You might also like

- Ieee Conference Paper TemplateDocument4 pagesIeee Conference Paper TemplateAnonymous Q0KzFR2iNo ratings yet

- Senate BillDocument17 pagesSenate BillAnonymous Q0KzFR2iNo ratings yet

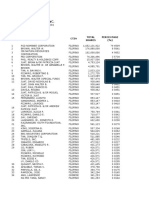

- 03 - 31 - 2017 - Quarterly Top 100 StockholdersDocument7 pages03 - 31 - 2017 - Quarterly Top 100 StockholdersAnonymous Q0KzFR2iNo ratings yet

- Spaced Repetition PDFDocument18 pagesSpaced Repetition PDFAnonymous Q0KzFR2iNo ratings yet

- Overview of Asset Allocation PlanDocument117 pagesOverview of Asset Allocation PlanAnonymous Q0KzFR2iNo ratings yet

- IEEE Conference Paper TemplateDocument2 pagesIEEE Conference Paper Templateganapathy2010svNo ratings yet

- 2017checklist FinancingCompanyDocument1 page2017checklist FinancingCompanyAnonymous Q0KzFR2iNo ratings yet

- Teaching Space Law in Law Schools, A Necessary Challenge in The Developing CountriesDocument7 pagesTeaching Space Law in Law Schools, A Necessary Challenge in The Developing CountriesAnonymous Q0KzFR2iNo ratings yet

- MacArthur's Daring Rescue from the PhilippinesDocument1 pageMacArthur's Daring Rescue from the PhilippinesAnonymous Q0KzFR2iNo ratings yet

- Examining Anonymous Internet Speech - Why The Pols Cannot ControlDocument29 pagesExamining Anonymous Internet Speech - Why The Pols Cannot ControlAnonymous Q0KzFR2iNo ratings yet

- Locus StandiDocument4 pagesLocus StandiAnonymous Q0KzFR2iNo ratings yet

- Taxation of Repurchase AgreementsDocument5 pagesTaxation of Repurchase AgreementsAnonymous Q0KzFR2iNo ratings yet

- Bitcoin and Cryptocurrency Regulation in The PhilippinesDocument9 pagesBitcoin and Cryptocurrency Regulation in The PhilippinesAnonymous Q0KzFR2iNo ratings yet

- Short Sale of StocksDocument31 pagesShort Sale of StocksAnonymous Q0KzFR2iNo ratings yet

- Deposit SubstitutesDocument35 pagesDeposit SubstitutesAnonymous Q0KzFR2iNo ratings yet

- Corporate NationalityDocument33 pagesCorporate NationalityAnonymous Q0KzFR2iNo ratings yet

- Swaps Betting Law Jib FLDocument4 pagesSwaps Betting Law Jib FLAnonymous Q0KzFR2iNo ratings yet

- Evidence Regalado Book OutlineDocument72 pagesEvidence Regalado Book OutlineAnonymous Q0KzFR2iNo ratings yet

- Bureau of Internal Revenue: Deficiency Tax AssessmentDocument9 pagesBureau of Internal Revenue: Deficiency Tax AssessmentXavier Cajimat UrbanNo ratings yet

- Republic Act 7718Document42 pagesRepublic Act 7718PTIC London100% (2)

- 1987 Philippine ConstitutionDocument35 pages1987 Philippine ConstitutionAnonymous Q0KzFR2iNo ratings yet

- BUSLA101 Contract of MarriageDocument4 pagesBUSLA101 Contract of MarriageAnonymous Q0KzFR2iNo ratings yet

- News ClippingDocument1 pageNews ClippingAnonymous Q0KzFR2iNo ratings yet

- The Five Best Anime of 2014Document20 pagesThe Five Best Anime of 2014Anonymous Q0KzFR2iNo ratings yet

- Evidence Rules and PrinciplesDocument37 pagesEvidence Rules and Principlesdaboy15No ratings yet

- SSRN Id2445601sDocument12 pagesSSRN Id2445601sAnonymous Q0KzFR2iNo ratings yet

- SSRN Id2293870Document43 pagesSSRN Id2293870Anonymous Q0KzFR2iNo ratings yet

- News ClippingDocument1 pageNews ClippingAnonymous Q0KzFR2iNo ratings yet

- Tax ReviewerDocument53 pagesTax ReviewerAllen LiberatoNo ratings yet

- Government Procurement Reform Act SummaryDocument24 pagesGovernment Procurement Reform Act SummaryAnonymous Q0KzFR2i0% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)