You might also like

- Degree of Leverage: Empirical Analysis from the Insurance SectorFrom EverandDegree of Leverage: Empirical Analysis from the Insurance SectorNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- Chapter - 3 Research Methodology 3.1 Research MethodologyDocument10 pagesChapter - 3 Research Methodology 3.1 Research MethodologySovin ChauhanNo ratings yet

- Aksujomas 03 01 05Document20 pagesAksujomas 03 01 05Rasaq MojeedNo ratings yet

- Penelitian Terdahulu 11 (Inter)Document10 pagesPenelitian Terdahulu 11 (Inter)Rofi'ah -No ratings yet

- The Effect of Current Ratio, Debt To Equity Ratio, Return On Assets On Earning Per Share (Study in Company Group of LQ45 Index Listed in Indonesia Stock Exchange 2011-2015)Document8 pagesThe Effect of Current Ratio, Debt To Equity Ratio, Return On Assets On Earning Per Share (Study in Company Group of LQ45 Index Listed in Indonesia Stock Exchange 2011-2015)ajmrdNo ratings yet

- The Impact of Financial Leverage To Profitability Study of Vehicle Companies From PakistanDocument21 pagesThe Impact of Financial Leverage To Profitability Study of Vehicle Companies From PakistanAhmad Ali100% (1)

- 65-Article Text-171-1-10-20200331Document6 pages65-Article Text-171-1-10-20200331mia muchia desdaNo ratings yet

- 1ratio Analysis of Automobile Sector For InvestmentDocument29 pages1ratio Analysis of Automobile Sector For Investmentpranab_nandaNo ratings yet

- The Influence of The Debt To Equity Ratio, Inventory Turn Over, and Current Ratio Against The Return On Equity in The Pharmaceutical Sector CompaniesDocument10 pagesThe Influence of The Debt To Equity Ratio, Inventory Turn Over, and Current Ratio Against The Return On Equity in The Pharmaceutical Sector CompaniesVincent SusantoNo ratings yet

- Financial Management Research ProjectDocument5 pagesFinancial Management Research ProjectMohit GoyalNo ratings yet

- The Effect of Return On Assets, Debt To Equity Ratio and Current Ratio On Earning Per Share (Study On LQ45 Index Banking Group Companies Listed On The Indonesia Stock Exchange 2015-2019)Document8 pagesThe Effect of Return On Assets, Debt To Equity Ratio and Current Ratio On Earning Per Share (Study On LQ45 Index Banking Group Companies Listed On The Indonesia Stock Exchange 2015-2019)ajmrdNo ratings yet

- A Usa Grenee Sfa 2004Document33 pagesA Usa Grenee Sfa 2004ridwanbudiman2000No ratings yet

- 391-Article Text-2781-1-10-20220620Document19 pages391-Article Text-2781-1-10-20220620bagas samuelNo ratings yet

- Firm Size 1Document9 pagesFirm Size 1afyqqhakimi205No ratings yet

- The Impact of Financial RatioDocument36 pagesThe Impact of Financial Ratio21-A-3-18 Desak Ayu Istri Shruti SarmaNo ratings yet

- Determinants of Dividend Policy in Saudi Listed CompaniesDocument10 pagesDeterminants of Dividend Policy in Saudi Listed CompaniesChickenrock TangerangNo ratings yet

- Financial Management - Assignment 1Document5 pagesFinancial Management - Assignment 1Manish Kumar GuptaNo ratings yet

- Financial Analysis Dissertation PDFDocument8 pagesFinancial Analysis Dissertation PDFProfessionalCollegePaperWritersUK100% (1)

- Impact of Financial Leverage On Cement Sector IndustryDocument16 pagesImpact of Financial Leverage On Cement Sector Industryinam100% (1)

- Audit Committee, Firm Size, Profitability, Leverage On Income SmoothingDocument14 pagesAudit Committee, Firm Size, Profitability, Leverage On Income SmoothingHisar PangaribuanNo ratings yet

- Effect of Working Capital Management On Firm ProfitabilityDocument15 pagesEffect of Working Capital Management On Firm ProfitabilityBagus Alaudin AhnafNo ratings yet

- Factors That Determine Dividend Payout. Evidence From The Financial Service Sector in South AfricaDocument9 pagesFactors That Determine Dividend Payout. Evidence From The Financial Service Sector in South AfricaNanditaNo ratings yet

