You might also like

- Mba201 PDFDocument71 pagesMba201 PDFnikhil100% (1)

- Approaches To Business EthicsDocument54 pagesApproaches To Business Ethicsraj015No ratings yet

- Business EthicsDocument64 pagesBusiness EthicsPravin Nishar100% (1)

- 01-The Curious Case of Filipino Micro-Entrepreneurs' Financial Sophistication and The Triple Bottom LineDocument10 pages01-The Curious Case of Filipino Micro-Entrepreneurs' Financial Sophistication and The Triple Bottom LineSharifi shahramNo ratings yet

- Ethics in HRDocument6 pagesEthics in HRMuskaan AgarwalNo ratings yet

- What Is Social Responsibility?Document8 pagesWhat Is Social Responsibility?Charo GironellaNo ratings yet

- Fundamentals of Business CommunicationDocument18 pagesFundamentals of Business CommunicationSandeep Shankar50% (2)

- LECTURE - 4 CHAPTER 4 Managing in A Global EnvironmentDocument33 pagesLECTURE - 4 CHAPTER 4 Managing in A Global EnvironmentAngelica100% (1)

- Ethics in Human Resources: Presented By:Swatinigam Jagraninstitute of ManagementDocument17 pagesEthics in Human Resources: Presented By:Swatinigam Jagraninstitute of ManagementMateo CarinoNo ratings yet

- Business Communication BOOK VU ComsatsDocument21 pagesBusiness Communication BOOK VU ComsatsTauseef AhmadNo ratings yet

- A Biography On Kishore BiyaniDocument39 pagesA Biography On Kishore Biyanipriya3131991100% (2)

- 10.topic 8 - Employee CompensationDocument28 pages10.topic 8 - Employee CompensationA Ahmad NazreenNo ratings yet

- Financial Management Megginson Smart GrahamDocument15 pagesFinancial Management Megginson Smart GrahamJason De Gracia BelandoNo ratings yet

- 9.topic 7 - Performance EvaluationDocument27 pages9.topic 7 - Performance EvaluationA Ahmad NazreenNo ratings yet

- Business Ethics ESB5011 Final Exam PDFDocument20 pagesBusiness Ethics ESB5011 Final Exam PDFEmmacue tNo ratings yet

- HR Planning and Recruitment ProcessDocument34 pagesHR Planning and Recruitment ProcessItchigo KorusakiNo ratings yet

- Business EthicsDocument144 pagesBusiness EthicsNeha KalraNo ratings yet

- Chapter 6 - Individual Factors: Moral Philosophies & ValuesDocument24 pagesChapter 6 - Individual Factors: Moral Philosophies & ValuesMariam KhailanyNo ratings yet

- Latif - Sample 1Document20 pagesLatif - Sample 1SarojNo ratings yet

- Chapter 10..writing Routine and Positive MessageDocument27 pagesChapter 10..writing Routine and Positive MessageAfsar Ahmed100% (1)

- Southwest Airlines Leadership Case StudyDocument2 pagesSouthwest Airlines Leadership Case StudyRohit KhanNo ratings yet

- Business Ethics Assig A4Document3 pagesBusiness Ethics Assig A4Rahima SyedNo ratings yet

- CH1 Bus EthDocument18 pagesCH1 Bus EthSushmita SarkarNo ratings yet

- HEC Undegraduate Policy 2023 Curriculum FinalDocument89 pagesHEC Undegraduate Policy 2023 Curriculum Finalhhhh.shehzadNo ratings yet

- Value, Ethics and Working Collaboratively (Corrected)Document12 pagesValue, Ethics and Working Collaboratively (Corrected)Ramisa TasfiahNo ratings yet

- Sample HR Interview QuestionsDocument74 pagesSample HR Interview Questionssumitvfx87No ratings yet

- Aroob Zia-MMS151055Document63 pagesAroob Zia-MMS151055AZAHR ALINo ratings yet

- HR Journal 2Document22 pagesHR Journal 2JMANo ratings yet

- Intro to Business EthicsDocument29 pagesIntro to Business EthicsMayank Yadav100% (1)

- Code of Ethics Importance and Encouraging Workplace Ethical BehaviorDocument8 pagesCode of Ethics Importance and Encouraging Workplace Ethical BehaviorfatyNo ratings yet

