You might also like

- Compromise PenaltiesDocument2 pagesCompromise PenaltiesCkey ArNo ratings yet

- BIR RULING (DA - (C-168) 519-08) - Liquidated DamagesDocument8 pagesBIR RULING (DA - (C-168) 519-08) - Liquidated Damagesjohn allen MarillaNo ratings yet

- BirDocument8 pagesBirDominique VasalloNo ratings yet

- RR 4-86Document2 pagesRR 4-86Mico Maagma CarpioNo ratings yet

- RR 2-98Document85 pagesRR 2-98restless11No ratings yet

- Joint Venture-TaxabilityDocument10 pagesJoint Venture-TaxabilitySyzian ExonyryNo ratings yet

- Ramo 1-2000Document177 pagesRamo 1-2000Kris Calabia100% (2)

- Best Evidence Obtainable in The Realm of The Phil. Tax CodeDocument4 pagesBest Evidence Obtainable in The Realm of The Phil. Tax Codehenzencamero100% (1)

- RMC 74-99 Treatment of Peza Sales and VatDocument4 pagesRMC 74-99 Treatment of Peza Sales and VatRester John NonatoNo ratings yet

- Sample PANDocument5 pagesSample PANArmie Lyn Simeon100% (1)

- BIR Ruling (DA-005-07) (Travel Agencies) PDFDocument4 pagesBIR Ruling (DA-005-07) (Travel Agencies) PDFAl Marvin0% (1)

- Bir Ruling No. 1243-18 - JvsDocument3 pagesBir Ruling No. 1243-18 - Jvsjohn allen MarillaNo ratings yet

- Trade and Cash Discount Practices in The PhilippinesDocument2 pagesTrade and Cash Discount Practices in The PhilippinesAileen Dela CruzNo ratings yet

- 20005rmo 10-05Document16 pages20005rmo 10-05Cheng OlayvarNo ratings yet

- BIR Ruling DA - C-018 075-10Document2 pagesBIR Ruling DA - C-018 075-10Mark Lord Morales BumagatNo ratings yet

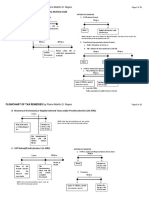

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- OM No. 2018-04-03Document2 pagesOM No. 2018-04-03Christian Albert HerreraNo ratings yet

- BusinessWorld - Marinated Meat and Fish Products No Longer VAT-exemptDocument2 pagesBusinessWorld - Marinated Meat and Fish Products No Longer VAT-exemptPJ NavarroNo ratings yet

- BIR Ruling No. 010-02 - 30 Day Period For Filing of Short Period Return by Absorbed CorporationDocument4 pagesBIR Ruling No. 010-02 - 30 Day Period For Filing of Short Period Return by Absorbed Corporationliz kawiNo ratings yet

- Requirements To Be Accredited As Tax AgentDocument3 pagesRequirements To Be Accredited As Tax AgentAvril Reina0% (1)

- RR No. 11-2018Document47 pagesRR No. 11-2018Micah Adduru - RoblesNo ratings yet

- Sworn StatementDocument2 pagesSworn Statementisabelle100% (1)

- Bir Waiver of Defense of PrescriptionDocument3 pagesBir Waiver of Defense of PrescriptionCha Ancheta CabigasNo ratings yet

- Integrity Pledge For Certified Public AccountantsDocument1 pageIntegrity Pledge For Certified Public AccountantsromabooNo ratings yet

- RR 12-1999Document21 pagesRR 12-1999anorith8867% (6)

- BIR - Affidavit of Preservation of Working PapersDocument1 pageBIR - Affidavit of Preservation of Working PapersLimuel Balestramon RazonalesNo ratings yet

- Ord, 24-93 Taguig Revenue CodeDocument219 pagesOrd, 24-93 Taguig Revenue CodeAldrinmarkquintana50% (2)

- RR 15-2010 Additional Notes To Financial StatementsDocument9 pagesRR 15-2010 Additional Notes To Financial StatementsMary Grace Caguioa AgasNo ratings yet

- Tax Remedies Flowchart (Revised)Document6 pagesTax Remedies Flowchart (Revised)GersonGamas0% (1)

