You might also like

- Automotive Lubricants: Supply Chain ManagementDocument6 pagesAutomotive Lubricants: Supply Chain ManagementMvb TradersNo ratings yet

- Future Outlook Indian Lub MarketDocument20 pagesFuture Outlook Indian Lub MarketPrabhu AgrawalNo ratings yet

- Global Lubricants and Base Oil Market: Trends & Opportunities (2014 Edition) - New Report by Daedal ResearchDocument12 pagesGlobal Lubricants and Base Oil Market: Trends & Opportunities (2014 Edition) - New Report by Daedal ResearchDaedal ResearchNo ratings yet

- Supply Chain Process of HPCLDocument27 pagesSupply Chain Process of HPCLAvinaba HazraNo ratings yet

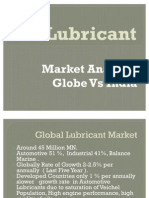

- Lubricant Market Globe Vs IndiaDocument19 pagesLubricant Market Globe Vs IndiaSandeep Walke100% (1)

- Lube IndiaDocument16 pagesLube IndiaSurya TejaNo ratings yet

- Business Opportunities in The Emerging Lubricant Markets of South Asia, The Middle East, and Northern Africa, 2005-2015Document11 pagesBusiness Opportunities in The Emerging Lubricant Markets of South Asia, The Middle East, and Northern Africa, 2005-2015Vishan SharmaNo ratings yet

- The Indian Lubricant Market - Survival of The SlickestDocument3 pagesThe Indian Lubricant Market - Survival of The SlickestajakbbNo ratings yet

- Development of Lubricant Industry in Next 5 YearsDocument4 pagesDevelopment of Lubricant Industry in Next 5 YearsDebalina SahaNo ratings yet

- Sales and Distribution Management of CastrolDocument17 pagesSales and Distribution Management of CastrolSourabh Saxena80% (10)

- Channel Conflict-Lubricant Markets-Petroleum IndustryDocument12 pagesChannel Conflict-Lubricant Markets-Petroleum IndustryNikhil100% (1)

- Survey On Various Lubricant Companies in India: Synopsis ofDocument14 pagesSurvey On Various Lubricant Companies in India: Synopsis ofRupesh KumarNo ratings yet

- Sale & Distribution Management: End Term Project ONDocument17 pagesSale & Distribution Management: End Term Project ONMd Saharukh AhamedNo ratings yet

- E&I Group ProjectDocument19 pagesE&I Group ProjectParth PanchalNo ratings yet

- Lubricant Market in IndiaDocument8 pagesLubricant Market in IndiaManthan Gattani100% (2)

- Synopsis ON Working Capital Management ON Shri Ram Life Insurance Company LTDocument23 pagesSynopsis ON Working Capital Management ON Shri Ram Life Insurance Company LTJunaid IqbalNo ratings yet

- Total Lubricants - Marketing StrategyDocument15 pagesTotal Lubricants - Marketing StrategyBenson Almeida82% (17)

- UntitledDocument5 pagesUntitledapi-293819200No ratings yet

- Oil and Gas Sector CrasherDocument6 pagesOil and Gas Sector CrasherRahul MehayNo ratings yet

- Costrol India Ltd-Monarch ResearchDocument14 pagesCostrol India Ltd-Monarch ResearchAvinash KamathNo ratings yet

- Base Oil Product TrendsDocument18 pagesBase Oil Product Trendsrvsingh100% (2)

- Global Turbine Oil MarketDocument13 pagesGlobal Turbine Oil MarketSanjay MatthewsNo ratings yet

- India Is The Sixth Largest Lubricant Market in The World With Estimated Revenues of RsDocument4 pagesIndia Is The Sixth Largest Lubricant Market in The World With Estimated Revenues of RsPrasanta BiswasNo ratings yet

- Dr. Prafulla A. Pawar - MKTDocument5 pagesDr. Prafulla A. Pawar - MKTChetal BholeNo ratings yet

- A Project Report On Indian Oil SectorDocument64 pagesA Project Report On Indian Oil SectorPranay Raju RallabandiNo ratings yet

- Indian Petroleum IndustryDocument11 pagesIndian Petroleum IndustryruchirsworldNo ratings yet

- Overview of Oil and Gas SectorDocument8 pagesOverview of Oil and Gas SectorMudit KothariNo ratings yet

