- Suncoast Office, A Goal Programming Problem, Solution, Analysis, Sensitivity Analysis, and ReportDocument8 pagesSuncoast Office, A Goal Programming Problem, Solution, Analysis, Sensitivity Analysis, and ReportArka ChakrabortyNo ratings yet

- National Institute of Research CentreDocument66 pagesNational Institute of Research CentreAtul MittalNo ratings yet

- Johnson RuleDocument2 pagesJohnson RuleKaran MadaanNo ratings yet

- Syllabus: Faculty of Management Studies, University of DelhiDocument7 pagesSyllabus: Faculty of Management Studies, University of DelhiAtul MittalNo ratings yet

- QDFADocument65 pagesQDFAAtul MittalNo ratings yet

- CDR Master Circular 2012Document72 pagesCDR Master Circular 2012Gaurav KukrejaNo ratings yet

- Online GroceryDocument6 pagesOnline GroceryAtul Mittal100% (1)

- 2013 Course CatalogDocument12 pages2013 Course CatalogAtul MittalNo ratings yet

- 15 Min Guide To GMATDocument13 pages15 Min Guide To GMATAaron CampbellNo ratings yet

- Transfer Pricing: Optimal Product Mix and Divisional ProfitsDocument69 pagesTransfer Pricing: Optimal Product Mix and Divisional ProfitsAtul Mittal100% (1)

- Intel Capital PortfolioDocument95 pagesIntel Capital PortfolioAtul MittalNo ratings yet

- Products of Large CorporatesDocument3 pagesProducts of Large CorporatesAtul MittalNo ratings yet

- Exposure Norms - RBI CircularDocument38 pagesExposure Norms - RBI CircularAtul MittalNo ratings yet

- FMS Admission Brochure 2012Document44 pagesFMS Admission Brochure 2012pisthuNo ratings yet

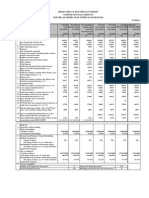

- BHARAT HEAVY ELECTRICALS LIMITED AUDITED FINANCIAL RESULTS FOR Q4 AND FY 2012Document3 pagesBHARAT HEAVY ELECTRICALS LIMITED AUDITED FINANCIAL RESULTS FOR Q4 AND FY 2012Shubham TrivediNo ratings yet

- Previous Year GD & Extempore Topic1Document5 pagesPrevious Year GD & Extempore Topic1Raj KumarNo ratings yet

- UniversitiesDocument1 pageUniversitiesAtul MittalNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- DMTM - NTC Online Acq - V001 NOV 2020 (Eng)Document18 pagesDMTM - NTC Online Acq - V001 NOV 2020 (Eng)Kartik KumarasamyNo ratings yet

- EC3115 - Monetary EconomicsDocument190 pagesEC3115 - Monetary EconomicsEdwin Aw100% (6)

- Financial Ratio Analysis of The City Bank LimitedDocument49 pagesFinancial Ratio Analysis of The City Bank LimitedshovowNo ratings yet

- Financial Frictions and Fluctuations in VolatilityDocument55 pagesFinancial Frictions and Fluctuations in VolatilityHHHNo ratings yet

- Effects of Deposits Mobilization On The Financial Performance of Microfinance Banks in Nigeria - A Study of Umuchinemere Pro-Credit Micro Finance Bank LimitedDocument76 pagesEffects of Deposits Mobilization On The Financial Performance of Microfinance Banks in Nigeria - A Study of Umuchinemere Pro-Credit Micro Finance Bank LimitedPrashant chaudharyNo ratings yet

- Ratios and PercentagesDocument10 pagesRatios and PercentagesPenmetsa Satyanarayana RajuNo ratings yet

- Rural Hosehold Demand in India - Analysis ReportDocument19 pagesRural Hosehold Demand in India - Analysis ReportkakuNo ratings yet

- VaR Implementation in G-SEC PortfolioDocument193 pagesVaR Implementation in G-SEC PortfolioDharmender KumarNo ratings yet

- Asce 7-22 CH 17 - For PCDocument42 pagesAsce 7-22 CH 17 - For PCsharethefilesNo ratings yet

- Jardenil V SalasDocument1 pageJardenil V Salascmv mendozaNo ratings yet

- Mortgage Backed Securities ExplainedDocument3 pagesMortgage Backed Securities Explainedmaria_tigasNo ratings yet

- FarazDocument3 pagesFarazSai SholinganallurNo ratings yet

- Net Present Value, Future Value, Mortgage Payments, Investment Returns, Bond Yields & Stock PricesDocument5 pagesNet Present Value, Future Value, Mortgage Payments, Investment Returns, Bond Yields & Stock PricesQuân VõNo ratings yet

- Investment Principles and Checklists OrdwayDocument149 pagesInvestment Principles and Checklists Ordwayevolve_us100% (2)

- Debt Equity Ratio MBA IIDocument17 pagesDebt Equity Ratio MBA IINiraj GuptaNo ratings yet

- Police Constable: SUSC - 2022 Mains Grand Test - 045Document32 pagesPolice Constable: SUSC - 2022 Mains Grand Test - 045vsurender reddyNo ratings yet

- Revised Co-Maker Policy Word DocsDocument4 pagesRevised Co-Maker Policy Word DocsAko C IanNo ratings yet

- Derivatives and Risk ManagementDocument17 pagesDerivatives and Risk ManagementDeepak guptaNo ratings yet

- AT Module-7 4th-EdnDocument74 pagesAT Module-7 4th-EdnAnton KhauNo ratings yet

- Other Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateDocument18 pagesOther Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateZaaavnn VannnnnNo ratings yet

- LECTURE 7 - Asset - Liability ManagementDocument19 pagesLECTURE 7 - Asset - Liability ManagementYvonneNo ratings yet

- Real GDP measures base year pricesDocument161 pagesReal GDP measures base year pricesHijab PrincessNo ratings yet

- Mortgage Market ExerciseshuDocument2 pagesMortgage Market ExerciseshuaryannnevillafuerteNo ratings yet

- Home Health Agency Change of Ownership or Control FormDocument12 pagesHome Health Agency Change of Ownership or Control FormReading_EagleNo ratings yet

- Annual Report 2017 PDFDocument376 pagesAnnual Report 2017 PDFanu riazNo ratings yet

- Personal Financial Planning LectureDocument52 pagesPersonal Financial Planning LectureSara LlameraNo ratings yet

- Advanced Bond ConceptsDocument8 pagesAdvanced Bond ConceptsEllaine OlimberioNo ratings yet

- Power and Energy Systems Engineering Economics Best Practice ManualDocument188 pagesPower and Energy Systems Engineering Economics Best Practice ManualkhusnunNo ratings yet

- Compound Interest Compound Interest: What Is 'Compound Interest' What Is 'Compound Interest'Document7 pagesCompound Interest Compound Interest: What Is 'Compound Interest' What Is 'Compound Interest'Pat PathairushNo ratings yet

- Public Sector Banks and Their TransformationDocument19 pagesPublic Sector Banks and Their TransformationJitendra Kumar RamNo ratings yet