You might also like

- Tata Consultancy Service PDFDocument57 pagesTata Consultancy Service PDFyogica3537100% (1)

- AM-FM Reception TipsDocument3 pagesAM-FM Reception TipsKrishna Ghimire100% (1)

- OMM807100043 - 3 (PID Controller Manual)Document98 pagesOMM807100043 - 3 (PID Controller Manual)cengiz kutukcu100% (3)

- TCS Company AnaylysisDocument22 pagesTCS Company AnaylysisPatrick BowmanNo ratings yet

- PDFDocument1 pagePDFJaime Arroyo0% (1)

- Tata Consultancy ServicesDocument26 pagesTata Consultancy ServicesKashish Arora100% (2)

- Introduction To Soft Floor CoveringsDocument13 pagesIntroduction To Soft Floor CoveringsJothi Vel Murugan83% (6)

- Tata Consultancy ServicesDocument59 pagesTata Consultancy ServicesEntertainment OverloadedNo ratings yet

- Nasscom Strategic ReviewDocument25 pagesNasscom Strategic Reviewpappu.subscriptionNo ratings yet

- ParaphrasingDocument11 pagesParaphrasingAntiiSukmaNo ratings yet

- High Velocity Itsm: Agile It Service Management for Rapid Change in a World of Devops, Lean It and Cloud ComputingFrom EverandHigh Velocity Itsm: Agile It Service Management for Rapid Change in a World of Devops, Lean It and Cloud ComputingNo ratings yet

- Portland Cement: Standard Specification ForDocument9 pagesPortland Cement: Standard Specification ForHishmat Ezz AlarabNo ratings yet

- Grade 6 q2 Mathematics LasDocument151 pagesGrade 6 q2 Mathematics LasERIC VALLE80% (5)

- Infosys Technologies Limited: Automotive IndustryDocument19 pagesInfosys Technologies Limited: Automotive IndustrySharath ReddyNo ratings yet

- RedingtonDocument7 pagesRedingtonapi-3716851No ratings yet

- Tata Consultancy Services LimitedDocument21 pagesTata Consultancy Services Limitedsanjeev kumar100% (1)

- Model Personal StatementDocument2 pagesModel Personal StatementSwayam Tripathy100% (1)

- Business To Business MarketingDocument56 pagesBusiness To Business MarketingGaurav Kumar0% (1)

- Presentation To Investor / Analyst (Company Update)Document51 pagesPresentation To Investor / Analyst (Company Update)Shyam SunderNo ratings yet

- Company Profile: Indiainfoline MarketsDocument4 pagesCompany Profile: Indiainfoline MarketsDharmesh TrivediNo ratings yet

- EFY-Top100 Oct09 PDFDocument15 pagesEFY-Top100 Oct09 PDFvenkatesh_1829No ratings yet

- Tata Elxsi LTD: General OverviewDocument9 pagesTata Elxsi LTD: General Overviewakanksha morghadeNo ratings yet

- TCSDocument19 pagesTCSTanay SamantaNo ratings yet

- Intex Technologies (India) LTDDocument35 pagesIntex Technologies (India) LTDnitu36No ratings yet

- Global Aspects of ITES1Document41 pagesGlobal Aspects of ITES1Ajit ShindeNo ratings yet

- TCSDocument19 pagesTCSSuguna GuruNo ratings yet

- Abt CISCODocument2 pagesAbt CISCOSarat ChandraNo ratings yet

- TCS FaDocument28 pagesTCS FasunnyNo ratings yet

- Serial System LTD Annual Report 2015Document202 pagesSerial System LTD Annual Report 2015WeR1 Consultants Pte LtdNo ratings yet

- System Limited (Internation Business Report)Document10 pagesSystem Limited (Internation Business Report)Muhammad AsadNo ratings yet

- Eco ProjectDocument29 pagesEco ProjectAditya SharmaNo ratings yet

- TOP 10 IT DistributorsDocument5 pagesTOP 10 IT DistributorsMayur SutharNo ratings yet

