You might also like

- Coal Supply in IndonesiaDocument25 pagesCoal Supply in IndonesiaSunapaNo ratings yet

- Coal Outlook 2019 - Webinar Alumni Tambang ITB - Sandro H S PDFDocument32 pagesCoal Outlook 2019 - Webinar Alumni Tambang ITB - Sandro H S PDFhipsterzNo ratings yet

- Coal Overview in IndonesiaDocument23 pagesCoal Overview in IndonesiaAbhishek TripathiNo ratings yet

- Summary Coal Industry in IndonesiaDocument9 pagesSummary Coal Industry in IndonesiadoddyibeNo ratings yet

- Analysis Coal FinalDocument21 pagesAnalysis Coal FinalAlok KumarNo ratings yet

- Port Development and PendulumDocument47 pagesPort Development and PendulumHerdy Pratama PutraNo ratings yet

- Coal MarketingDocument5 pagesCoal MarketingVenuNo ratings yet

- BHP vs. Rio TintoDocument54 pagesBHP vs. Rio Tintoeholmes80100% (2)

- Coal Supply Chain IcrDocument32 pagesCoal Supply Chain IcrKorchak JohnNo ratings yet

- Coal Sourcing Handling and Transportation Report - Volume - VDocument497 pagesCoal Sourcing Handling and Transportation Report - Volume - Vদেওয়ানসাহেবNo ratings yet

- Jagartha Obeservation: Nickel Mining Industry OverviewDocument32 pagesJagartha Obeservation: Nickel Mining Industry OverviewRatumasFeNo ratings yet

- Adaro Energy Annual Report 2011 EngDocument280 pagesAdaro Energy Annual Report 2011 EngAsti MarianaNo ratings yet

- Global CementDocument25 pagesGlobal Cementm.moszkowski9755No ratings yet

- Investment Opportunity of Mineral and Coal in IndonesiaDocument26 pagesInvestment Opportunity of Mineral and Coal in IndonesiaKrisdanyolan SimarmataNo ratings yet

- Cokal Investor PresentationDocument34 pagesCokal Investor PresentationdonnypsNo ratings yet

- INR - Ed-1 Feb 2020Document41 pagesINR - Ed-1 Feb 2020Dirga DanielNo ratings yet

- at Kearney-MakingIndonesiah4.0 NetExportAcceleration v2.5 ShortDocument9 pagesat Kearney-MakingIndonesiah4.0 NetExportAcceleration v2.5 Shortwirawanprasetyo100% (1)

- Maputo Development CorridorDocument18 pagesMaputo Development CorridorRaimundo Paulo Langa100% (1)

- McKinsey Perspective On Chinas Auto Market in 2020 PDFDocument16 pagesMcKinsey Perspective On Chinas Auto Market in 2020 PDFMiguel Castell100% (1)

- BP Matsuri Suites - FinalDocument229 pagesBP Matsuri Suites - FinalAldi WirawanNo ratings yet

- Kalimantan Coal Railway ProjectDocument23 pagesKalimantan Coal Railway ProjectmimandapiconeNo ratings yet

- Mining and ResourcesDocument32 pagesMining and ResourcesNicolas Tapia100% (2)

- CA Indonesia 2013Document44 pagesCA Indonesia 2013DonnyNo ratings yet

- MRO On The Move: Outsourcing Maintenance, Repair and OperationsDocument12 pagesMRO On The Move: Outsourcing Maintenance, Repair and Operationssha_yadNo ratings yet

- Coal MarketDocument79 pagesCoal MarketFarah Rizka Rahmatia100% (2)

- APAC ProspectusDocument84 pagesAPAC Prospectusshare818No ratings yet

- MBI Presentation - Chandershekher JoshiDocument8 pagesMBI Presentation - Chandershekher JoshiChander ShekherNo ratings yet

- Coal Handling OperationalDocument12 pagesCoal Handling Operationalmugiraharjo7No ratings yet

- DOID Delta Dunia Makmur TBK Presentation Material UBS November 2010Document19 pagesDOID Delta Dunia Makmur TBK Presentation Material UBS November 2010Arief PermanaNo ratings yet

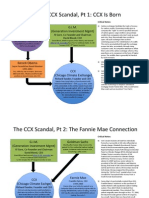

- CCX Scandal, Chicago Carbon ExchangeDocument4 pagesCCX Scandal, Chicago Carbon ExchangeKim HedumNo ratings yet