- The Impact of Liquidity On Firm PerformanceDocument4 pagesThe Impact of Liquidity On Firm PerformancejdkjkfjkaNo ratings yet

- A Research ProposalDocument5 pagesA Research Proposalshahzad akNo ratings yet

- Auto Industry Research For FCGC 2011Document18 pagesAuto Industry Research For FCGC 2011bhundofcbmNo ratings yet

- Analysis of Effect Profitability, Liquidity and Solvability To Firm ValueDocument6 pagesAnalysis of Effect Profitability, Liquidity and Solvability To Firm ValuehichamlamNo ratings yet

- The Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDocument34 pagesThe Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDevikaNo ratings yet

- Effects of Cost Management On The Financial Performance of Profit Making Organizations in NigeriaDocument26 pagesEffects of Cost Management On The Financial Performance of Profit Making Organizations in NigeriaOgechukwu JulianaNo ratings yet

- Umer & Usman 2018Document9 pagesUmer & Usman 2018Babar NawazNo ratings yet

- Working Capital ManagementDocument8 pagesWorking Capital ManagementHarish.PNo ratings yet

- Jurnal ProfitabilitasDocument15 pagesJurnal ProfitabilitasDiah UtianiNo ratings yet

- Effect of Profitability of Corporate Values Through Dividend PolicyDocument9 pagesEffect of Profitability of Corporate Values Through Dividend Policysafa haddadNo ratings yet

- Jurnal Pendukung 5Document17 pagesJurnal Pendukung 5ARIF MUDJIONONo ratings yet

- Artikel Ardyas Yoga Yudhana NewDocument14 pagesArtikel Ardyas Yoga Yudhana Newyoteng87No ratings yet

- Profitability, Growth Opportunity, Capital Structure and The Firm ValueDocument22 pagesProfitability, Growth Opportunity, Capital Structure and The Firm ValueYohanes Danang PramonoNo ratings yet

- Fund Management and Profitability With Reference To APMDCDocument5 pagesFund Management and Profitability With Reference To APMDCthesijNo ratings yet

- Journal of Economics & BusinessDocument9 pagesJournal of Economics & Businessnoel_manroeNo ratings yet

- Impact of Leverage Ratio On ProfitabilityDocument9 pagesImpact of Leverage Ratio On ProfitabilitySaadia SaeedNo ratings yet

- The Effect of Economic Value Added FreeDocument15 pagesThe Effect of Economic Value Added FreeSumant AlagawadiNo ratings yet

- SSRN Id2603248Document7 pagesSSRN Id2603248vera maulithaNo ratings yet

- A Study On The Relationship Between Cash-Flow and Financial Performance of Insurance Companies: Evidence From A Developing EconomyDocument10 pagesA Study On The Relationship Between Cash-Flow and Financial Performance of Insurance Companies: Evidence From A Developing EconomymikeokayNo ratings yet

- The Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsDocument15 pagesThe Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsLouise Barik- بريطانية مغربيةNo ratings yet

- 1.yulius - Kurnia - Susanto With Cover Page v2Document8 pages1.yulius - Kurnia - Susanto With Cover Page v2dudung masterNo ratings yet

- Term Paper Insurance CompanyDocument24 pagesTerm Paper Insurance CompanyartusharNo ratings yet

- Profitability, Liquidity, Leverage, and Earnings Growth Hesty Juni Tambuati Subing, Citra Mariana, Rini SusianiDocument5 pagesProfitability, Liquidity, Leverage, and Earnings Growth Hesty Juni Tambuati Subing, Citra Mariana, Rini SusianiFani YanuarNo ratings yet

- Corporate Finance: Ambedkar University DelhiDocument44 pagesCorporate Finance: Ambedkar University DelhiRoshni RajanNo ratings yet

- Hero Moto Corp Financial AnalysisDocument16 pagesHero Moto Corp Financial AnalysisUmeshchandu4a9No ratings yet

- FCF, 23 163Document9 pagesFCF, 23 163Azizur Rahman RejviNo ratings yet

- Me Jona ImamDocument10 pagesMe Jona ImamFatima TahirNo ratings yet

- Ijebmr 847Document16 pagesIjebmr 847Amal MobarakiNo ratings yet

- The Role of Profitability and Leverage in Determining Indonesia's Companies Stock PricesDocument10 pagesThe Role of Profitability and Leverage in Determining Indonesia's Companies Stock Pricesindex PubNo ratings yet