- 1.1 Company & Process Details of KPIT Cummins, Hinjewadi PuneDocument65 pages1.1 Company & Process Details of KPIT Cummins, Hinjewadi PuneamarnathwissenNo ratings yet

- Asm BrochureDocument2 pagesAsm Brochuremsn1270No ratings yet

- ITM - Group Project - B3Document13 pagesITM - Group Project - B3uddhavkulkarniNo ratings yet

- Abridged Annual Report 2013 14 Reliance CommunicationsDocument96 pagesAbridged Annual Report 2013 14 Reliance CommunicationsVARBALNo ratings yet

- About GenpactDocument3 pagesAbout GenpactShreyans JainNo ratings yet

- Redington: Supply Chain Services Provider in Emerging MarketsDocument16 pagesRedington: Supply Chain Services Provider in Emerging Marketssantoshpania100% (1)

- AirtelDocument31 pagesAirtelRajiv KeshriNo ratings yet

- Presentation On Software Services in India: Group 8Document30 pagesPresentation On Software Services in India: Group 8yesh86No ratings yet

- Group 2 - ITC InfotechDocument15 pagesGroup 2 - ITC InfotechRohan KabraNo ratings yet

- FMP Stage 1Document27 pagesFMP Stage 1Rishabh srivastavNo ratings yet

- Airbnb ReportDocument10 pagesAirbnb Reportaslam khanNo ratings yet

- InternDocument9 pagesInternPalak HemnaniNo ratings yet

- ETA2UDocument25 pagesETA2UDaniel GhrossNo ratings yet

- Reliance Communications LTDDocument4 pagesReliance Communications LTDSahil JainNo ratings yet

- VoltasDocument8 pagesVoltasVISHWAS GOWDA H VNo ratings yet

- Notable Products and Services: HardwareDocument22 pagesNotable Products and Services: HardwareAnshi GuptaNo ratings yet

- Tech Mahindra Q1 Revenue Up 14%Document5 pagesTech Mahindra Q1 Revenue Up 14%WeR1 Consultants Pte LtdNo ratings yet

- Case Study TCSDocument19 pagesCase Study TCSMohammed Naqi Wasif0% (1)

- Annual Report 2011-12 Misi (1) TulipDocument65 pagesAnnual Report 2011-12 Misi (1) Tulipajx1979No ratings yet

- Infosys Technologies Limited: Automotive IndustryDocument19 pagesInfosys Technologies Limited: Automotive IndustryHarshpreet BhatiaNo ratings yet

- LID Power Solutions LTD ProfileDocument9 pagesLID Power Solutions LTD ProfileSharmileNo ratings yet

- WiproDocument4 pagesWiproritvikjindalNo ratings yet

- TVS Electric Shares PresentationDocument32 pagesTVS Electric Shares Presentationgixodoj234No ratings yet

- SAP NW Sol Catalogue 2007Document160 pagesSAP NW Sol Catalogue 2007rahul_alone149958No ratings yet

- Wipro LimtDocument10 pagesWipro LimtSupriye SabharwalNo ratings yet

- 121 Mahindra SatyamDocument4 pages121 Mahindra SatyamArpita YadavNo ratings yet

- IT Sector and Its CompaniesDocument11 pagesIT Sector and Its Companiespriyanka_joshi_31No ratings yet

- SAS InstituteDocument10 pagesSAS Instituteapi-3716851No ratings yet

- FIEM Annual Report 2014Document100 pagesFIEM Annual Report 2014preetilakhotiaNo ratings yet

- It/Ites Industry: G.V.Sandeep Cygnus Business Consulting and Research PVT LTDDocument22 pagesIt/Ites Industry: G.V.Sandeep Cygnus Business Consulting and Research PVT LTDdustinlarkNo ratings yet

- Role of Mis in BSNL Telecommunications 2Document21 pagesRole of Mis in BSNL Telecommunications 2ThaslyNazNo ratings yet

- BrandDocument24 pagesBrandamri21No ratings yet

- Scope and Impact of Industry On Indian EconomyDocument66 pagesScope and Impact of Industry On Indian Economysomiya kausualNo ratings yet

