You might also like

- Exp 2 (WL)Document8 pagesExp 2 (WL)Aswathy M NNo ratings yet

- Exp 2 (WL)Document8 pagesExp 2 (WL)Aswathy M NNo ratings yet

- Experiment No: 1 Earthquake Analysis Date:: Structural Engineering Lab-IiDocument7 pagesExperiment No: 1 Earthquake Analysis Date:: Structural Engineering Lab-IiAswathy M NNo ratings yet

- V-VIII Sem Scheme Civil Final 18-6-2017Document4 pagesV-VIII Sem Scheme Civil Final 18-6-2017SudeepSMenasinakaiNo ratings yet

- Ev 1Document9 pagesEv 1Aswathy M NNo ratings yet

- Syllabus SJVN LTD Executive Trainees Civil Engg1Document3 pagesSyllabus SJVN LTD Executive Trainees Civil Engg1Aswathy M NNo ratings yet

- 1893-Part 1-2016-1 PDFDocument44 pages1893-Part 1-2016-1 PDFDarshit Vejani100% (3)

- M.Tech-Construction Techonology: SyllabusDocument45 pagesM.Tech-Construction Techonology: SyllabusAswathy M NNo ratings yet

- CH 1Document30 pagesCH 1Prashant SharmaNo ratings yet

- Mtech SyllabusDocument44 pagesMtech SyllabusLal ChhuanmawiaNo ratings yet

- Lecture11 PDFDocument16 pagesLecture11 PDFAswathy M NNo ratings yet

- Spicy Chicken Curry: Semiya Paayasam Aka Seviyan Kheer (Vermicelli Pudding) Eggless Chocolate CroissantsDocument2 pagesSpicy Chicken Curry: Semiya Paayasam Aka Seviyan Kheer (Vermicelli Pudding) Eggless Chocolate CroissantsAswathy M NNo ratings yet

- Micro STRDocument182 pagesMicro STRAswathy M NNo ratings yet

- Scanning Electron MicroscopeDocument15 pagesScanning Electron MicroscopeFathan Hanifi Mada MahendraNo ratings yet

- Recipie N ShortDocument1 pageRecipie N ShortAswathy M NNo ratings yet

- SCC Elevated Temp...Document10 pagesSCC Elevated Temp...Aswathy M NNo ratings yet

- Curing Read OnlyDocument9 pagesCuring Read OnlyM Mirza Abdillah PratamaNo ratings yet

- Micro Freeze ThawDocument7 pagesMicro Freeze ThawAswathy M NNo ratings yet

- Ev - SemDocument9 pagesEv - SemAswathy M NNo ratings yet

- Waste FibersDocument6 pagesWaste FibersAswathy M NNo ratings yet

- Delayed Ettringite Formation (DEF)Document25 pagesDelayed Ettringite Formation (DEF)tcthomasNo ratings yet

- Lime - MetakaolineDocument4 pagesLime - MetakaolineAswathy M NNo ratings yet

- Micro SEMDocument8 pagesMicro SEMAswathy M NNo ratings yet

- PP Fibres in ConcreteDocument120 pagesPP Fibres in ConcreteAswathy M NNo ratings yet

- Lime - MetakaolineDocument4 pagesLime - MetakaolineAswathy M NNo ratings yet

- CCE Proficience ChecklistDocument2 pagesCCE Proficience ChecklistPraveenpal Kumar PalNo ratings yet

- Curing Read OnlyDocument9 pagesCuring Read OnlyM Mirza Abdillah PratamaNo ratings yet

- Instruction For Submitting ApplicationDocument1 pageInstruction For Submitting ApplicationAswathy M NNo ratings yet

- Jan-May 2016 Poster 3Document1 pageJan-May 2016 Poster 3Aswathy M NNo ratings yet

- ScheduleDocument1 pageScheduleAswathy M NNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Exercises Chapter 8 Time Value of MoneyDocument2 pagesExercises Chapter 8 Time Value of MoneyThet Thet MarNo ratings yet

- FABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsDocument14 pagesFABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsSophia MagdaraogNo ratings yet

- Acct Project Question 2Document14 pagesAcct Project Question 2grace100% (1)