- Sector Wise Effect of Solvency On Profitability Evidence From Jordanian ContextDocument8 pagesSector Wise Effect of Solvency On Profitability Evidence From Jordanian Contextwilliam chandraNo ratings yet

- Mutawali Id enDocument12 pagesMutawali Id enMUC kediriNo ratings yet

- 6070 12504 1 SMDocument17 pages6070 12504 1 SMRizkiNo ratings yet

- Analysis of The Factors Affecting Devident PolicyDocument12 pagesAnalysis of The Factors Affecting Devident PolicyJung AuLiaNo ratings yet

- The Effect of Debt Equity Ratio, Dividend Payout Ratio, and Profitability On The Firm ValueDocument6 pagesThe Effect of Debt Equity Ratio, Dividend Payout Ratio, and Profitability On The Firm ValueThe IjbmtNo ratings yet

- Roa CR Der THP Hs Inter DividenDocument15 pagesRoa CR Der THP Hs Inter Dividenumar YPUNo ratings yet

- Performance Evaluation PDFDocument10 pagesPerformance Evaluation PDFsiddhartha karNo ratings yet

- The Impact of Firm Growth On Stock Returns of Nonfinancial Firms Listed On Egyptian Stock ExchangeDocument17 pagesThe Impact of Firm Growth On Stock Returns of Nonfinancial Firms Listed On Egyptian Stock Exchangealma kalyaNo ratings yet

- 1.1 Industry ProfileDocument9 pages1.1 Industry ProfilemgajenNo ratings yet

- Findings: Age Wise ClassificationDocument3 pagesFindings: Age Wise ClassificationmgajenNo ratings yet

- Table 17: Factors Wise Classification From Respondents: (AverageDocument4 pagesTable 17: Factors Wise Classification From Respondents: (AveragemgajenNo ratings yet

- Summary, Findings and ConclusionDocument10 pagesSummary, Findings and ConclusionmgajenNo ratings yet

- 1.3 Company ProfileDocument10 pages1.3 Company ProfilemgajenNo ratings yet

- Findings of Leverages and Cost SheetDocument3 pagesFindings of Leverages and Cost SheetmgajenNo ratings yet

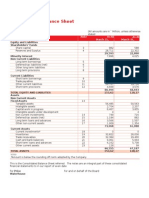

- Consolidated Balance Sheet: Annual Report 2013 - 2014Document2 pagesConsolidated Balance Sheet: Annual Report 2013 - 2014mgajenNo ratings yet

- Inventory To Current Asset RatioDocument6 pagesInventory To Current Asset RatiomgajenNo ratings yet

- Ratio Formula RemarksDocument7 pagesRatio Formula RemarksmgajenNo ratings yet

- Credit Appraisal IntroductionDocument17 pagesCredit Appraisal IntroductionmgajenNo ratings yet

- Objectives of The Study Primary ObjectiveDocument1 pageObjectives of The Study Primary ObjectivemgajenNo ratings yet

- Credit Appraisal & NPA Management: Arkadip Gupta PGDMB14-101Document34 pagesCredit Appraisal & NPA Management: Arkadip Gupta PGDMB14-101mgajenNo ratings yet

- Project On IobDocument63 pagesProject On IobSadha Nanda PrabhuNo ratings yet

- Mr.S.VIGNESH (REG NO:711300247) Student From Your College (Chennai) Private Limited From 28Document1 pageMr.S.VIGNESH (REG NO:711300247) Student From Your College (Chennai) Private Limited From 28mgajenNo ratings yet

- IOB Annual Report 2011Document184 pagesIOB Annual Report 2011mgajenNo ratings yet

- (Highest Safety) : Crisil AaaDocument1 page(Highest Safety) : Crisil AaamgajenNo ratings yet

- A Study On Grievance Handling Procedure at Hema Engineering Industries Limited, HosurDocument9 pagesA Study On Grievance Handling Procedure at Hema Engineering Industries Limited, Hosurmgajen100% (1)

