You might also like

- Consumer Protection Bureau DC Appeals Court DecisionDocument110 pagesConsumer Protection Bureau DC Appeals Court DecisionGintautas Dumcius100% (1)

- California Civil Procedure Demurrers GuideDocument45 pagesCalifornia Civil Procedure Demurrers GuideDiane SternNo ratings yet

- CCP 770.020 - ID of Persons in Chain of TitleDocument3 pagesCCP 770.020 - ID of Persons in Chain of TitleDiane SternNo ratings yet

- 2015-6-29 Winslow ORDER Murrillo 012492-12Document7 pages2015-6-29 Winslow ORDER Murrillo 012492-12Diane SternNo ratings yet

- Format Noticed MotionsDocument83 pagesFormat Noticed MotionsDiane Stern100% (1)

- HTTP WWW - Joevpa.com Boardwhofired Sht1 MailingDocument8 pagesHTTP WWW - Joevpa.com Boardwhofired Sht1 MailingDiane SternNo ratings yet

- Mers and Merscorp Agree To A Cease and Desist Order - Occ Involved - 4-13-2011Document31 pagesMers and Merscorp Agree To A Cease and Desist Order - Occ Involved - 4-13-201183jjmack100% (7)

- The Supreme Court of California BookletDocument70 pagesThe Supreme Court of California BookletDiane SternNo ratings yet

- The Supreme Court of California BookletDocument70 pagesThe Supreme Court of California BookletDiane SternNo ratings yet

- HTTP WWW - Joevpa.com Boardwhofired Sht2Document8 pagesHTTP WWW - Joevpa.com Boardwhofired Sht2Diane SternNo ratings yet

- 2010 CA Judges HDBKDocument8 pages2010 CA Judges HDBKDiane SternNo ratings yet

- CH 12 Noticed MotionsDocument83 pagesCH 12 Noticed MotionsDiane SternNo ratings yet

- MERS Announcement No 2011-01 16 Feb 2011Document2 pagesMERS Announcement No 2011-01 16 Feb 2011William A. Roper Jr.100% (1)

- Latin Phrases List (FullDocument154 pagesLatin Phrases List (FullDiane SternNo ratings yet

- HTTP WWW - Joevpa.com Boardwhofired Sht1 MailingDocument8 pagesHTTP WWW - Joevpa.com Boardwhofired Sht1 MailingDiane SternNo ratings yet

- Read Read 2nd Circuit Pro Se Appeal Packet With Forms 2dca-Shm-AllDocument108 pagesRead Read 2nd Circuit Pro Se Appeal Packet With Forms 2dca-Shm-AllDiane SternNo ratings yet

- Latin Phrases List (FullDocument154 pagesLatin Phrases List (FullDiane SternNo ratings yet

- 2014-July Ch. 23 DemurrersDocument58 pages2014-July Ch. 23 DemurrersDiane Stern100% (1)

- CCP 527. Injunction TimelinesDocument40 pagesCCP 527. Injunction TimelinesDiane SternNo ratings yet

- CCP ch3 Summons (412.10 - 412.30Document2 pagesCCP ch3 Summons (412.10 - 412.30Diane SternNo ratings yet

- CA Copyrights and Patents - AspDocument8 pagesCA Copyrights and Patents - AspDiane SternNo ratings yet

- AHMSI Table of ContentsDocument4 pagesAHMSI Table of ContentsDiane SternNo ratings yet

- CA Citizen Rights - AspDocument10 pagesCA Citizen Rights - AspDiane SternNo ratings yet

- CA Civil Code trustee substitutionDocument3 pagesCA Civil Code trustee substitutionDiane SternNo ratings yet

- CA Civil Code trustee substitutionDocument3 pagesCA Civil Code trustee substitutionDiane SternNo ratings yet

- Qwikie 2924.12 2924.17Document2 pagesQwikie 2924.12 2924.17Diane SternNo ratings yet

- CCC 2924 L & L eDocument1 pageCCC 2924 L & L eDiane SternNo ratings yet

- CCP ch3 Summons (412.10 - 412.30Document2 pagesCCP ch3 Summons (412.10 - 412.30Diane SternNo ratings yet

- California Mortgage Law - Notice of Default RequirementsDocument1 pageCalifornia Mortgage Law - Notice of Default RequirementsDiane SternNo ratings yet

- CCP 527. Injunction TimelinesDocument40 pagesCCP 527. Injunction TimelinesDiane SternNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cost of Capital Capital Structure Dividend ProblemsDocument26 pagesCost of Capital Capital Structure Dividend Problemssalehin19690% (1)

