You might also like

- Lecture OutlineDocument55 pagesLecture OutlineShweta ChaudharyNo ratings yet

- Invtemp 140909235749 Phpapp01Document92 pagesInvtemp 140909235749 Phpapp01Amit VermaNo ratings yet

- InventoryDocument46 pagesInventorySoumitra ChakrabortyNo ratings yet

- Unit-3 (Industrial Management)Document48 pagesUnit-3 (Industrial Management)Ankur Agrawal0% (1)

- Inventory ManagementDocument52 pagesInventory Managementsatyamchoudhary2004No ratings yet

- Inventory ControlDocument26 pagesInventory ControlhajarawNo ratings yet

- Material Management: An Important Front For Cost SavingDocument67 pagesMaterial Management: An Important Front For Cost SavingAlexNo ratings yet

- What Is Inventory?: Parts and Materials Available Capacity Human ResourcesDocument35 pagesWhat Is Inventory?: Parts and Materials Available Capacity Human ResourcesHaider ShadfanNo ratings yet

- Cycle InventoryDocument13 pagesCycle InventoryUmang ZehenNo ratings yet

- Inventory & Risk PoolingDocument64 pagesInventory & Risk PoolingMohit GuptaNo ratings yet

- InventoryDocument36 pagesInventorynidhi_friend1020032748No ratings yet

- Inventory Planning: Nazmun NaharDocument29 pagesInventory Planning: Nazmun NaharKamrulHassanNo ratings yet

- Chapter 17. Inventory Control: Inventory Is The Stock of Any Item or Resource Used in AnDocument21 pagesChapter 17. Inventory Control: Inventory Is The Stock of Any Item or Resource Used in AnHassan SalamaNo ratings yet

- Inventory ControlDocument35 pagesInventory ControlSyed Haseeb AhmadNo ratings yet

- Inventory Management: Tanay Agrawal Sripal Jain Sudeepta Borah Mayank BahetiDocument32 pagesInventory Management: Tanay Agrawal Sripal Jain Sudeepta Borah Mayank BahetirnaganirmitaNo ratings yet

- Inventory ControlDocument36 pagesInventory ControlAnkur YashNo ratings yet

- 8 Managing of Economics of ScaleDocument38 pages8 Managing of Economics of ScaleDwita Permatasari100% (1)

- Inventory Management 1 PDFDocument31 pagesInventory Management 1 PDFfew.fearlessNo ratings yet

- Unit 3 Industrial ManagementDocument48 pagesUnit 3 Industrial ManagementImad AghilaNo ratings yet

- CH 15 Inventory ManagementDocument21 pagesCH 15 Inventory ManagementAshwin MishraNo ratings yet

- Inventory ManagementDocument47 pagesInventory ManagementDhivaakar KrishnanNo ratings yet

- IM 322 Inventory Management: Chapter 3 Economic Order Quantity Model (EOQ)Document24 pagesIM 322 Inventory Management: Chapter 3 Economic Order Quantity Model (EOQ)es_sajiNo ratings yet

- UNIT-3: Inventory ControlDocument48 pagesUNIT-3: Inventory Controlgau_1119No ratings yet

- Chapter 6 Inventory ControlDocument35 pagesChapter 6 Inventory ControlImad GhoriNo ratings yet

- InventoryDocument7 pagesInventoryvinit PatidarNo ratings yet

- Chap 015Document43 pagesChap 015Ponkiya AnkitNo ratings yet

- Chap015 Inventory ControlDocument43 pagesChap015 Inventory ControlKhushbu ChandnaniNo ratings yet

- Inventory PPT (EOQ)Document38 pagesInventory PPT (EOQ)drajingoNo ratings yet

- Dr. Abe Feinberg's Inventory NotesDocument5 pagesDr. Abe Feinberg's Inventory NotesBeautyfull Naina MehtaNo ratings yet

- Ch08 - InventoryDocument111 pagesCh08 - InventoryelakkiyaNo ratings yet

- Cycle InventoryDocument75 pagesCycle InventoryDeep DaveNo ratings yet

- InventoryDocument69 pagesInventoryPriya PintoNo ratings yet

- Chapter 20 - PPT OutlineDocument5 pagesChapter 20 - PPT OutlineJanice TangNo ratings yet