- FS Master Plan Kek CCCC PDFDocument135 pagesFS Master Plan Kek CCCC PDFAmilJuniwaluNo ratings yet

- PT. Pelindo 3 SyndicateDocument32 pagesPT. Pelindo 3 Syndicategalihdiadi-1No ratings yet

- Coal Outlook ReportDocument51 pagesCoal Outlook ReportSterios SouyoutzoglouNo ratings yet

- Feasibility - HDPE Drum - Costing Based On 2011 DataDocument8 pagesFeasibility - HDPE Drum - Costing Based On 2011 DataRammeshwar D Gupta100% (1)

- Indonesia Port Development: - Bilateral Maritime Forum 4Document8 pagesIndonesia Port Development: - Bilateral Maritime Forum 4Indra Degree KarimahNo ratings yet

- Agc 604/3 Operations StrategyDocument32 pagesAgc 604/3 Operations StrategyYeohNo ratings yet

- Mining Guide 2022Document166 pagesMining Guide 2022Bas KoroNo ratings yet

- Banpu - Annual Report - 2011Document162 pagesBanpu - Annual Report - 2011juli_0942080No ratings yet

- Reporting Coal Exploration FriederichMDocument73 pagesReporting Coal Exploration FriederichMDadan100% (1)

- KPI - Port of LADocument28 pagesKPI - Port of LAsambitpandaNo ratings yet

- PT Acset Indonusa TBK - Concrete & Semi Top Down Method PDFDocument82 pagesPT Acset Indonusa TBK - Concrete & Semi Top Down Method PDFGenius People100% (1)

- JP Morgan - Indonesia Coal Mining 2011Document39 pagesJP Morgan - Indonesia Coal Mining 2011KJPP ASRNo ratings yet

- FAQ On InvestmentDocument80 pagesFAQ On InvestmentIrka PlayingNo ratings yet

- Coal Trading: The BasicsDocument2 pagesCoal Trading: The BasicsBisto MasiloNo ratings yet

- 21-Project Teaser Diamond Mining Enoque 2020Document9 pages21-Project Teaser Diamond Mining Enoque 2020michel louis friedmanNo ratings yet

- The Coal Resource, A Comprehensive Overview of Coal (World Coal Institute)Document48 pagesThe Coal Resource, A Comprehensive Overview of Coal (World Coal Institute)alabamacoal100% (1)

- Coal Supply Pre-Qualified DocumentDocument14 pagesCoal Supply Pre-Qualified DocumentPT. Jayakhisma Globe IndonesiaNo ratings yet

- Mining Methods: PlotmakerDocument78 pagesMining Methods: PlotmakertamanimoNo ratings yet

- Ship Unloaders InfoDocument4 pagesShip Unloaders InfojagrutNo ratings yet

- Port Performance IndicatorsDocument20 pagesPort Performance IndicatorsPMA Vepery100% (1)

- Forward Planning For Coal BusinessDocument10 pagesForward Planning For Coal BusinessSyamsu Tri AtmokoNo ratings yet

- McKinsey Energy Insights Global Energy Perspective 2019 Reference Case SummaryDocument31 pagesMcKinsey Energy Insights Global Energy Perspective 2019 Reference Case SummaryOkwudiliNo ratings yet

- Pertamina Green ProductsDocument34 pagesPertamina Green ProductsMarsyaNo ratings yet

- Coal (From The Old English Term Col, Which Has Meant "Mineral of Fossilized Carbon" Since The 13thDocument6 pagesCoal (From The Old English Term Col, Which Has Meant "Mineral of Fossilized Carbon" Since The 13thJaydeep SinghNo ratings yet

- MSC ChemicalDocument50 pagesMSC Chemicalnida shahbazNo ratings yet

- Pressure Biotic MaterialDocument2 pagesPressure Biotic Materialsarath.kumarnmk930No ratings yet

- Nature and Occurrence of Coal SeamsDocument6 pagesNature and Occurrence of Coal SeamsSheshu Babu100% (2)

- CoalDocument7 pagesCoalببجي ببجيNo ratings yet

- Coal Materials and Energy PapersDocument23 pagesCoal Materials and Energy PapersRirinNo ratings yet

- Fossil Fuels Are Fuels Formed by Natural Resources Such As AnaerobicDocument11 pagesFossil Fuels Are Fuels Formed by Natural Resources Such As AnaerobicFrances Aila Toreja BalotocNo ratings yet