- BIR Ruling (DA - (C-066) 228-09) - Capital Infusion in The Form of APIC Not Subject To Donor's TaxDocument8 pagesBIR Ruling (DA - (C-066) 228-09) - Capital Infusion in The Form of APIC Not Subject To Donor's TaxJerwin Dave100% (1)

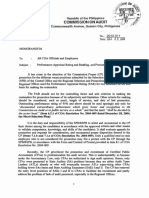

- COMMISSION ON AUDIT MEMORANDUM NO. 2012-011 Performance Appraisal Rating (COA - M2012-011)Document2 pagesCOMMISSION ON AUDIT MEMORANDUM NO. 2012-011 Performance Appraisal Rating (COA - M2012-011)Prateik Ryuki100% (1)

- BIR Revenue Regulations No. 2-98Document93 pagesBIR Revenue Regulations No. 2-98Maan EspinosaNo ratings yet

- Ramo 1-2019Document74 pagesRamo 1-2019Donato Vergara IIINo ratings yet

- DST On Lease AgreementsDocument1 pageDST On Lease Agreementsrachellemae10No ratings yet

- Taxation of Non-Bank Financial Intermediaries PhilippinesDocument12 pagesTaxation of Non-Bank Financial Intermediaries Philippinesjosiah9_5No ratings yet

- Rmo 21-2000Document15 pagesRmo 21-2000jef comendadorNo ratings yet

- Expanded Withholding Taxes On Government Income PaymentsDocument172 pagesExpanded Withholding Taxes On Government Income PaymentsBien Bowie A. CortezNo ratings yet

- RR 2-98Document136 pagesRR 2-98hizelaryaNo ratings yet

- BIR Rulings On Change of Useful LifeDocument6 pagesBIR Rulings On Change of Useful LifeCarlota Nicolas VillaromanNo ratings yet

- Attachment To State Tax Including Cpa Cert PDFDocument4 pagesAttachment To State Tax Including Cpa Cert PDFBradNo ratings yet

- RemediesDocument45 pagesRemediesCzarina100% (1)

- Tax Alert BIR Ruling 142-2011Document3 pagesTax Alert BIR Ruling 142-2011Ia Bolos0% (1)

- How To Compute DSTDocument6 pagesHow To Compute DSTShayne AgustinNo ratings yet

- Sample Audited Financial Statements For Sole Proprietorship PDFDocument16 pagesSample Audited Financial Statements For Sole Proprietorship PDFKristen100% (3)

- BIR Revenue Regulation No. 02-98 Dated 17 April 1998Document74 pagesBIR Revenue Regulation No. 02-98 Dated 17 April 1998wally_wanda93% (14)

- Taxation - 7 Tax Remedies Under LGCDocument3 pagesTaxation - 7 Tax Remedies Under LGCcmv mendozaNo ratings yet

- Sec Reportorial RequirementsDocument2 pagesSec Reportorial RequirementsAnonymous qDb8S3koENo ratings yet

- Withholding Tax Reviewer CompiledDocument14 pagesWithholding Tax Reviewer CompiledAcademic Stuff100% (1)

- Professional Regulation Commission Board of Accountancy Quality Accreditation Checklist Pursuant of ORB Resolution No.Document1 pageProfessional Regulation Commission Board of Accountancy Quality Accreditation Checklist Pursuant of ORB Resolution No.Gualberto Plasos67% (3)

- Philippine Institute of Certified Public Accountants (PICPA)Document2 pagesPhilippine Institute of Certified Public Accountants (PICPA)Jeaneth Dela Pena Carnicer100% (1)

- 1.) Who Are Eligible To Register As Bmbes?: AnswerDocument6 pages1.) Who Are Eligible To Register As Bmbes?: AnswerHazel Seguerra BicadaNo ratings yet

- BIR Audit ManualDocument89 pagesBIR Audit ManualRivera RwlrNo ratings yet

- GCRO Top230 PG April2019Document223 pagesGCRO Top230 PG April2019Edmerl AbadNo ratings yet

- RR 12-99 Full TextDocument5 pagesRR 12-99 Full TextErmawoo100% (2)