- Chapter-20 Inventory ManagementDocument20 pagesChapter-20 Inventory ManagementPooja SheoranNo ratings yet

- Unit 4. Inventory Analysis and ControlDocument57 pagesUnit 4. Inventory Analysis and Controlskannanmec100% (1)

- Inventory Management: Bus Adm 370 - CHP 12 Inventory MGMTDocument7 pagesInventory Management: Bus Adm 370 - CHP 12 Inventory MGMTSidharth GoyalNo ratings yet

- 05 Inventory ManagementDocument47 pages05 Inventory ManagementjackNo ratings yet

- Independent Demand SystemsDocument40 pagesIndependent Demand SystemsAraNo ratings yet

- Inventory Management: Presented By: Apple MagpantayDocument31 pagesInventory Management: Presented By: Apple MagpantayRuth Ann DimalaluanNo ratings yet

- Inventory Control: Operations ManagementDocument43 pagesInventory Control: Operations ManagementRahul KhannaNo ratings yet

- The Basic Economic Order Quantity ModelDocument13 pagesThe Basic Economic Order Quantity ModelRichardson HolderNo ratings yet

- SCM CycleDocument45 pagesSCM CycleMuhammad DuraidNo ratings yet

- Materials Management EssentialsDocument46 pagesMaterials Management Essentialstemesgen yohannesNo ratings yet

- Inventory PDFDocument22 pagesInventory PDFKatrina MarzanNo ratings yet

- Inventory OptimizationDocument83 pagesInventory OptimizationAbdul AzizNo ratings yet

- 5 1 Inventory ManagementDocument42 pages5 1 Inventory Managementhrithima100% (13)

- Inventory ManagementDocument40 pagesInventory ManagementsaloniNo ratings yet

- Material de Inventarios1Document13 pagesMaterial de Inventarios1wam30959No ratings yet

- OM M8 Inventory Management HandoutDocument39 pagesOM M8 Inventory Management HandoutChandan SainiNo ratings yet

- IE305 CH 4 Inventory and Economic Order QuantityDocument52 pagesIE305 CH 4 Inventory and Economic Order Quantitymuhendis_8900100% (1)

- Inventory Management EOQDocument55 pagesInventory Management EOQsushant chaudharyNo ratings yet

- Managing Economies of Scale in A Supply ChainDocument76 pagesManaging Economies of Scale in A Supply ChainAvinash Kumar80% (5)

- InventoryDocument75 pagesInventoryAlyssa DecanoNo ratings yet

- Inventory Control EOQ ModelDocument44 pagesInventory Control EOQ ModelHOD MEC BVC Engineering Colelge OdalarevuNo ratings yet

- Understanding Inventory Management ConceptsDocument8 pagesUnderstanding Inventory Management ConceptsNirav PatelNo ratings yet

- Inventory Management 21 PankajDocument34 pagesInventory Management 21 PankajPankaj Tadaskar TadaskarNo ratings yet

- Inventory Management-I PPT 16-18Document31 pagesInventory Management-I PPT 16-18Prateek KonvictedNo ratings yet

- Managing Economies of Scale Cycle InventoryDocument33 pagesManaging Economies of Scale Cycle InventoryRohit DuttaNo ratings yet

- Inventory IIDocument37 pagesInventory IISuraj MishraNo ratings yet

- BestDocument25 pagesBestadmasuNo ratings yet

- Chapter 2 ForecastingDocument42 pagesChapter 2 Forecastingworkumogess3100% (1)

- Chap.4 - Inventory Management EditedDocument44 pagesChap.4 - Inventory Management EditedadmasuNo ratings yet

- EsentialDocument57 pagesEsentialadmasuNo ratings yet

- Renewal ReceiptDocument2 pagesRenewal ReceiptAmanSharmaNo ratings yet

- ORMS - 1 - Foundation DataDocument55 pagesORMS - 1 - Foundation DataLoki Jayanagar BlrNo ratings yet

- 02b Deterministic Inventory ModelsDocument51 pages02b Deterministic Inventory ModelskaustavpalNo ratings yet