- Mazada Consortium LimitedDocument3 pagesMazada Consortium Limitedjowila5377No ratings yet

- Winning at New ProductsDocument24 pagesWinning at New Products劉緯文100% (1)

- GCE A - AS Level Biology A Topic Test - Biodiversity, Evolution and DiseaseDocument25 pagesGCE A - AS Level Biology A Topic Test - Biodiversity, Evolution and Diseasearfaat shahNo ratings yet

- Oo All MethodDocument35 pagesOo All Methodmeeraselvam19761970No ratings yet

- NCERT Exemplar Class 7 Maths IntegersDocument661 pagesNCERT Exemplar Class 7 Maths IntegersRohiniNo ratings yet

- Vichinsky Et Al.2019Document11 pagesVichinsky Et Al.2019Kuliah Semester 4No ratings yet

- 2013 - To and Fro. Modernism and Vernacular ArchitectureDocument246 pages2013 - To and Fro. Modernism and Vernacular ArchitecturesusanaNo ratings yet

- How To Query Asham Tele Points (Telebirr)Document13 pagesHow To Query Asham Tele Points (Telebirr)Fayisa ETNo ratings yet

- Sec ListDocument288 pagesSec ListTeeranun NakyaiNo ratings yet

- B737 SRM 51 - 40 - 08 Rep - Fiberglass OverlaysDocument6 pagesB737 SRM 51 - 40 - 08 Rep - Fiberglass OverlaysAlex CanizalezNo ratings yet

- MgF2 SolGelDocument8 pagesMgF2 SolGelumut bayNo ratings yet

- Chapter 2 Solutions - Power-Generation-OperationDocument11 pagesChapter 2 Solutions - Power-Generation-OperationKleilson Chagas50% (4)

- Variable Frequency DriveDocument8 pagesVariable Frequency DriveNAYEEM100% (1)

- SAP2000 Analysis - Computers and Structures, IncDocument6 pagesSAP2000 Analysis - Computers and Structures, IncshadabghazaliNo ratings yet

- The Standard Model Theory - Kreon Papathanasiou - ph4884Document30 pagesThe Standard Model Theory - Kreon Papathanasiou - ph4884Haigh RudeNo ratings yet

- Tecnicas Monitoreo CorrosionDocument8 pagesTecnicas Monitoreo CorrosionJavier GonzalezNo ratings yet

- Cn101386595-Chemical Synthesis Method of 10-Methoxyl-5H-Dibenz (B, F) AzapineDocument4 pagesCn101386595-Chemical Synthesis Method of 10-Methoxyl-5H-Dibenz (B, F) AzapineDipti DodiyaNo ratings yet

- SP Post ListDocument54 pagesSP Post ListJoel Eljo Enciso SaraviaNo ratings yet

- Risk Management Q1Document8 pagesRisk Management Q1Parth MuniNo ratings yet

- An Example of A Rating Scale To Q4Document4 pagesAn Example of A Rating Scale To Q4Zeeshan ch 'Hadi'No ratings yet

- Interweave Fiber Catalog Fall 2009Document56 pagesInterweave Fiber Catalog Fall 2009Interweave100% (1)

- NCLFNP - Mr. Robert McClelland CaseDocument4 pagesNCLFNP - Mr. Robert McClelland CaseAiresh Lamao50% (2)

- Jurnal: Ekonomi PembangunanDocument14 pagesJurnal: Ekonomi PembangunanAgus MelasNo ratings yet

- Creativity MCQDocument17 pagesCreativity MCQAmanVatsNo ratings yet

- Literature Review 1Document7 pagesLiterature Review 1api-609504422No ratings yet

- Las-Shs Gen - Chem Melc 1 q2 Week-1Document11 pagesLas-Shs Gen - Chem Melc 1 q2 Week-1Carl Baytola RatesNo ratings yet

- 3.Space-Activity BookDocument21 pages3.Space-Activity BookRania FarranNo ratings yet

- Self-Diagnosis With Advanced Hospital Management-IJRASETDocument5 pagesSelf-Diagnosis With Advanced Hospital Management-IJRASETIJRASETPublicationsNo ratings yet

- Chap 5 - MOMDocument27 pagesChap 5 - MOMladdooparmarNo ratings yet

- 02.03.05.06.01 - Manage Sales Rebate AgreementDocument11 pages02.03.05.06.01 - Manage Sales Rebate AgreementVinoth100% (1)