You might also like

- Service Tax BrajeshDocument28 pagesService Tax BrajeshVenkat ReddyNo ratings yet

- Service TaxDocument7 pagesService TaxmurusaNo ratings yet

- Final Tax Sem 4PAYMENT, REGISTRATION AND RETURNS OF SERVICE TAXDocument32 pagesFinal Tax Sem 4PAYMENT, REGISTRATION AND RETURNS OF SERVICE TAXkarthika kounderNo ratings yet

- Service Tax: Some of The Major Services That Come Under The Ambit of Service Tax AreDocument7 pagesService Tax: Some of The Major Services That Come Under The Ambit of Service Tax AreChetan ShivankarNo ratings yet

- Service Tax: Aiaims Mms-ADocument31 pagesService Tax: Aiaims Mms-AAbbas Haider NaqviNo ratings yet

- Liability of Service TaxDocument7 pagesLiability of Service TaxkasiriverNo ratings yet

- Provisons On Service TaxDocument37 pagesProvisons On Service TaxSunita NitinNo ratings yet

- Service Tax1Document8 pagesService Tax1Suman pendharkarNo ratings yet

- Indian Service TaxDocument13 pagesIndian Service Taxanon_993677No ratings yet

- Service TaxDocument3 pagesService Taxapi-3822396No ratings yet

- What Is Service Tax ?Document15 pagesWhat Is Service Tax ?Nawab SahabNo ratings yet

- Service Tax Act - FAQsDocument80 pagesService Tax Act - FAQsvarada2No ratings yet

- Bustax 4Document117 pagesBustax 4Frances AgustinNo ratings yet

- Service Tax - 1.1Document18 pagesService Tax - 1.1Arun ChopraNo ratings yet

- Indirec TaxDocument8 pagesIndirec TaxSubashNo ratings yet

- Payment of Service Tax Under Reverse Charge - A Comprehensive StudyDocument13 pagesPayment of Service Tax Under Reverse Charge - A Comprehensive Studyav_meshramNo ratings yet

- Administration of Value Added Tax-VatDocument13 pagesAdministration of Value Added Tax-VatRuth NyawiraNo ratings yet

- Service Tax: Q.No.1. What Is The Need of Introduction of Service Tax?Document5 pagesService Tax: Q.No.1. What Is The Need of Introduction of Service Tax?Kiran RaviNo ratings yet

- 2 Service TaxDocument10 pages2 Service TaxArchana ThirunagariNo ratings yet

- C1 Indirect Taxes: Service TaxDocument29 pagesC1 Indirect Taxes: Service TaxporzvtzoNo ratings yet

- BGM - ST Audit - CA Bimal Jain 26042014Document13 pagesBGM - ST Audit - CA Bimal Jain 26042014rohitNo ratings yet

- Presentation On Service Tax AmendmentsDocument19 pagesPresentation On Service Tax AmendmentsSmriti KhannaNo ratings yet

- 1 Budget Impact 2012-13Document5 pages1 Budget Impact 2012-13Rajkamal TiwariNo ratings yet

- Project Report ON Service Tax: Information Technology ProgrammeDocument19 pagesProject Report ON Service Tax: Information Technology ProgrammemayankkrishnaNo ratings yet

- Answer 4: Custom DutyDocument3 pagesAnswer 4: Custom DutyAshlee RobertsNo ratings yet

- Service TAXDocument27 pagesService TAXSamiya KhanNo ratings yet

- Service Tax NotesDocument24 pagesService Tax Notesfaraznaqvi100% (1)

- Reverse Charge Mechanism by Bimal Jain Tax ExpertDocument4 pagesReverse Charge Mechanism by Bimal Jain Tax ExpertYogesh ChaudhariNo ratings yet

- CIR Vs CADocument7 pagesCIR Vs CAChrissyNo ratings yet

- Group Assignment - April 23Document16 pagesGroup Assignment - April 23DIVA RTHININo ratings yet

- Chapter 1. Overview of Service Tax: Constitutional Validity and ConceptsDocument38 pagesChapter 1. Overview of Service Tax: Constitutional Validity and ConceptsPrateek UpadhyayNo ratings yet

- Taxes in IndiaDocument6 pagesTaxes in IndiaRAJIV MURALNo ratings yet

- Sopore Law CollegeDocument7 pagesSopore Law Collegelone NasirNo ratings yet

- Sales TaxDocument52 pagesSales TaxSavan DesaiNo ratings yet

- What Is GSTDocument98 pagesWhat Is GSTNorasyikin OsmanNo ratings yet

- Service Tax Exemptions Including SEZDocument52 pagesService Tax Exemptions Including SEZrabiyaniNo ratings yet