- Bir Ruling (Da - (C-005) 023-08)Document4 pagesBir Ruling (Da - (C-005) 023-08)Marlene TongsonNo ratings yet

- BIR Ruling (DA-335) 815-09Document5 pagesBIR Ruling (DA-335) 815-09Ren Mar CruzNo ratings yet

- Tax Alert - 2005 - OctDocument11 pagesTax Alert - 2005 - OctKarina PulidoNo ratings yet

- Justice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)Document4 pagesJustice Teresita Leonardo-De Castro Cases (2008-2015) : Scope and Limitations of Taxation (Constitutional Limitations)jimNo ratings yet

- Cir V. Solidbank Corporation: FactsDocument3 pagesCir V. Solidbank Corporation: FactsJustine Jay Casas LopeNo ratings yet

- Taxation Law Pre-Bar Notes 2017-SupplementalDocument7 pagesTaxation Law Pre-Bar Notes 2017-SupplementalPnix HortinelaNo ratings yet

- Corporation Code Case DoctrineDocument70 pagesCorporation Code Case DoctrineArchie Guevarra100% (1)

- 2007 Revised Rules in The Availment of Income Tax HolidayDocument23 pages2007 Revised Rules in The Availment of Income Tax HolidayArchie Guevarra100% (1)

- CTA AC No. 40 (Honest Services V City of Makati) (Situs of Local Taxes)Document15 pagesCTA AC No. 40 (Honest Services V City of Makati) (Situs of Local Taxes)Archie GuevarraNo ratings yet

- CTA EB No. 1117 Liquigaz V CIR (Interest)Document60 pagesCTA EB No. 1117 Liquigaz V CIR (Interest)Archie GuevarraNo ratings yet

- CreditTrans - Article 1953 Republic V GrijaldoDocument1 pageCreditTrans - Article 1953 Republic V GrijaldoArchie GuevarraNo ratings yet

- Overseas V CorderoDocument7 pagesOverseas V CorderoArchie GuevarraNo ratings yet

- GR No. 168129 (CIR V Phil Health Care) (Nonretroactivity)Document12 pagesGR No. 168129 (CIR V Phil Health Care) (Nonretroactivity)Archie GuevarraNo ratings yet

- RR 16-05 - AmendmentsDocument39 pagesRR 16-05 - AmendmentsArchie GuevarraNo ratings yet

- Negotiable Instruments - AnnotatedDocument54 pagesNegotiable Instruments - AnnotatedArchie GuevarraNo ratings yet

- GR No. 195580 (Narra Nickel v. Redmont) (Grandfather Rule)Document43 pagesGR No. 195580 (Narra Nickel v. Redmont) (Grandfather Rule)Archie GuevarraNo ratings yet

- RR 2-98 - AmendmentsDocument196 pagesRR 2-98 - AmendmentsArchie Guevarra100% (1)

- Book 1Document2 pagesBook 1Archie GuevarraNo ratings yet

- BIR Ruling (DA-152-07) (Restricted Stock Unit Plan)Document4 pagesBIR Ruling (DA-152-07) (Restricted Stock Unit Plan)Archie GuevarraNo ratings yet

- Logic Term Paper - ObietaDocument36 pagesLogic Term Paper - ObietaArchie Guevarra100% (1)

- Good Governance - Take Home ExamDocument3 pagesGood Governance - Take Home ExamArchie GuevarraNo ratings yet

- Grace Corp Audited FSDocument17 pagesGrace Corp Audited FSArchie Guevarra90% (10)

- Good Governance - Take Home ExamDocument3 pagesGood Governance - Take Home ExamArchie GuevarraNo ratings yet

- SolutionDocument5 pagesSolutionArchie GuevarraNo ratings yet

- Painting: 22.1 Types of PaintsDocument8 pagesPainting: 22.1 Types of PaintsRosy RoseNo ratings yet

- DGA Furan AnalysisDocument42 pagesDGA Furan AnalysisShefian Md Dom100% (10)

- Indiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)Document2 pagesIndiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)abramsdcNo ratings yet

- Denso - History PDFDocument5 pagesDenso - History PDFVenkateswaran KrishnamurthyNo ratings yet