- Fa2 Tut 5Document5 pagesFa2 Tut 5Truong Thi Ha Trang 1KT-19No ratings yet

- Triple B BondsDocument2 pagesTriple B BondsChauhan SumitNo ratings yet

- Cease and DesistDocument6 pagesCease and DesistKNOWLEDGE SOURCE100% (2)

- Corporation, Annum That Was Expressly Stipulated in The Sales Invoices. The Court Held ThatDocument10 pagesCorporation, Annum That Was Expressly Stipulated in The Sales Invoices. The Court Held ThatCamille DuterteNo ratings yet

- CBO Hatch Letter On Financial Transaction TaxDocument6 pagesCBO Hatch Letter On Financial Transaction TaxMilton RechtNo ratings yet

- Multi-Purpose Loan (MPL) Application FormDocument16 pagesMulti-Purpose Loan (MPL) Application FormPablito BeringNo ratings yet

- PArtDocument6 pagesPArtMay DabuNo ratings yet

- MR Vasanth Rao Bangalore MetroDocument16 pagesMR Vasanth Rao Bangalore MetrotakiasNo ratings yet

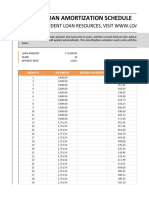

- Calculate student loan paymentsDocument18 pagesCalculate student loan paymentsIsmail UsmanNo ratings yet

- Coursebook Answers: Business in ContextDocument7 pagesCoursebook Answers: Business in ContextImran Ali75% (8)

- Foreclosure Reform Analysis FINALDocument23 pagesForeclosure Reform Analysis FINALSouthern California Public RadioNo ratings yet

- B5 PsafDocument926 pagesB5 PsafIRIBHOGBE OSAJIENo ratings yet

- Dr. Mohd Bahroddin Bin Badri - Credit Guarantee Kafalah Bi Al-Ujrah2Document25 pagesDr. Mohd Bahroddin Bin Badri - Credit Guarantee Kafalah Bi Al-Ujrah2solehanaNo ratings yet

- Estimating Spot Rates and FWD Rates (Using Bootstrapping Method)Document3 pagesEstimating Spot Rates and FWD Rates (Using Bootstrapping Method)9210490991No ratings yet

- Pablo P. Garcia V. Yolanda Valdez Villar G.R. No. 158891, June 27, 2012, J. Leonardo-DecastroDocument2 pagesPablo P. Garcia V. Yolanda Valdez Villar G.R. No. 158891, June 27, 2012, J. Leonardo-DecastroBianca Nerizza A. Infantado IINo ratings yet

- QRatiosDocument5 pagesQRatiosstriderjebby6512No ratings yet

- Nippon India Growth Fund: (Mid Cap Fund-An Open Ended Equity Scheme Predominantly Investing in Mid Cap Stocks)Document29 pagesNippon India Growth Fund: (Mid Cap Fund-An Open Ended Equity Scheme Predominantly Investing in Mid Cap Stocks)Saif MansooriNo ratings yet

- Just The Faqs:: Answers Common Questions About Reverse MortgagesDocument16 pagesJust The Faqs:: Answers Common Questions About Reverse MortgagesValerie VanBooven RN BSNNo ratings yet

- Acctg 115 - CH 10 SolutionsDocument22 pagesAcctg 115 - CH 10 SolutionschinmusicianNo ratings yet

- Loan Application Form - With Pretermination - 05092019Document2 pagesLoan Application Form - With Pretermination - 05092019Ki KoNo ratings yet

- Indiana Loan Broker AgreementDocument2 pagesIndiana Loan Broker AgreementalokprasadNo ratings yet

- Investment Banking - Course Notes PDFDocument42 pagesInvestment Banking - Course Notes PDFDr. Vishal GhagNo ratings yet

- Islamic Finance Book - 2nd Edition PDFDocument140 pagesIslamic Finance Book - 2nd Edition PDFMhmdNo ratings yet

- Samplepractice Exam 9 April 2017 Questions and AnswersDocument24 pagesSamplepractice Exam 9 April 2017 Questions and AnswersAngel Queen Marino SamoragaNo ratings yet

- Fernandez VsDocument56 pagesFernandez VsfirstNo ratings yet

- Loan Syndication For Domestic Borrowings in Merchant BankingDocument24 pagesLoan Syndication For Domestic Borrowings in Merchant BankingKinjal ShahNo ratings yet

- Service Concession AgreementDocument31 pagesService Concession AgreementvorapratikNo ratings yet

- Term Paper On APEX FOODS LTD. Samina Sultana-8451Document45 pagesTerm Paper On APEX FOODS LTD. Samina Sultana-8451pranta senNo ratings yet

- 10 Financial Principles That Are BiblicalDocument5 pages10 Financial Principles That Are BiblicalLuis JohnsonNo ratings yet