- Withholding Tax: Period of Payment of TaxDocument4 pagesWithholding Tax: Period of Payment of TaxlegendNo ratings yet

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- Servicetaxandvat 130420194223 Phpapp01Document65 pagesServicetaxandvat 130420194223 Phpapp01Ram ShiralkarNo ratings yet

- Service TaxDocument17 pagesService Taxvenky_1986100% (2)

- Reverse Charge in Service TaxDocument14 pagesReverse Charge in Service TaxvishalsolsheNo ratings yet

- General Tax Liabilities of Domestic CorpsDocument5 pagesGeneral Tax Liabilities of Domestic CorpsCora EleazarNo ratings yet

- Assessment 1 - Written or Oral QuestionsDocument7 pagesAssessment 1 - Written or Oral Questionswilson garzonNo ratings yet

- Public CHAPTER 4Document15 pagesPublic CHAPTER 4embiale ayaluNo ratings yet

- Stax ManualDocument97 pagesStax ManualSamartha Raj SinghNo ratings yet

- Office of The Commissioner of Service Tax, Delhi-I 17-B, IAEA House, Indraprastha Estate, New Delhi - 110 002Document11 pagesOffice of The Commissioner of Service Tax, Delhi-I 17-B, IAEA House, Indraprastha Estate, New Delhi - 110 002pmNo ratings yet

- Brief Introduction: Levy Whether Constitutionally Valid?Document11 pagesBrief Introduction: Levy Whether Constitutionally Valid?nishantjain95No ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- Practice Note No.01/2019 Withholding Tax On Payment For Goods and Services As Per Income Tax Act, Cap 332Document16 pagesPractice Note No.01/2019 Withholding Tax On Payment For Goods and Services As Per Income Tax Act, Cap 332musaNo ratings yet

- PWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionDocument5 pagesPWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionAnonymous FnM14a0No ratings yet

- VAT GUIDE 2nd EditionDocument28 pagesVAT GUIDE 2nd EditionLoretta Wise100% (1)

- Cir Vs CA and ComarsecoDocument2 pagesCir Vs CA and ComarsecoEllen Glae DaquipilNo ratings yet

- Corporate Income TaxDocument14 pagesCorporate Income Tax36. Lê Minh Phương 12A3No ratings yet

- Analysis of Income Tax in AfghanistanDocument47 pagesAnalysis of Income Tax in Afghanistanmasoud_dostNo ratings yet

- Assad Associates VAT Act 2014Document9 pagesAssad Associates VAT Act 2014Marc MarcoNo ratings yet

- Withholding Tax Rates MalawiDocument2 pagesWithholding Tax Rates Malawianraomca100% (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Chapter 3 - Events After The Reporting PeriodDocument8 pagesChapter 3 - Events After The Reporting PeriodNURKHAIRUNNISANo ratings yet

- Chapter 4 - Company TaxationDocument7 pagesChapter 4 - Company TaxationNURKHAIRUNNISANo ratings yet

- Mindmap - Revenue RecognitionDocument1 pageMindmap - Revenue RecognitionNURKHAIRUNNISANo ratings yet

- Mindmap - Accounting Policies, Changes in Accounting Estimates & ErrorsDocument1 pageMindmap - Accounting Policies, Changes in Accounting Estimates & ErrorsNURKHAIRUNNISANo ratings yet

- Mindmap - The Conceptual FrameworkDocument1 pageMindmap - The Conceptual FrameworkNURKHAIRUNNISANo ratings yet

- Chapter 1 - Basis Period and Change in Accounting DatesDocument7 pagesChapter 1 - Basis Period and Change in Accounting DatesNURKHAIRUNNISA100% (3)

- Chapter 2 - Industrial Building AllowanceDocument3 pagesChapter 2 - Industrial Building AllowanceNURKHAIRUNNISANo ratings yet

- Chapter 3 - Agriculture AllowancesDocument3 pagesChapter 3 - Agriculture AllowancesNURKHAIRUNNISA100% (2)

- Assignment - Fundamental of ManagementDocument8 pagesAssignment - Fundamental of ManagementNURKHAIRUNNISANo ratings yet

- Assignment - EntrepreneurshipDocument2 pagesAssignment - EntrepreneurshipNURKHAIRUNNISANo ratings yet

- Assignment - StatisticDocument7 pagesAssignment - StatisticNURKHAIRUNNISA0% (1)

- Assignment - Accounting TheoryDocument25 pagesAssignment - Accounting TheoryNURKHAIRUNNISA75% (4)

- Assignment - EntrepreneurshipDocument71 pagesAssignment - EntrepreneurshipNURKHAIRUNNISA100% (2)

- Assignment - Commercial LawDocument15 pagesAssignment - Commercial LawNURKHAIRUNNISANo ratings yet