- Pooja 2Document2 pagesPooja 2KAPASAN DEKHONo ratings yet

- Sweet Employee and Company ProfileDocument67 pagesSweet Employee and Company ProfileAchibabaNo ratings yet

- MonorailDocument13 pagesMonorailAMIT0048No ratings yet

- Sovachem & Co.: Tax InvoiceDocument1 pageSovachem & Co.: Tax InvoiceSohamNo ratings yet

- Application Form For Membership - New 2017Document1 pageApplication Form For Membership - New 2017Instech Premier Sdn BhdNo ratings yet

- Customer Satisfaction Towards PAYtm ServicesDocument53 pagesCustomer Satisfaction Towards PAYtm ServicesVignesh Kumar Voleti69% (13)

- Legal NoticeDocument4 pagesLegal NoticeIshwari SabadraNo ratings yet

- Quotation: Kentex CargoDocument2 pagesQuotation: Kentex CargoMalueth AnguiNo ratings yet

- Rwservlet PDFDocument1 pageRwservlet PDFRatna chourasiyaNo ratings yet

- TAX 1016 Lesson TWODocument8 pagesTAX 1016 Lesson TWOMonica MonicaNo ratings yet

- Klaus Vogel On Double Taxation Conventions - BrochureDocument4 pagesKlaus Vogel On Double Taxation Conventions - Brochuremejocoba820% (1)

- Transporation and Developing A Transportation Network For Supply ChainDocument2 pagesTransporation and Developing A Transportation Network For Supply ChainDhruv SahneyNo ratings yet

- UPI - Unified Payment InterfaceDocument9 pagesUPI - Unified Payment Interfacemohit0744No ratings yet

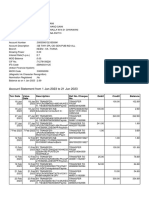

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilNo ratings yet

- Mrs. KAMLESH SINGH bank account statement from Jan 2019 to Aug 2019Document4 pagesMrs. KAMLESH SINGH bank account statement from Jan 2019 to Aug 2019Saurabh SinghNo ratings yet

- OpTransactionHistoryUX324 01 2020 PDFDocument4 pagesOpTransactionHistoryUX324 01 2020 PDFHimavanth ReddyNo ratings yet

- MT940 Bank Format ExplainedDocument23 pagesMT940 Bank Format Explainedvickygupta12381% (16)

- Accounting Errors and Dentist Business TransactionsDocument1 pageAccounting Errors and Dentist Business TransactionsJordy TangNo ratings yet

- Final Payslip of Circle For 7-17Document11 pagesFinal Payslip of Circle For 7-17Manas Kumar SahooNo ratings yet

- Profile of Dnanir Global Logistic Services in JeddahDocument17 pagesProfile of Dnanir Global Logistic Services in JeddahIlyas ShareefNo ratings yet

- Transactions List: Stefan Bulgariu RO31BRDE240SV19357632400 RON Stefan BulgariuDocument3 pagesTransactions List: Stefan Bulgariu RO31BRDE240SV19357632400 RON Stefan BulgariuBulgariu StefanNo ratings yet

- No:-0003597994 - Issue Date 14.08.2020: Alliance Broadband Services Pvt. LTDDocument1 pageNo:-0003597994 - Issue Date 14.08.2020: Alliance Broadband Services Pvt. LTDsomcmsNo ratings yet

- Saral Nivesh POS plan detailsDocument1 pageSaral Nivesh POS plan detailsDeepak VaishnavNo ratings yet

- Account statement details for Panyam BalajiDocument4 pagesAccount statement details for Panyam BalajibalajiNo ratings yet

- E-Accounting & Tax Course with GST, IT & PTDocument2 pagesE-Accounting & Tax Course with GST, IT & PTWedsa KumariNo ratings yet

- Website:www - Mahadiscom.in: MSEDCL Call Center: 18002333435 18001023435 1912Document3 pagesWebsite:www - Mahadiscom.in: MSEDCL Call Center: 18002333435 18001023435 1912Chetan RamtekeNo ratings yet

- Production Planning and ControlDocument10 pagesProduction Planning and Controljnsingh12345No ratings yet