- Global Ad Trends The Pivot To e PDFDocument5 pagesGlobal Ad Trends The Pivot To e PDFGauri SinghNo ratings yet

- 12 - Chapter 4 PDFDocument26 pages12 - Chapter 4 PDFDarsh LathiaNo ratings yet

- Branding Practices of Public and Private Sector Oil Companies - Indian Lubricant MarketDocument9 pagesBranding Practices of Public and Private Sector Oil Companies - Indian Lubricant MarketIrfan RamdhaniNo ratings yet

- Bangladesh Lubricants Market - Growth, Trends, and Forecast (2019 - 2024)Document10 pagesBangladesh Lubricants Market - Growth, Trends, and Forecast (2019 - 2024)Mahedi HasanNo ratings yet

- Indian Tyre Industry: Porter's Five Forces AnalysisDocument9 pagesIndian Tyre Industry: Porter's Five Forces AnalysisRohit MalhotraNo ratings yet

- Material BalanceDocument58 pagesMaterial BalanceAnonymous zWnXYeFkdk50% (2)

- Oligopoly in Oil Refinery IndustryDocument5 pagesOligopoly in Oil Refinery IndustryDokania Anish100% (2)

- Lubricant IndustryDocument48 pagesLubricant IndustryJay_ntNo ratings yet

- Reliance Industries Limted Company AnalysisDocument10 pagesReliance Industries Limted Company AnalysisDivya Prakash MishraNo ratings yet

- IOCL ReportDocument16 pagesIOCL Reportmannu.abhimanyu309893% (14)

- Indian Petrolium Industry EsseyDocument15 pagesIndian Petrolium Industry EsseyShashank BansalNo ratings yet

- Assessing Market Potential of CNG Engine Oil FOR Gulf Oil Corporation Limited BY Neha 203Document68 pagesAssessing Market Potential of CNG Engine Oil FOR Gulf Oil Corporation Limited BY Neha 203Abhinav SaraswatNo ratings yet

- Persistence Market ResearchDocument7 pagesPersistence Market Researchapi-302003482No ratings yet

- Table of Contents For Industry Focus-Lubricants & Engine OilsDocument4 pagesTable of Contents For Industry Focus-Lubricants & Engine OilsJinalSNo ratings yet

- Strengths: Brand EquitiesDocument6 pagesStrengths: Brand EquitiesSHETTY VIRAJNo ratings yet

- Company Analysis - CastrolDocument12 pagesCompany Analysis - CastrolSamirNo ratings yet

- Hexa Research IncDocument4 pagesHexa Research Incapi-293819200No ratings yet

- Indian OilDocument41 pagesIndian Oilj_sachin09No ratings yet

- Finel ProjectDocument64 pagesFinel Projectsandy100% (3)

- Mudranki FileDocument78 pagesMudranki Filedrashyagarg7No ratings yet

- Task 7 RefDocument25 pagesTask 7 Refsreejith emNo ratings yet

- L146 2018 08 Aug IndiaDocument1 pageL146 2018 08 Aug IndiasudhanshuNo ratings yet

- S I: F C G C: Arindam Banerjee Muzaffar Jamal Dheeraj AwasthyDocument31 pagesS I: F C G C: Arindam Banerjee Muzaffar Jamal Dheeraj AwasthyOsama AshrafNo ratings yet

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitFrom EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitNo ratings yet

- Lubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6From EverandLubrication Tactics for Industries Made Simple, 8th Discipline of World Class Maintenance Management: 1, #6Rating: 5 out of 5 stars5/5 (1)

- Machinery Oil Analysis & Condition Monitoring : A Practical Guide to Sampling and Analyzing Oil to Improve Equipment ReliabilityFrom EverandMachinery Oil Analysis & Condition Monitoring : A Practical Guide to Sampling and Analyzing Oil to Improve Equipment ReliabilityRating: 3 out of 5 stars3/5 (4)

- Reaching Zero with Renewables: Biojet FuelsFrom EverandReaching Zero with Renewables: Biojet FuelsNo ratings yet

- Heavy and Extra-heavy Oil Upgrading TechnologiesFrom EverandHeavy and Extra-heavy Oil Upgrading TechnologiesRating: 4 out of 5 stars4/5 (2)

- Services Marketing Lovelock Wirtz Chaterjee CH 13Document22 pagesServices Marketing Lovelock Wirtz Chaterjee CH 13Harinesh PandyaNo ratings yet