- TaxDocuments 20221231D 1680486197406 0Document10 pagesTaxDocuments 20221231D 1680486197406 0J CNo ratings yet

- Case Laws May 2014Document7 pagesCase Laws May 2014Anamika Chauhan VermaNo ratings yet

- CPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/LlamadoDocument12 pagesCPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/LlamadoEdma Glory MacadaagNo ratings yet

- Collector Vs HendersonDocument1 pageCollector Vs HendersonLisa GarciaNo ratings yet

- ACT Yearly BillDocument2 pagesACT Yearly BillNarenNo ratings yet

- CIR V Acesite Hotel Corp.Document4 pagesCIR V Acesite Hotel Corp.'mhariie-mhAriie TOotNo ratings yet

- TM 4Document5 pagesTM 4Jai VermaNo ratings yet

- 24 - 38221544103291 SCR GuntupalliDocument3 pages24 - 38221544103291 SCR GuntupalliAbhishek DahiyaNo ratings yet

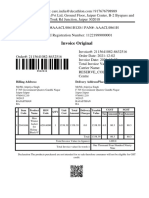

- InvoiceDocument1 pageInvoiceatipriya choudharyNo ratings yet

- LP 8 TaxationDocument2 pagesLP 8 TaxationJames CorpuzNo ratings yet

- GST Returns Reconciliation - MALLESHAM GAMPADocument27 pagesGST Returns Reconciliation - MALLESHAM GAMPArakianand007No ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Abhay ThakurNo ratings yet

- Bid Form Price ScheduleDocument3 pagesBid Form Price ScheduleMARLON LIMNo ratings yet

- Q Unfortunately, The Legislative Branch Failed To Amend Under Ra No. 10963 (Train Law) The Tax Rate With Respect To Rfcs. 27Document3 pagesQ Unfortunately, The Legislative Branch Failed To Amend Under Ra No. 10963 (Train Law) The Tax Rate With Respect To Rfcs. 27Rosemarie CruzNo ratings yet

- 18 - Royalty Payment ScheduleDocument2 pages18 - Royalty Payment ScheduleDJ DogasNo ratings yet

- Suplement To G Card ExamDocument35 pagesSuplement To G Card ExamCalwin ParthibarajNo ratings yet

- Sundar Shetty: Eligibility Comes From Efforts, Luck Comes From Opportunities L - 1Document36 pagesSundar Shetty: Eligibility Comes From Efforts, Luck Comes From Opportunities L - 1Abhay GroverNo ratings yet

- Salceda Briefer On The CREATE Veto 03262021 FormattedDocument3 pagesSalceda Briefer On The CREATE Veto 03262021 FormattedJeorge VerbaNo ratings yet

- MohsinUmair&Co Services PortfolioDocument2 pagesMohsinUmair&Co Services PortfolioSunnyNo ratings yet

- Tariff TerminologyDocument11 pagesTariff TerminologyRonnie Magsino100% (1)

- 2000 June 2006 (Back)Document1 page2000 June 2006 (Back)Rica Santos-vallesteroNo ratings yet

- Meenu Chopra Income Tax BasicsDocument66 pagesMeenu Chopra Income Tax BasicsRvi Mahay100% (1)

- Payment Receipt: Applicant DetailsDocument1 pagePayment Receipt: Applicant Detailsakhil SrinadhuNo ratings yet

- (D) The Provisions of Taxation in The Philippine Constitution Are Grants of Power and Not Limitations On Taxing PowersDocument44 pages(D) The Provisions of Taxation in The Philippine Constitution Are Grants of Power and Not Limitations On Taxing PowersCyril John RamosNo ratings yet

- 3 Percentages (II) : Net Chargeable Income Tax RateDocument2 pages3 Percentages (II) : Net Chargeable Income Tax Rate(4C27) Wong Ching Tung, Zoey 20181D043spss.hkNo ratings yet

- Shri Paresh Parekh, Chartered Accountants, Partner, Ernst & Young Pvt. LTDDocument46 pagesShri Paresh Parekh, Chartered Accountants, Partner, Ernst & Young Pvt. LTDSridharRaoNo ratings yet

- Chapter 1-Introduction To Taxation PDFDocument7 pagesChapter 1-Introduction To Taxation PDFAbraham ChinNo ratings yet

- TDS - Applicability On Any Type of Development AgreementDocument2 pagesTDS - Applicability On Any Type of Development Agreementparasshah.kljNo ratings yet

- Belete Addis Characterization of Taxable Units and Tax Bases 'A'Document35 pagesBelete Addis Characterization of Taxable Units and Tax Bases 'A'EmshawNo ratings yet

- CIR Vs LincolnDocument2 pagesCIR Vs LincolnAmee Bagtang-dapingNo ratings yet