- Assignment 6 Resource ManagementDocument42 pagesAssignment 6 Resource Managementsakhar babuNo ratings yet

- Three Major Approaches To Business EthicsDocument6 pagesThree Major Approaches To Business Ethicsxndrxx100% (1)

- University of Lahore Business Communication Course OutlineDocument3 pagesUniversity of Lahore Business Communication Course OutlineHassanRaza100% (1)

- 7.reading Skills For Effective Business CommunicationDocument16 pages7.reading Skills For Effective Business CommunicationDevanshu GehlotNo ratings yet

- Ethics and Communication PDFDocument2 pagesEthics and Communication PDFRonnieNo ratings yet

- Albrecht, S. L., Bakker, A. B., Gruman, J. A., Macey, W. H., Saks, A. M. (2015)Document31 pagesAlbrecht, S. L., Bakker, A. B., Gruman, J. A., Macey, W. H., Saks, A. M. (2015)FRANCISCA JAVIERA VILLALOBOS POVEDANo ratings yet

- WEEK 1 (Defining Leadership)Document4 pagesWEEK 1 (Defining Leadership)Joshua OrimiyeyeNo ratings yet

- Lesson Plan Financial Derivatives MbaiiiDocument5 pagesLesson Plan Financial Derivatives MbaiiiSheg AonNo ratings yet

- Course Identification: Mid Term Exam 15% Result in Points Result in %Document9 pagesCourse Identification: Mid Term Exam 15% Result in Points Result in %Gurlal SinghNo ratings yet

- Syllabus Bcom 3 SemDocument24 pagesSyllabus Bcom 3 Semmahesh50500% (1)

- Talon-Talon National High School: Department of EducationDocument15 pagesTalon-Talon National High School: Department of Educationjayvee grace tuballaNo ratings yet

- Business Communication Lesson 1Document4 pagesBusiness Communication Lesson 1Kryzelle Angela OnianaNo ratings yet

- Academic WritingDocument27 pagesAcademic WritingShinie100% (3)

- Ethics in Business CommunicationDocument2 pagesEthics in Business CommunicationppoojashreeNo ratings yet

- Understanding Ethics and Morality in BusinessDocument5 pagesUnderstanding Ethics and Morality in BusinessSagarNo ratings yet

- Business Research MethodsDocument62 pagesBusiness Research MethodsSourav KaranthNo ratings yet

- Chapter 17 Managers As LeadersDocument20 pagesChapter 17 Managers As Leaderstanvir ehsanNo ratings yet

- Business Ethics Project ReportDocument16 pagesBusiness Ethics Project ReportAnanay ChopraNo ratings yet

- Evaluation of Management Thought PDFDocument2 pagesEvaluation of Management Thought PDFErica50% (2)

- How The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.Document15 pagesHow The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.IOSRjournalNo ratings yet

- Behaviour & Leadership T GreenDocument16 pagesBehaviour & Leadership T GreenJürgen StraussNo ratings yet

- Doing Business in India A Cultural & Ethical PerspectiveDocument7 pagesDoing Business in India A Cultural & Ethical PerspectiveSumit SrivastawaNo ratings yet

- Ethics Business Research PDFDocument2 pagesEthics Business Research PDFDestinyNo ratings yet

- Mingers - What Is It To Be CriticalDocument19 pagesMingers - What Is It To Be CriticalSushanta_sarmaNo ratings yet

- Talent Management Information SystemDocument7 pagesTalent Management Information SystemAnkita BhardwajNo ratings yet

- International Strategic Management A Complete Guide - 2020 EditionFrom EverandInternational Strategic Management A Complete Guide - 2020 EditionNo ratings yet

- Ipi144576 PDFDocument18 pagesIpi144576 PDFakituchNo ratings yet

- Preparing Students For Their Future Accounting Careers PDFDocument15 pagesPreparing Students For Their Future Accounting Careers PDFakituchNo ratings yet

- Strategic Management Corporate Performance, Governance & Business Ethics PDFDocument24 pagesStrategic Management Corporate Performance, Governance & Business Ethics PDFakituchNo ratings yet

- Romney Ch01Document85 pagesRomney Ch01bajigur47No ratings yet

- Conformance and PerformanceDocument2 pagesConformance and PerformancetekabiNo ratings yet