- Inti Agri Resources TBK.: Company Report: January 2019 As of 31 January 2019Document3 pagesInti Agri Resources TBK.: Company Report: January 2019 As of 31 January 2019Yohanes ImmanuelNo ratings yet

- Cash and Accrual BasisDocument5 pagesCash and Accrual BasisLeisleiRago100% (1)

- Risk & ReturnDocument20 pagesRisk & Returnjhumli100% (1)

- Accounting For PartnershipsDocument58 pagesAccounting For PartnershipsAmy MurphyNo ratings yet

- FIN4020-CHAPTER 2-SAMPLE MCQsDocument2 pagesFIN4020-CHAPTER 2-SAMPLE MCQsSyahrul Aman IsmailNo ratings yet

- Uncertainty and Consumer Behavior: ©2005 Pearson Education, IncDocument53 pagesUncertainty and Consumer Behavior: ©2005 Pearson Education, IncMarinaNo ratings yet

- Beams Aa13e SM 01Document14 pagesBeams Aa13e SM 01jiajiaNo ratings yet

- Intrinsic Value - Digital BookDocument60 pagesIntrinsic Value - Digital Bookfuzzychan50% (2)

- Balance Sheet TemplateDocument4 pagesBalance Sheet TemplateSardar A A KhanNo ratings yet

- Bain and CompanyDocument10 pagesBain and CompanyRahul SinghNo ratings yet

- ZeeFreaks - Swing Trading vs. Trend FollowingDocument5 pagesZeeFreaks - Swing Trading vs. Trend FollowingcyrenetpaNo ratings yet

- Wakala ModelDocument24 pagesWakala ModelNurul Syuhada Ismail0% (1)

- Sec-F Grp-3 CF-II Project - Tata SteelDocument20 pagesSec-F Grp-3 CF-II Project - Tata SteelPranav BajajNo ratings yet

- CURRENT PRICING OF IPOs: Is It Investor-Friendly?Document53 pagesCURRENT PRICING OF IPOs: Is It Investor-Friendly?Sayam RoyNo ratings yet

- Quarterly Report Q3 2010 MJNADocument20 pagesQuarterly Report Q3 2010 MJNAcb0bNo ratings yet

- Accounts Code SS 30Document32 pagesAccounts Code SS 30VidhiNo ratings yet

- Baron Coburg - Analisis y SolucionDocument7 pagesBaron Coburg - Analisis y SolucionHancel CentenoNo ratings yet

- FAR Test BankDocument24 pagesFAR Test BankMaryjel17No ratings yet

- D-Intervenors Motion For Complete Summary Judgement With ExhibitsDocument74 pagesD-Intervenors Motion For Complete Summary Judgement With Exhibitsapi-467534276No ratings yet

- AC330 Class2 CascinoDocument18 pagesAC330 Class2 Cascino2c_adminNo ratings yet

- Suncorp Group Investor Day Presentation ASX - FinalDocument28 pagesSuncorp Group Investor Day Presentation ASX - FinaldigifiNo ratings yet

- Group 4 Assignment Campus Deli 1Document9 pagesGroup 4 Assignment Campus Deli 1namitasharma1512100% (4)

- Cost of Capital (AnkushaDocument42 pagesCost of Capital (AnkushaPiyush ChauhanNo ratings yet

- Difference Between Member and Shareholder of A Company For A CompanyDocument2 pagesDifference Between Member and Shareholder of A Company For A CompanyMragank ShuklaNo ratings yet

- Ratio: Gas Authority of India Limited (Gail)Document9 pagesRatio: Gas Authority of India Limited (Gail)hari_mohan_7No ratings yet

- A Dozen Things Ive Learned About Great CEOs From The Outsiders Written by William ThorndikeDocument6 pagesA Dozen Things Ive Learned About Great CEOs From The Outsiders Written by William ThorndikepiyushNo ratings yet

- 2011-12-13 Rothstein Scott AMDocument129 pages2011-12-13 Rothstein Scott AMmatthendleyNo ratings yet

- Investment Avenues (Securities) in PakistanDocument7 pagesInvestment Avenues (Securities) in PakistanPolite Charm100% (1)

- Wonderful Malaysia Berhad - Illustrative Financial Statements 2014Document243 pagesWonderful Malaysia Berhad - Illustrative Financial Statements 2014Selva Bavani SelwaduraiNo ratings yet