- ISLAMIC BANKING IN PAKISTAN: MEEZAN BANK'S CASE STUDYDocument6 pagesISLAMIC BANKING IN PAKISTAN: MEEZAN BANK'S CASE STUDYfaisal_ahsan7919No ratings yet

- Tax Invoice No. 540: DescriptionDocument1 pageTax Invoice No. 540: DescriptionMariam BaldeNo ratings yet

- Requirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableDocument338 pagesRequirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableRigine MorgadezNo ratings yet

- Conclusions and Suggestions.: Chapter No. 07Document35 pagesConclusions and Suggestions.: Chapter No. 07SarinNo ratings yet

- PDFDocument2 pagesPDFash saNo ratings yet

- Overview of Marine Insurance Law Prof. Dr. Marko PavlihaDocument51 pagesOverview of Marine Insurance Law Prof. Dr. Marko PavlihasimranNo ratings yet

- Carlo Corp acquisition of John Co assetsDocument7 pagesCarlo Corp acquisition of John Co assetsAlarich CatayocNo ratings yet

- Kunci JawabanDocument31 pagesKunci JawabanDeni HudayaNo ratings yet

- AVF HDFC Bank FormDocument2 pagesAVF HDFC Bank Formakash agarwalNo ratings yet

- PSBA Refresher Course Hyperinflation Accounting QuestionsDocument2 pagesPSBA Refresher Course Hyperinflation Accounting QuestionsAna Marie IllutNo ratings yet

- Acc Exam 1Document21 pagesAcc Exam 1binalamitNo ratings yet

- MCOM Advanced Financial AccountingDocument2 pagesMCOM Advanced Financial AccountingKishan Kudia0% (3)

- Capm and AptDocument2 pagesCapm and AptNeelam MadarapuNo ratings yet

- The Following Is The Unadjusted Trial Balance For Rocky MountainDocument2 pagesThe Following Is The Unadjusted Trial Balance For Rocky MountainMiroslav GegoskiNo ratings yet

- Survey ChecklistDocument4 pagesSurvey ChecklistAngela Miles DizonNo ratings yet

- Indonesia - ARTO - First Digibank Taking Off 080621Document26 pagesIndonesia - ARTO - First Digibank Taking Off 080621robNo ratings yet

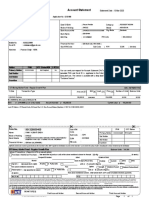

- Account Statement: Vinay Kumar SinghDocument1 pageAccount Statement: Vinay Kumar SinghUtkarsh SinghNo ratings yet

- Maven 1 Bedroom Sample ComputationDocument1 pageMaven 1 Bedroom Sample ComputationJonathan LeciasNo ratings yet

- Ic 86 Practice Test 4Document29 pagesIc 86 Practice Test 4Samba SivaNo ratings yet

- Top 500 Banking Brands Cover StoryDocument5 pagesTop 500 Banking Brands Cover StoryPhương Anh TrầnNo ratings yet

- Shriram Life Insurance Company (Wiki)Document2 pagesShriram Life Insurance Company (Wiki)KaranPatil50% (2)

- ABM5 NOTES (1st QUARTER)Document16 pagesABM5 NOTES (1st QUARTER)Adrianne Mae Almalvez Rodrigo100% (1)

- HDFC Insta Loan DetailsDocument3 pagesHDFC Insta Loan DetailsbalaNo ratings yet

- Financial Statement Analysis: Project Report ON "Motherson Sumi Systems LTD"Document17 pagesFinancial Statement Analysis: Project Report ON "Motherson Sumi Systems LTD"writik sahaNo ratings yet

- 8th MFI - Conference AgendaDocument8 pages8th MFI - Conference AgendaJesbechoNo ratings yet

- STA 2191 - AM I - Lecture 7 - Life Annuity ContractsDocument21 pagesSTA 2191 - AM I - Lecture 7 - Life Annuity ContractsCyprian OmariNo ratings yet

- Invoice 1904071602506wbmgorflj4qpn8Document1 pageInvoice 1904071602506wbmgorflj4qpn8Atiq R RafiNo ratings yet