- Romanian National Hospital Master Plan A New Strategy For Hospital Infrastructure DevelopmentDocument66 pagesRomanian National Hospital Master Plan A New Strategy For Hospital Infrastructure DevelopmentHarinesh PandyaNo ratings yet

- Cold Mix Asphalt and Specification of It PDFDocument7 pagesCold Mix Asphalt and Specification of It PDFle thanhNo ratings yet

- Harita Seating Systems Annual Report 2012-13Document84 pagesHarita Seating Systems Annual Report 2012-13Harinesh PandyaNo ratings yet

- IntroductionDocument16 pagesIntroductionA1B2C3D4G6No ratings yet

- Oil and Gas BudgetDocument32 pagesOil and Gas BudgetHarinesh PandyaNo ratings yet

- Auto and Auto Ancillaries Sector in IndiaDocument0 pagesAuto and Auto Ancillaries Sector in IndiaHarinesh PandyaNo ratings yet

- Organised RetailDocument51 pagesOrganised RetailHarinesh PandyaNo ratings yet

- SH 2013 Q3 1 ICRA AutomobilesDocument5 pagesSH 2013 Q3 1 ICRA AutomobilesHarinesh PandyaNo ratings yet

- Make or Break - Why Accurate Cost Estimation Is Key ArticleDocument0 pagesMake or Break - Why Accurate Cost Estimation Is Key ArticleHarinesh PandyaNo ratings yet

- Annnual Report UjalaDocument168 pagesAnnnual Report UjalaHarinesh PandyaNo ratings yet

- Crisis Time For India Again at The WTODocument4 pagesCrisis Time For India Again at The WTOHarinesh PandyaNo ratings yet

- MC FinalDocument5 pagesMC FinalHarinesh PandyaNo ratings yet

- 31.job Costing (Exercise Questions)Document6 pages31.job Costing (Exercise Questions)Harinesh PandyaNo ratings yet

- 11a.introduction To Cost Management - Horngren SupplementDocument4 pages11a.introduction To Cost Management - Horngren SupplementHarinesh PandyaNo ratings yet

- Crisis Time For India Again at The WTODocument4 pagesCrisis Time For India Again at The WTOHarinesh PandyaNo ratings yet

- Operations Management and Strategy For Your ReadingDocument9 pagesOperations Management and Strategy For Your ReadingHarinesh PandyaNo ratings yet

- Crisis Time For India Again at The WTODocument4 pagesCrisis Time For India Again at The WTOHarinesh PandyaNo ratings yet

- Challenges of Tata Steel's Corus Takeover - India Knowledge@WhartonDocument4 pagesChallenges of Tata Steel's Corus Takeover - India Knowledge@WhartonHarinesh PandyaNo ratings yet

- Romanian National Hospital Master Plan A New Strategy For Hospital Infrastructure DevelopmentDocument66 pagesRomanian National Hospital Master Plan A New Strategy For Hospital Infrastructure DevelopmentHarinesh PandyaNo ratings yet

- Adialisation in Ndia: Insights & AnalysisDocument38 pagesAdialisation in Ndia: Insights & AnalysisHarinesh PandyaNo ratings yet

- Start Page Numbering at A Specific Page in MS WordDocument2 pagesStart Page Numbering at A Specific Page in MS WordHarinesh PandyaNo ratings yet

- India's Growing Retail Industry ReportDocument11 pagesIndia's Growing Retail Industry ReportPiyush JainNo ratings yet

- Information Technology - EssentialsDocument23 pagesInformation Technology - EssentialsHarinesh PandyaNo ratings yet

- IntroductionDocument16 pagesIntroductionA1B2C3D4G6No ratings yet

- Kingfisher Airlines - Audited Results 2012Document2 pagesKingfisher Airlines - Audited Results 2012Harinesh PandyaNo ratings yet

- Frekonomics Final ReviewDocument15 pagesFrekonomics Final ReviewHarinesh PandyaNo ratings yet

- History of Big Bazaar Final HRM Final ProjectDocument6 pagesHistory of Big Bazaar Final HRM Final ProjectHarinesh PandyaNo ratings yet

- Tata CorusDocument14 pagesTata CorusHarinesh PandyaNo ratings yet

- NLP Endorsement LetterDocument2 pagesNLP Endorsement LetterVan Russel Anajao RoblesNo ratings yet