- RELATIVE CLAUSES 1º Bachillerato and KeyDocument3 pagesRELATIVE CLAUSES 1º Bachillerato and Keyrapitanoroel0% (2)

- Shape It! SB 1Document13 pagesShape It! SB 1Ass of Fire50% (6)

- PDF RR Grade Sep ProjectsDocument46 pagesPDF RR Grade Sep ProjectsjunqiangdongNo ratings yet

- Tesla - Electric Railway SystemDocument3 pagesTesla - Electric Railway SystemMihai CroitoruNo ratings yet

- OD - SAP Connector UtilityDocument22 pagesOD - SAP Connector UtilityShivani SharmaNo ratings yet

- Sample Heat Sheets June 2007Document63 pagesSample Heat Sheets June 2007Nesuui MontejoNo ratings yet

- Atmosphere Study Guide 2013Document4 pagesAtmosphere Study Guide 2013api-205313794No ratings yet

- What Is An InfographicDocument4 pagesWhat Is An InfographicAryaaaNo ratings yet

- Bye Laws For MirzapurDocument6 pagesBye Laws For MirzapurUtkarsh SharmaNo ratings yet

- Meyer and Zack KM CycleDocument16 pagesMeyer and Zack KM Cyclemohdasriomar84No ratings yet

- Cavitation in Francis PDFDocument373 pagesCavitation in Francis PDFAlberto AliagaNo ratings yet

- PTEG Spoken OfficialSampleTest L5 17mar11Document8 pagesPTEG Spoken OfficialSampleTest L5 17mar11Katia LeliakhNo ratings yet

- A Modified Linear Programming Method For Distribution System ReconfigurationDocument6 pagesA Modified Linear Programming Method For Distribution System Reconfigurationapi-3697505No ratings yet

- What Is A Timer?Document12 pagesWhat Is A Timer?Hemraj Singh Rautela100% (1)

- Sip TrunkDocument288 pagesSip TrunkSayaOtanashiNo ratings yet

- Trading Book - AGDocument7 pagesTrading Book - AGAnilkumarGopinathanNairNo ratings yet

- Mechanical Power FormulaDocument9 pagesMechanical Power FormulaEzeBorjesNo ratings yet

- Antibiotic I and II HWDocument4 pagesAntibiotic I and II HWAsma AhmedNo ratings yet

- Med Error PaperDocument4 pagesMed Error Paperapi-314062228100% (1)

- General LPG Installation Guide PDFDocument60 pagesGeneral LPG Installation Guide PDFgheorghe garduNo ratings yet

- Fallas Compresor Copeland-DesbloqueadoDocument16 pagesFallas Compresor Copeland-DesbloqueadoMabo MabotecnicaNo ratings yet

- Shsa1105 - Unit-III Course MaterialsDocument58 pagesShsa1105 - Unit-III Course Materialssivanikesh bonagiriNo ratings yet

- Homework 1 Tarea 1Document11 pagesHomework 1 Tarea 1Anette Wendy Quipo Kancha100% (1)

- Cover Sheet: Online Learning and Teaching (OLT) Conference 2006, Pages Pp. 21-30Document12 pagesCover Sheet: Online Learning and Teaching (OLT) Conference 2006, Pages Pp. 21-30Shri Avinash NarendhranNo ratings yet

- I. Ifugao and Its TribeDocument8 pagesI. Ifugao and Its TribeGerard EscandaNo ratings yet

- Almutairy / Musa MR: Boarding PassDocument1 pageAlmutairy / Musa MR: Boarding PassMusaNo ratings yet

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionRating: 5 out of 5 stars5/5 (27)

- Taxes Have Consequences: An Income Tax History of the United StatesFrom EverandTaxes Have Consequences: An Income Tax History of the United StatesNo ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionFrom EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionNo ratings yet

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012From EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No ratings yet

- Decrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationFrom EverandDecrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsRating: 3.5 out of 5 stars3.5/5 (9)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Stiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills and MoreFrom EverandStiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills and MoreRating: 4.5 out of 5 stars4.5/5 (13)

- Canadian International Taxation: Income Tax Rules for ResidentsFrom EverandCanadian International Taxation: Income Tax Rules for ResidentsNo ratings yet