You might also like

- Procedure of Credit RatingDocument57 pagesProcedure of Credit RatingMilon SultanNo ratings yet

- Financial Management LO3Document6 pagesFinancial Management LO3Hadeel Abdul Salam100% (1)

- Compliance FAQ GuideDocument5 pagesCompliance FAQ GuideJagadeeshwar ReddyNo ratings yet

- Capital BudgetingDocument62 pagesCapital BudgetingtanyaNo ratings yet

- Cost Audit Report CRA 3 (In Excel)Document25 pagesCost Audit Report CRA 3 (In Excel)aishwarya raikar100% (1)

- RBI Response on Inoperative Bank Accounts and Unclaimed AmountsDocument29 pagesRBI Response on Inoperative Bank Accounts and Unclaimed AmountsigoysinghNo ratings yet

- UnderwritingDocument3 pagesUnderwritingkalidharNo ratings yet

- Audit & Assurance 2012Document13 pagesAudit & Assurance 2012S M Wadud TuhinNo ratings yet

- 12 - Summary and ConclusionDocument13 pages12 - Summary and ConclusionJanak SinghNo ratings yet

- CDR Master Circular 2012Document72 pagesCDR Master Circular 2012Gaurav KukrejaNo ratings yet

- Exam 1 PDFDocument4 pagesExam 1 PDFFiraa'ool YusufNo ratings yet

- Election Prediction - 2020 - All Island AnalysisDocument241 pagesElection Prediction - 2020 - All Island AnalysisSanjeewa HemaratneNo ratings yet

- Finc631 TestDocument10 pagesFinc631 TestsushilNo ratings yet

- Tips On Project FinancingDocument3 pagesTips On Project FinancingRattinakumar SivaradjouNo ratings yet

- Questions - Rebate On Bills DiscountedDocument4 pagesQuestions - Rebate On Bills DiscountedJiss Palelil0% (1)

- Profit Prior To IncorporationDocument30 pagesProfit Prior To Incorporationsyed amanNo ratings yet

- Working Capital Management: A Guide to Optimizing Current AssetsDocument6 pagesWorking Capital Management: A Guide to Optimizing Current Assetsarchana_anuragiNo ratings yet

- LFAR Report for Bank BranchesDocument16 pagesLFAR Report for Bank BranchesAmrit SinghaniaNo ratings yet

- Demat Account Must ReadDocument2 pagesDemat Account Must Readaditisalvi10No ratings yet

- Financial Econometrics-Mba 451F Cia - 1 Building Research ProposalDocument4 pagesFinancial Econometrics-Mba 451F Cia - 1 Building Research ProposalPratik ChourasiaNo ratings yet

- Accounting Standards: UNIT-1Document55 pagesAccounting Standards: UNIT-1Anwar Ashraf Ashrafi100% (1)

- 08 Risk Management QuestionnaireDocument7 pages08 Risk Management QuestionnaireBhupendra ThakurNo ratings yet

- Latest Updates Developments On IRDAIDocument23 pagesLatest Updates Developments On IRDAINarashimhalu RameshNo ratings yet

- 02 Fundamentals of Business AnalysisDocument21 pages02 Fundamentals of Business AnalysisFree-Your-MindNo ratings yet

- 2022 March Supervisory Stress Test MethodologyDocument106 pages2022 March Supervisory Stress Test MethodologyAimane CAFNo ratings yet

- Flowchart RevenueDocument45 pagesFlowchart RevenueRezki PerdanaNo ratings yet

- Assignment of Management of Working Capital: TopicDocument13 pagesAssignment of Management of Working Capital: TopicDavinder Singh BanssNo ratings yet

- Sanction, Documentation and Disbursement of CreditDocument32 pagesSanction, Documentation and Disbursement of Creditrajin_rammstein100% (1)

- Poi Unit-D (2) Customer ServiceDocument16 pagesPoi Unit-D (2) Customer ServiceEHOUMAN JEAN JACQUES EBAHNo ratings yet

- Term Paper On Dhaka BankDocument29 pagesTerm Paper On Dhaka BankQuazi Aritra Reyan100% (1)

- Overview - HR Benefits AdministrationDocument2 pagesOverview - HR Benefits AdministrationSultan KhanNo ratings yet

- Business Risk Assessment - TemplateDocument4 pagesBusiness Risk Assessment - TemplateBogdan ArseneNo ratings yet

- Substantive Procedures For Sales RevenueDocument5 pagesSubstantive Procedures For Sales RevenuePubg DonNo ratings yet

- Credit RatingDocument63 pagesCredit Ratingnikhu_shuklaNo ratings yet

- Corporate Goverance - Exercise 2Document4 pagesCorporate Goverance - Exercise 2Aprille Gay FelixNo ratings yet

- BFW3841 Credit Analysis and Lening Management AssignmentDocument1 pageBFW3841 Credit Analysis and Lening Management Assignmenthi2joeyNo ratings yet