- BP Golden Rules of SafetyDocument10 pagesBP Golden Rules of SafetyAzad Namazov100% (1)

- Open Source Tools: Boring Head Exploded ViewDocument7 pagesOpen Source Tools: Boring Head Exploded ViewTom RuxtonNo ratings yet

- WPQ Ejcom Nr476Document13 pagesWPQ Ejcom Nr476Touil HoussemNo ratings yet

- Past Questions and Question Spotting 2022 InteractionsDocument10 pagesPast Questions and Question Spotting 2022 InteractionsSamantha AnyangoNo ratings yet

- DB 01 SubstationDocument1 pageDB 01 Substationfahamida joyaNo ratings yet

- Investor and Analyst Perceptions of Improving Audit Quality with Auditor TenureDocument28 pagesInvestor and Analyst Perceptions of Improving Audit Quality with Auditor TenureAndersonMonteiroNo ratings yet

- PDF Ciara Herndon Resume December 2020Document3 pagesPDF Ciara Herndon Resume December 2020api-484247819No ratings yet

- Pergunta 1: 1 / 1 PontoDocument22 pagesPergunta 1: 1 / 1 PontoBruno CuryNo ratings yet

- CCN Lab Assignment # 3 (70067010)Document15 pagesCCN Lab Assignment # 3 (70067010)HANNAN TARIQNo ratings yet

- Black BookDocument9 pagesBlack Book148 Kanchan SasaneNo ratings yet

- Sample Complaint Letter Bank Fees IIDocument2 pagesSample Complaint Letter Bank Fees IIRoshan Khan100% (1)

- Troubleshooting OSPF - Cisco LiveDocument113 pagesTroubleshooting OSPF - Cisco LiveRakesh MadhanNo ratings yet

- Solution Manual For Personal Finance 12th Edition by GarmanDocument7 pagesSolution Manual For Personal Finance 12th Edition by Garmana719435805No ratings yet

- Chapter 6Document8 pagesChapter 6Coci KhouryNo ratings yet

- CAGM 8601 Maintenance Organisation Approval CAAM Part 145Document90 pagesCAGM 8601 Maintenance Organisation Approval CAAM Part 145Dwayne MarvinNo ratings yet

- About EthiopianDocument7 pagesAbout EthiopianTiny GechNo ratings yet

- Final Step-B Answer KeyDocument4 pagesFinal Step-B Answer KeyUnwantedNo ratings yet

- Annotated Bibliography Assignment 2Document5 pagesAnnotated Bibliography Assignment 2Kam MoshierNo ratings yet

- SME Bank Employees Seek Separation PayDocument20 pagesSME Bank Employees Seek Separation PayRoberts SamNo ratings yet

- Chesterton - Outline of SanityDocument82 pagesChesterton - Outline of SanityKeith BuhlerNo ratings yet

- AY - XP 081013 CE AE-X 081013 BE S Manual 2004-s2Document52 pagesAY - XP 081013 CE AE-X 081013 BE S Manual 2004-s2José MacedoNo ratings yet

- Degree Veri Form PDFDocument4 pagesDegree Veri Form PDFShakeel AhmedNo ratings yet

- Katalog SNI Kehutanan PDFDocument2 pagesKatalog SNI Kehutanan PDFLaichul MachfudhorNo ratings yet

- Breaking Samsung's Root of Trust by Exploiting S-BootDocument77 pagesBreaking Samsung's Root of Trust by Exploiting S-BootcalculusNo ratings yet

- Minutes - Inventory Case FoldersDocument2 pagesMinutes - Inventory Case FoldersCA CANo ratings yet

- REST, dojo, JavaFX: Catalog App</TITLEDocument45 pagesREST, dojo, JavaFX: Catalog App</TITLEnaresh921No ratings yet

- Phaser 7100Document40 pagesPhaser 7100luterocoruna8342No ratings yet

- Men's Health - Australia (August 2016) (PDFDrive)Document156 pagesMen's Health - Australia (August 2016) (PDFDrive)pedroNo ratings yet

- Decreased Intracranial Pressure With Optimal Head Elevation of 30 or 45 Degrees in Traumatic Brain Injury Patients (Literatur Review)Document4 pagesDecreased Intracranial Pressure With Optimal Head Elevation of 30 or 45 Degrees in Traumatic Brain Injury Patients (Literatur Review)Theresia Avila KurniaNo ratings yet