You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lechner V.tri County Rescue, Inc. Complaint 11.18.15 PDFDocument14 pagesLechner V.tri County Rescue, Inc. Complaint 11.18.15 PDFWIS Digital News StaffNo ratings yet

- Mandela: His 8 Lessons of Leadership by RICHARD STENGEL WednesdayDocument56 pagesMandela: His 8 Lessons of Leadership by RICHARD STENGEL Wednesdayimamhossain50% (2)

- Human Factors: (Pear Model)Document14 pagesHuman Factors: (Pear Model)Eckson FernandezNo ratings yet

- Ra 10149 PDFDocument14 pagesRa 10149 PDFCon PuNo ratings yet

- Clinton 6Document563 pagesClinton 6MagaNWNo ratings yet

- Sayings of Ali Ibn Abi TalibDocument9 pagesSayings of Ali Ibn Abi TalibJonathan DubéNo ratings yet

- Rogelio Engada, vs. Hon. Court of Appeals, and People of The Philippines, Rogelio Engada Hon. Court of Appeals, and People of The PhilippinesDocument3 pagesRogelio Engada, vs. Hon. Court of Appeals, and People of The Philippines, Rogelio Engada Hon. Court of Appeals, and People of The PhilippinesRenée Kristen CortezNo ratings yet

- Supreme Court Reports (2012) 8 S.C.R. 652 (2012) 8 S.C.R. 651Document147 pagesSupreme Court Reports (2012) 8 S.C.R. 652 (2012) 8 S.C.R. 651Sharma SonuNo ratings yet

- Summary - The Discipline of TeamsDocument2 pagesSummary - The Discipline of Teamsjkgonzalez67% (3)

- PS Early Childhood Education PDFDocument69 pagesPS Early Childhood Education PDFHanafi MamatNo ratings yet

- 11go Coc CoeDocument2 pages11go Coc CoePatrick Ignacio83% (48)

- Dudjoms Prayer For Recognising Faults 2 PDFDocument22 pagesDudjoms Prayer For Recognising Faults 2 PDFThiagoFerrettiNo ratings yet

- Bay Al InahDocument12 pagesBay Al InahAyu SetzianiNo ratings yet

- Pineda vs. CADocument15 pagesPineda vs. CAAji AmanNo ratings yet

- NOTICE by AFF of Relinquisment of Resident Agency Status Howard Griswold 4 14 13Document3 pagesNOTICE by AFF of Relinquisment of Resident Agency Status Howard Griswold 4 14 13Gemini Research100% (1)

- DLL For PhiloDocument11 pagesDLL For Philosmhilez100% (1)

- Transplantation of Human Organs and Tissues Act, 1994. ("Tissues" Added in 2011 Amendment) The Legal Framework in IndiaDocument10 pagesTransplantation of Human Organs and Tissues Act, 1994. ("Tissues" Added in 2011 Amendment) The Legal Framework in IndiasamridhiNo ratings yet

- Badillo vs. Court of Appeals, 555 SCRA 435 (2008) - FulltextDocument7 pagesBadillo vs. Court of Appeals, 555 SCRA 435 (2008) - FulltextNyla0% (1)

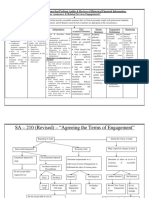

- 53 Standards On Auditing Flowcharts PDFDocument22 pages53 Standards On Auditing Flowcharts PDFSaloni100% (1)

- Crim Soc Set B 2010Document12 pagesCrim Soc Set B 2010Claudine Gubia-on PuyaoNo ratings yet

- Questionnaire (For Printing)Document4 pagesQuestionnaire (For Printing)Anonymous VOiMiOhAr40% (5)

- Drug Aproval Process in IndiaDocument3 pagesDrug Aproval Process in IndiaSamit BisenNo ratings yet

- Housing Standards Act 2908Document18 pagesHousing Standards Act 2908tarisaiNo ratings yet

- SGND Khalsa College: MR Samarpit Kalra Iiird Year (B) Roll No.-028Document46 pagesSGND Khalsa College: MR Samarpit Kalra Iiird Year (B) Roll No.-028Sagar Kapoor100% (3)

- Law On Natural Resources ReviewerDocument130 pagesLaw On Natural Resources ReviewerAsh CampiaoNo ratings yet

- Brand Collaboration Agreement: (Labevande)Document3 pagesBrand Collaboration Agreement: (Labevande)Richard Williams0% (1)

- Motion To DismissDocument26 pagesMotion To DismissAlyssa Roberts100% (1)

- Time As An Essence of ContractsDocument20 pagesTime As An Essence of ContractsAyushi Agrawal100% (1)

- Chapter 4 Palliative CareDocument21 pagesChapter 4 Palliative CareEINSTEIN2DNo ratings yet

- NYPD: Guidelines For Use of Force in New York CityDocument89 pagesNYPD: Guidelines For Use of Force in New York CityNewsweekNo ratings yet