- R04 Introduction To GIPS IFT NotesDocument4 pagesR04 Introduction To GIPS IFT NotesSumaira ShahidNo ratings yet

- Fazlani CVDocument3 pagesFazlani CVmba2135156No ratings yet

- General ReportDocument30 pagesGeneral ReportRaman LakhanpalNo ratings yet

- LOG311-Nguyễn Thanh Tùng - HS153103Document9 pagesLOG311-Nguyễn Thanh Tùng - HS153103Nguyen Thanh Tung (K15 HL)No ratings yet

- Spotify An ITIL Case StudyDocument13 pagesSpotify An ITIL Case StudyAvneeshÜbermenschBalyanNo ratings yet

- PentanaBrochure2017 V2 WebDocument3 pagesPentanaBrochure2017 V2 WebamasiddayNo ratings yet

- Chapter 26Document22 pagesChapter 26Elie Bou GhariosNo ratings yet

- ISO 14001 2015 Checklist6Document8 pagesISO 14001 2015 Checklist6Belajar K3LNo ratings yet

- OECD Working Paper Discusses Social Media Use by GovernmentsDocument72 pagesOECD Working Paper Discusses Social Media Use by GovernmentsAnibal MartinNo ratings yet

- 2010 Hays Salary Guide in AsiaDocument60 pages2010 Hays Salary Guide in AsiaJarvisNo ratings yet

- Buy American Webinar 20100906Document25 pagesBuy American Webinar 20100906Daniel GiblettNo ratings yet

- PWC Vietnam Technology enDocument16 pagesPWC Vietnam Technology engogana93100% (1)

- Indonesia Salary Guide 2011 12Document28 pagesIndonesia Salary Guide 2011 12Ridayani DamanikNo ratings yet

- Emerging Issues in Company Law PDFDocument31 pagesEmerging Issues in Company Law PDFabhimanyukumar0% (1)

- 2013 JCOPE Annual ReportDocument316 pages2013 JCOPE Annual ReportNick ReismanNo ratings yet

- Cobit For Internal Auditors: Lucas Kowal, Avp BNP Paribas NaDocument31 pagesCobit For Internal Auditors: Lucas Kowal, Avp BNP Paribas Naavnish_irmNo ratings yet

- InsiderDocument33 pagesInsidervikhyat2010No ratings yet

- Sap GRC Interview QuestionsDocument20 pagesSap GRC Interview QuestionsBiswa Ranjan Nayak100% (3)

- Construction Roles and ResponsibilitiesDocument4 pagesConstruction Roles and ResponsibilitiesDarl Anthony VelosoNo ratings yet

- Noise ManagementDocument24 pagesNoise ManagementKhushi ShaikhNo ratings yet

- Screenshot 2023-07-24 at 11.58.21Document47 pagesScreenshot 2023-07-24 at 11.58.21Verina NahabweNo ratings yet

- Weathering the StormDocument180 pagesWeathering the StormscribdNo ratings yet

- Dissertation On Public Procurement ReformsDocument127 pagesDissertation On Public Procurement Reformsross.hartleysaNo ratings yet

- Social Security Law No.1 For The Year 2014 and Its AmendmentsDocument116 pagesSocial Security Law No.1 For The Year 2014 and Its AmendmentsgemrafiNo ratings yet

- NEPRA Drafts New HSE Code for Power Sector LicenseesDocument68 pagesNEPRA Drafts New HSE Code for Power Sector LicenseesSyed Fawad ShahNo ratings yet

- TIL 1707 - Outer Crossfire Tube Packing Ring UpgradeDocument6 pagesTIL 1707 - Outer Crossfire Tube Packing Ring UpgradeBouazzaNo ratings yet

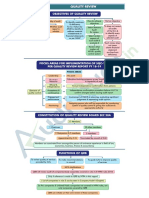

- Objectives of Quality ReviewDocument6 pagesObjectives of Quality ReviewVijay Kumar KollaNo ratings yet

- FMVSS 106 Brake Hose Test ProceduresDocument180 pagesFMVSS 106 Brake Hose Test ProceduresgerrecartNo ratings yet

- FSANZ Safe Food Australia - WEBDocument225 pagesFSANZ Safe Food Australia - WEBNyanne MianoNo ratings yet