- Executive Placement Service Revenues World Summary: Market Values & Financials by CountryFrom EverandExecutive Placement Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Management Consulting Services Miscellaneous Revenues World Summary: Market Values & Financials by CountryFrom EverandManagement Consulting Services Miscellaneous Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Technical & Trade School Revenues World Summary: Market Values & Financials by CountryFrom EverandTechnical & Trade School Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- PDF Processed With Cutepdf Evaluation EditionDocument3 pagesPDF Processed With Cutepdf Evaluation EditionShyam SunderNo ratings yet

- Standalone Financial Results For March 31, 2016 (Result)Document11 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results For September 30, 2016 (Result)Document3 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Transcript of The Investors / Analysts Con Call (Company Update)Document15 pagesTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderNo ratings yet

- Investor Presentation For December 31, 2016 (Company Update)Document27 pagesInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- L Rexx PDFDocument9 pagesL Rexx PDFborisg3No ratings yet

- Age and Gender Detection Using Deep Learning: HYDERABAD - 501 510Document11 pagesAge and Gender Detection Using Deep Learning: HYDERABAD - 501 510ShyamkumarBannuNo ratings yet

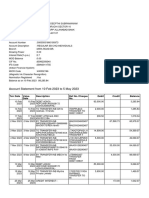

- Feb-May SBI StatementDocument2 pagesFeb-May SBI StatementAshutosh PandeyNo ratings yet

- Schematic Circuits: Section C - ElectricsDocument1 pageSchematic Circuits: Section C - ElectricsIonut GrozaNo ratings yet

- Pin Joint en PDFDocument1 pagePin Joint en PDFCicNo ratings yet

- Bulk Separator - V-1201 Method StatementDocument2 pagesBulk Separator - V-1201 Method StatementRoshin99No ratings yet

- WKS 8 & 9 - Industrial Dryer 2T 2020-2021Document26 pagesWKS 8 & 9 - Industrial Dryer 2T 2020-2021Mei Lamfao100% (1)

- Assembly and RiggingDocument52 pagesAssembly and RiggingPokemon Go0% (1)

- English ID Student S Book 1 - 015Document1 pageEnglish ID Student S Book 1 - 015Williams RoldanNo ratings yet

- DR - Rajinikanth - Pharmaceutical ValidationDocument54 pagesDR - Rajinikanth - Pharmaceutical Validationمحمد عطاNo ratings yet

- Video Course NotesDocument18 pagesVideo Course NotesSiyeon YeungNo ratings yet

- 10 - SHM, Springs, DampingDocument4 pages10 - SHM, Springs, DampingBradley NartowtNo ratings yet

- Civil Engineering Literature Review SampleDocument6 pagesCivil Engineering Literature Review Sampleea442225100% (1)

- CH 2 PDFDocument85 pagesCH 2 PDFSajidNo ratings yet

- 5 Teacher Induction Program - Module 5Document27 pages5 Teacher Induction Program - Module 5LAZABELLE BAGALLON0% (1)

- Technical Textile and SustainabilityDocument5 pagesTechnical Textile and SustainabilityNaimul HasanNo ratings yet

- KV4BBSR Notice ContractuaL Interview 2023-24Document9 pagesKV4BBSR Notice ContractuaL Interview 2023-24SuchitaNo ratings yet

- List of Institutions With Ladderized Program Under Eo 358 JULY 2006 - DECEMBER 31, 2007Document216 pagesList of Institutions With Ladderized Program Under Eo 358 JULY 2006 - DECEMBER 31, 2007Jen CalaquiNo ratings yet

- 96 Dec2018 NZGeoNews PDFDocument139 pages96 Dec2018 NZGeoNews PDFAditya PrasadNo ratings yet

- CNC Manuel de Maintenance 15i 150i ModelADocument526 pagesCNC Manuel de Maintenance 15i 150i ModelASebautomatismeNo ratings yet

- Busbusilak - ResearchPlan 3Document4 pagesBusbusilak - ResearchPlan 3zkcsswddh6No ratings yet

- IELTS Letter Writing TipsDocument7 pagesIELTS Letter Writing Tipsarif salmanNo ratings yet