- Credit Risk Management in Icici BankDocument2 pagesCredit Risk Management in Icici Banknatashafdo50% (2)

- Wealth Management in India Challenges and StrategiesDocument10 pagesWealth Management in India Challenges and StrategieskonnectedNo ratings yet

- ILFS Group Companies - NCLT and NCLAT OrdersDocument21 pagesILFS Group Companies - NCLT and NCLAT Ordersvismita diwanNo ratings yet

- ICRRS Guidelines - BB - Version 2.0Document25 pagesICRRS Guidelines - BB - Version 2.0Optimistic EyeNo ratings yet

- Neft and RtgsDocument4 pagesNeft and RtgsmukeshkpatidarNo ratings yet

- Credit Rating of Banks As Its Impact On Their ProfitabilityDocument45 pagesCredit Rating of Banks As Its Impact On Their ProfitabilityMuhammad Ali100% (1)

- Guidance Note On Audit of BanksDocument808 pagesGuidance Note On Audit of BanksGanesh PhadatareNo ratings yet

- Hacc423 Question Bank 2021Document13 pagesHacc423 Question Bank 2021Tawanda Tatenda HerbertNo ratings yet

- 2016 12 SP Accountancy Solved 01Document8 pages2016 12 SP Accountancy Solved 01Sto BreakerNo ratings yet

- Legal Aspects: Fraud Investigations - Employee FraudDocument11 pagesLegal Aspects: Fraud Investigations - Employee FraudCorina-maria DincăNo ratings yet

- Grievance Redressal PolicyDocument3 pagesGrievance Redressal PolicyRomaldin RodriguesNo ratings yet

- Onicra Credit Rating AgencyDocument2 pagesOnicra Credit Rating AgencyAvtar SinghNo ratings yet

- Study On Investor Behaviour in Systematic Investment Plan of Mutual FundDocument7 pagesStudy On Investor Behaviour in Systematic Investment Plan of Mutual FundSurajNo ratings yet

- Asset Liability ManagementDocument24 pagesAsset Liability ManagementG117No ratings yet

- Comparative Study Auditing Between Profit & Nonprofit OrganizationsDocument52 pagesComparative Study Auditing Between Profit & Nonprofit OrganizationsNael Loay Arandas100% (7)

- Download Free EIS Videos and Questions BookDocument98 pagesDownload Free EIS Videos and Questions BookAruna RajappaNo ratings yet

- Audit Reports TypeDocument3 pagesAudit Reports Typesarah031No ratings yet

- Law011-1 MainAssessment Sem1Document4 pagesLaw011-1 MainAssessment Sem1ahadraza10% (1)

- Questionnaire - First Security Islami Bank LimitedDocument3 pagesQuestionnaire - First Security Islami Bank LimitedBishu BiswasNo ratings yet

- Financial System Questions and AnswersDocument8 pagesFinancial System Questions and AnswersWaqas KhanNo ratings yet

- Annual Report 2014Document80 pagesAnnual Report 2014khongaybytNo ratings yet

- Gartner Cool Vendors in Storage Technologies 2014Document10 pagesGartner Cool Vendors in Storage Technologies 2014Mohan ArumugamNo ratings yet

- Installation and Setup Guide For DD990 Storage SystemDocument6 pagesInstallation and Setup Guide For DD990 Storage SystemMohan ArumugamNo ratings yet

- Backup and Restore in SANDocument16 pagesBackup and Restore in SANMohan ArumugamNo ratings yet

- Backup BookDocument30 pagesBackup BookMohan ArumugamNo ratings yet

- Using The AIX Logical Volume Manager To Perform SAN Storage MigrationsDocument20 pagesUsing The AIX Logical Volume Manager To Perform SAN Storage MigrationsMohan ArumugamNo ratings yet

- Red Hat Enterprise Linux-7-7.0 Release Notes-En-USDocument89 pagesRed Hat Enterprise Linux-7-7.0 Release Notes-En-USMohan ArumugamNo ratings yet

- PuppetLabs PrimerDocument77 pagesPuppetLabs PrimerMohan ArumugamNo ratings yet

- Cloud Backup VL 2011Document32 pagesCloud Backup VL 2011Mohan ArumugamNo ratings yet

- Mathematical Modeling 10 StepsDocument1 pageMathematical Modeling 10 StepsMohan ArumugamNo ratings yet

- EGI Mainframe Vs Open SystemsDocument6 pagesEGI Mainframe Vs Open SystemsMohan ArumugamNo ratings yet

- BNYM FactSheetDocument4 pagesBNYM FactSheetMohan ArumugamNo ratings yet

- Sample Storage Network Config DiagramDocument1 pageSample Storage Network Config DiagramMohan ArumugamNo ratings yet

- HDS Software Product Overview TrueDocument2 pagesHDS Software Product Overview TrueMohan ArumugamNo ratings yet

- Aix Online Migration PDFDocument6 pagesAix Online Migration PDFMohan ArumugamNo ratings yet

