You might also like

- Nmims Icef 2019Document12 pagesNmims Icef 2019Rituparna DasNo ratings yet

- Letter From IBC CambridgeDocument1 pageLetter From IBC CambridgeRituparna DasNo ratings yet

- Liquidation of Cooperative Banks in India: Implications of Performance Indicators For LiquidationDocument22 pagesLiquidation of Cooperative Banks in India: Implications of Performance Indicators For LiquidationRituparna DasNo ratings yet

- Forecasting Paper BOUNDDocument7 pagesForecasting Paper BOUNDRituparna DasNo ratings yet

- Among Top 1% of 200 MillionDocument1 pageAmong Top 1% of 200 MillionRituparna DasNo ratings yet

- Sample Test Paper On Bank ManagementDocument1 pageSample Test Paper On Bank ManagementRituparna DasNo ratings yet

- Rituparna Das: Supply in India), M.Sc. (Economics), B.Sc. (Economics Honours), NET, SLET & State Research ScholarshipDocument12 pagesRituparna Das: Supply in India), M.Sc. (Economics), B.Sc. (Economics Honours), NET, SLET & State Research ScholarshipRituparna DasNo ratings yet

- Instructions: All Questions Are Compulsory and Carry Equal MarksDocument1 pageInstructions: All Questions Are Compulsory and Carry Equal MarksRituparna DasNo ratings yet

- Financial Risk and Economics Educator and Author - GlobalDocument1 pageFinancial Risk and Economics Educator and Author - GlobalRituparna DasNo ratings yet

- Full Page PhotoDocument1 pageFull Page PhotoRituparna DasNo ratings yet

- My Contribution in Interdisciplinary TeachingDocument3 pagesMy Contribution in Interdisciplinary TeachingRituparna DasNo ratings yet

- Full Page Photo3Document1 pageFull Page Photo3Rituparna DasNo ratings yet

- NigeriaDocument2 pagesNigeriaRituparna DasNo ratings yet

- Full Page Photo2Document1 pageFull Page Photo2Rituparna DasNo ratings yet

- Risk Management and Derivatives MBA (Finance) Full Marks 10 Time 1 PeriodDocument1 pageRisk Management and Derivatives MBA (Finance) Full Marks 10 Time 1 PeriodRituparna DasNo ratings yet

- Programme On Fixed Income in ExcelDocument2 pagesProgramme On Fixed Income in ExcelRituparna DasNo ratings yet

- Financial Management FinalDocument1 pageFinancial Management FinalRituparna DasNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sewage Treatment PlantDocument16 pagesSewage Treatment PlantSrinivasa NadgoudaNo ratings yet

- Design of Sand FilterDocument5 pagesDesign of Sand FilterAbhay ThakurNo ratings yet

- Honors Chemistry Semester 1 ProjectDocument7 pagesHonors Chemistry Semester 1 Projectapi-239401136No ratings yet

- 503-Article Text-1428-1-10-20211210 - 2Document10 pages503-Article Text-1428-1-10-20211210 - 2yamar2000No ratings yet

- Industrial Effluent's Health Impact on Noyyal River Basin VillagersDocument8 pagesIndustrial Effluent's Health Impact on Noyyal River Basin VillagersTimothy BrownNo ratings yet

- Water Pollution Sources, Effects, Control and ManagementDocument4 pagesWater Pollution Sources, Effects, Control and Managementetik ainun rohmahNo ratings yet

- Introduction to BioSand FiltersDocument19 pagesIntroduction to BioSand FiltersMyk Twentytwenty NBeyondNo ratings yet

- Introduction To Environmental Studies (Nes 101) - 1Document141 pagesIntroduction To Environmental Studies (Nes 101) - 1Bildad JoashNo ratings yet

- Flow Chart Sewage TreatmentDocument2 pagesFlow Chart Sewage TreatmentapriNo ratings yet

- Ecology MCQ بيئة وتلوثDocument19 pagesEcology MCQ بيئة وتلوثAli AliNo ratings yet

- Industrial Pollution ControlDocument37 pagesIndustrial Pollution ControlAlperNo ratings yet

- Case Study of Bhandup Water Treatment Plant: - Project Guide: Satishchandra OzarkarDocument27 pagesCase Study of Bhandup Water Treatment Plant: - Project Guide: Satishchandra OzarkarMAYURESH PATIL100% (1)

- Grease Trap DesignDocument2 pagesGrease Trap DesigndcsamaraweeraNo ratings yet

- 3 Lecture Wastewater Characteristic AnalysisDocument41 pages3 Lecture Wastewater Characteristic AnalysiszeyadNo ratings yet

- Let Us Build A Healthy SocietyDocument13 pagesLet Us Build A Healthy SocietySalman FarisNo ratings yet

- Water Quality Status of Main TempleDocument6 pagesWater Quality Status of Main TempleInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Biology Portfolio Water For AllDocument13 pagesBiology Portfolio Water For AllAaron Mathew JohnNo ratings yet

- Proposal For Kubota HCZ-50 Wastewater Treatment Plant For Cargills Bandarawela PDFDocument25 pagesProposal For Kubota HCZ-50 Wastewater Treatment Plant For Cargills Bandarawela PDFshehanNo ratings yet

- Struktur Organisasi Personil OC-2 KOTAKU SumutDocument1 pageStruktur Organisasi Personil OC-2 KOTAKU SumuttomcivilianNo ratings yet

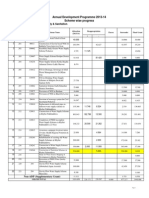

- Sector: Drinking Water Supply & Sanitation: Annual Development Programme 2013-14 Scheme Wise ProgressDocument1 pageSector: Drinking Water Supply & Sanitation: Annual Development Programme 2013-14 Scheme Wise ProgressFazal Ahmad MarwatNo ratings yet

- INAE Project Report PDFDocument211 pagesINAE Project Report PDFAkhilesh GuptaNo ratings yet

- Water Consumption Calculation: Vietcombank VietnamDocument10 pagesWater Consumption Calculation: Vietcombank VietnamsamehNo ratings yet

- Plumbing Design Service ProposalDocument2 pagesPlumbing Design Service ProposalChristan Daniel RestorNo ratings yet

- Remote Sensing for Water Quality and ResourcesDocument8 pagesRemote Sensing for Water Quality and ResourcesAlejandro Rodriguez100% (1)

- Ssemmambo Mathias Project Final Report-1Document87 pagesSsemmambo Mathias Project Final Report-1macklyn tyanNo ratings yet

- Waste Water TeatmentDocument18 pagesWaste Water TeatmentLazaro100% (1)

- Pollution PDFDocument14 pagesPollution PDFRavi Chandran R CNo ratings yet

- SSR Mvjce NaacDocument133 pagesSSR Mvjce NaacPrathap VuyyuruNo ratings yet

- Optimize Jar Test Parameters for Water TreatmentDocument9 pagesOptimize Jar Test Parameters for Water Treatmentمحمد أمير لقمانNo ratings yet

- Pollution ControlDocument62 pagesPollution ControlshubhamNo ratings yet