You might also like

- Money Theories, Money and Monetary PolicyDocument33 pagesMoney Theories, Money and Monetary PolicyFhremond ApoleNo ratings yet

- Pepsi-Cola Products Philippines Inc. (Pcppi) : Fhremond C. ApoleDocument7 pagesPepsi-Cola Products Philippines Inc. (Pcppi) : Fhremond C. ApoleFhremond ApoleNo ratings yet

- FINMANDocument30 pagesFINMANFhremond ApoleNo ratings yet

- 2009 EmployerSurveyDocument10 pages2009 EmployerSurveyFhremond ApoleNo ratings yet

- Areas of ConsiderationDocument1 pageAreas of ConsiderationFhremond ApoleNo ratings yet

- IntroDocument1 pageIntroFhremond ApoleNo ratings yet

- VII. Marketing Strategy: A.) SegmentationDocument2 pagesVII. Marketing Strategy: A.) SegmentationFhremond ApoleNo ratings yet

- Bodies of WaterDocument4 pagesBodies of WaterFhremond ApoleNo ratings yet

- Big BankDocument1 pageBig BankFhremond ApoleNo ratings yet

- Multiple Choice QuestionsDocument11 pagesMultiple Choice QuestionsFhremond Apole75% (8)

- TheoriesDocument6 pagesTheoriesFhremond ApoleNo ratings yet

- Money Andthe EconomyDocument8 pagesMoney Andthe EconomyFhremond ApoleNo ratings yet

- Bodies of WaterDocument4 pagesBodies of WaterFhremond ApoleNo ratings yet

- The Nervous SystemDocument38 pagesThe Nervous SystemFhremond ApoleNo ratings yet

- AcTG TestDocument8 pagesAcTG TestFhremond ApoleNo ratings yet

- GR 172087Document16 pagesGR 172087Fhremond ApoleNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Understanding Zara's Supply ChainDocument7 pagesUnderstanding Zara's Supply ChainDYPUSM WECNo ratings yet

- TENDER RFX NO. 2122100065 Supply of Skilled Manpower Services For Works in Generation DivisionDocument3 pagesTENDER RFX NO. 2122100065 Supply of Skilled Manpower Services For Works in Generation Divisionxafajat881No ratings yet

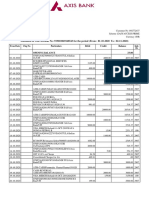

- Statement of Axis Account No:919010069168543 For The Period (From: 01-10-2020 To: 02-11-2020)Document2 pagesStatement of Axis Account No:919010069168543 For The Period (From: 01-10-2020 To: 02-11-2020)minniNo ratings yet

- Acct Statement - XX6717 - 18072023Document11 pagesAcct Statement - XX6717 - 18072023Mevaram GurjarNo ratings yet

- HG6145F GPON Optical Network Terminal Product Manual ADocument38 pagesHG6145F GPON Optical Network Terminal Product Manual AAtila RaphaelNo ratings yet

- Franklin PDFDocument48 pagesFranklin PDFkermech21607No ratings yet

- Account Statement: Date Value Date Description Cheque Deposit Withdrawal BalanceDocument2 pagesAccount Statement: Date Value Date Description Cheque Deposit Withdrawal Balanceomm123No ratings yet

- Non-Marketable Financial Assets: Bank DepositsDocument8 pagesNon-Marketable Financial Assets: Bank DepositsDhruv MishraNo ratings yet

- Contentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFDocument4 pagesContentitemfile Clakzz57bxlrw0a21yjksjcx8 PDFJoseph OndariNo ratings yet

- Account Statements-AprDocument2 pagesAccount Statements-AprCAT ClusterNo ratings yet

- CCNA 200 Part 1Document406 pagesCCNA 200 Part 1Wallace LiraNo ratings yet

- Throughput of Inbound Applications (MBPS) : Applications (Exinda-Heves) Feb 16 2022 12:00am - Feb 17 2022 12:00amDocument6 pagesThroughput of Inbound Applications (MBPS) : Applications (Exinda-Heves) Feb 16 2022 12:00am - Feb 17 2022 12:00amLuis FernandoNo ratings yet

- Loan Agreement Document of $100,000.00 USDDocument3 pagesLoan Agreement Document of $100,000.00 USDUniverse Loan Company LimtedNo ratings yet

- Geeta Sy Fee ReceiptDocument1 pageGeeta Sy Fee Receiptrocky handsomeNo ratings yet

- T Rec K.26 200804 I!!pdf eDocument8 pagesT Rec K.26 200804 I!!pdf ejmrs7322No ratings yet

- Class 9 and 11-ptm CircularDocument2 pagesClass 9 and 11-ptm CircularRishabh GargNo ratings yet

- This Document Has 881 PagesDocument17 pagesThis Document Has 881 Pagespadmakar tripathiNo ratings yet

- PowerPoint Presentation On Inventory ControlDocument41 pagesPowerPoint Presentation On Inventory ControlSafwan Shaikh100% (2)

- Chapter 13: Basics of Commercial BankingDocument2 pagesChapter 13: Basics of Commercial BankingShane Tabunggao100% (1)

- Handyman Contractor Invoice TemplateDocument2 pagesHandyman Contractor Invoice TemplateStephanies GonzalezNo ratings yet

- Form12BB R539 Proof Submission Form PDFDocument4 pagesForm12BB R539 Proof Submission Form PDFSiva ThotaNo ratings yet

- Fortigate 2600f SeriesDocument6 pagesFortigate 2600f SeriesAzhar HussainNo ratings yet

- Bizmanualz Accounting Policies and Procedures SampleDocument8 pagesBizmanualz Accounting Policies and Procedures SamplePaulo LindgrenNo ratings yet

- Chapter 1-QuizDocument27 pagesChapter 1-QuizJpzelle100% (1)

- Product and Distribution StrategiesDocument37 pagesProduct and Distribution Strategiesmonel_24671No ratings yet

- 9 Feb 2021 FoodDocument2 pages9 Feb 2021 FoodRakesh ThalorNo ratings yet

- Net Pacific Inc. Organizational Structure: Evelyn Morales Lito Tac-AnDocument1 pageNet Pacific Inc. Organizational Structure: Evelyn Morales Lito Tac-AnPatrick PenachosNo ratings yet

- Basic Reconciliation StatementsDocument41 pagesBasic Reconciliation StatementsBeverly EroyNo ratings yet

- Benefit Verification LetterDocument4 pagesBenefit Verification LetterDonna BridgesNo ratings yet

- UGBS 205 Fundamentals of Accounting Methods: Week 8 - Bank Reconciliation StatementDocument16 pagesUGBS 205 Fundamentals of Accounting Methods: Week 8 - Bank Reconciliation StatementYaw Baah-BarimahNo ratings yet