- 9092 - Tivoli Flashcopy Manager Update and DemonstrationDocument36 pages9092 - Tivoli Flashcopy Manager Update and DemonstrationMohan ArumugamNo ratings yet

- AIX Presentation - NiceOneDocument67 pagesAIX Presentation - NiceOneMohan ArumugamNo ratings yet

- Nokia Technology StrategyDocument23 pagesNokia Technology StrategyMohan ArumugamNo ratings yet

- Striking Work PresoDocument9 pagesStriking Work PresoMohan ArumugamNo ratings yet

- Land Bank of the Philippines 2020 Balance SheetDocument1 pageLand Bank of the Philippines 2020 Balance SheetCharlen Relos GermanNo ratings yet

- Tally AssignmentDocument3 pagesTally AssignmentSoumya LatheyNo ratings yet

- Banc One Case Study PDF FreeDocument10 pagesBanc One Case Study PDF FreeFathima KamalNo ratings yet

- Ca Final RTP May 2014 IndiaDocument7 pagesCa Final RTP May 2014 IndiaNIKHILESH9No ratings yet

- IMD Total Public Equity Asset Class Review: April 25, 2016Document39 pagesIMD Total Public Equity Asset Class Review: April 25, 2016hNo ratings yet

- e-StatementBRImo 206701008089509 Oct2023 20231218 105159Document3 pagese-StatementBRImo 206701008089509 Oct2023 20231218 105159Nicol IrfansyahNo ratings yet

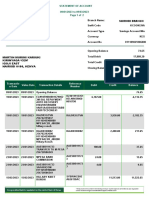

- Martin Murimi KariukiDocument2 pagesMartin Murimi KariukiKameneja LeeNo ratings yet

- 11 ACC CH 6.11 To 6.16 MemosDocument19 pages11 ACC CH 6.11 To 6.16 Memosora mashaNo ratings yet

- Partnership Formation Answer KeyDocument8 pagesPartnership Formation Answer KeyNichole Joy XielSera TanNo ratings yet

- Sem Plang Merchandising Periodic Problem With AnswersDocument21 pagesSem Plang Merchandising Periodic Problem With Answerscole sprouse100% (1)

- Tax Free ExchangeDocument4 pagesTax Free ExchangeLara YuloNo ratings yet

- Forming a Partnership with Cash and LandDocument2 pagesForming a Partnership with Cash and LandArian AmuraoNo ratings yet

- Investment PaperDocument3 pagesInvestment Paperapi-583759965No ratings yet

- Ecf 320 - Money, Banking and Financial MarketsDocument22 pagesEcf 320 - Money, Banking and Financial MarketsFredrich KztizNo ratings yet

- Ratio Analysis 3Document4 pagesRatio Analysis 3Vinay ChhedaNo ratings yet

- Hill Country CaseDocument5 pagesHill Country CaseDeepansh Kakkar100% (1)

- Opportunities and Challenges of E - Payment System in IndiaDocument9 pagesOpportunities and Challenges of E - Payment System in IndiaSUJITH THELAPURATHNo ratings yet

- ACT Invoice March 2020Document2 pagesACT Invoice March 2020Vishnu RaajNo ratings yet

- Mutual Funds: Concept and CharacteristicsDocument179 pagesMutual Funds: Concept and CharacteristicssiddharthzalaNo ratings yet

- FFM 9 Im 13Document15 pagesFFM 9 Im 13Ernest NyangiNo ratings yet

- Accounting For Partnerships: Basic Considerations and FormationDocument22 pagesAccounting For Partnerships: Basic Considerations and FormationAj CapungganNo ratings yet

- What Is A LOT in Forex Trading - Lot Sizes ExplainedDocument23 pagesWhat Is A LOT in Forex Trading - Lot Sizes Explainedomar lakhrash100% (2)

- Sample Problems Solutions Sections 2.3 & 2.4.: R P P M A R MDocument5 pagesSample Problems Solutions Sections 2.3 & 2.4.: R P P M A R MTerry Clarice DecatoriaNo ratings yet

- Business Finance Week 1 & 2Document38 pagesBusiness Finance Week 1 & 2Myka Zoldyck100% (6)

- Lloyds Bank logo historyDocument7 pagesLloyds Bank logo historyJawad AhmedNo ratings yet

- Compound Interest Problems With Detailed SolutionsDocument11 pagesCompound Interest Problems With Detailed SolutionsJerle Mae ParondoNo ratings yet

- Sir Osborne Smith 01-04-1935 To 30-06-1937Document6 pagesSir Osborne Smith 01-04-1935 To 30-06-1937Chintan P. ModiNo ratings yet

- 9 - Mirovic - BolesnikovDocument15 pages9 - Mirovic - BolesnikovIvanaNo ratings yet

- Detailed Solutions To Problem 5Document3 pagesDetailed Solutions To Problem 5Maria AngelicaNo ratings yet

- INSEAD - Executive Master in Finance - CurriculumDocument17 pagesINSEAD - Executive Master in Finance - CurriculumJM KoffiNo ratings yet