You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Google Book Search ProjectDocument1,063 pagesGoogle Book Search ProjectSubhro ChatterjeeNo ratings yet

- Aami Chanchal He by Buddhadeb Basu BdeBoDocument109 pagesAami Chanchal He by Buddhadeb Basu BdeBoDipesh Chandra BaruaNo ratings yet

- Infrastructure Health in Civil EngineeringDocument684 pagesInfrastructure Health in Civil EngineeringDipesh Chandra Barua100% (1)

- Ce Formulas PDFDocument18 pagesCe Formulas PDFLouisgospel EnriquezNo ratings yet

- Jiban Ujjiban Salil ChowdhuryDocument113 pagesJiban Ujjiban Salil ChowdhuryDipesh Chandra BaruaNo ratings yet

- Lateral Pile Analyis With PY Curves - Newton Excel Bach, Not (Just) An Excel BlogDocument8 pagesLateral Pile Analyis With PY Curves - Newton Excel Bach, Not (Just) An Excel BlogDipesh Chandra BaruaNo ratings yet

- Akanka Natak 2 Manoj MitraDocument244 pagesAkanka Natak 2 Manoj MitraDipesh Chandra BaruaNo ratings yet

- Bangla Theatrer Darshan ChowdhuryDocument438 pagesBangla Theatrer Darshan ChowdhuryDipesh Chandra BaruaNo ratings yet

- Bipodjonok Baro by Nachiketa ChakrabortyDocument173 pagesBipodjonok Baro by Nachiketa ChakrabortyDipesh Chandra BaruaNo ratings yet

- Bijon Bhattacharya by DR Rubel AnsariDocument15 pagesBijon Bhattacharya by DR Rubel AnsariDipesh Chandra BaruaNo ratings yet

- CFD - BatheDocument781 pagesCFD - Batheoliviasaa100% (1)

- (Lectu 2Document969 pages(Lectu 2Dipesh Chandra BaruaNo ratings yet

- Lateral Load Test Pile - General Arrangement & Test ProcedureDocument7 pagesLateral Load Test Pile - General Arrangement & Test ProcedureDipesh Chandra BaruaNo ratings yet

- Finite Element Analysis - Degraded Concrete Structures (Csni-R99-1) (1998)Document365 pagesFinite Element Analysis - Degraded Concrete Structures (Csni-R99-1) (1998)Dipesh Chandra BaruaNo ratings yet

- PaycheckDocument6 pagesPaycheckDipesh Chandra BaruaNo ratings yet

- Payment of Wages (A) Bill - 2016Document4 pagesPayment of Wages (A) Bill - 2016Dipesh Chandra BaruaNo ratings yet

- Govt Passes Ordinance To Pay Wages Digitally or Through Cheques - Rajya Sabha TVDocument10 pagesGovt Passes Ordinance To Pay Wages Digitally or Through Cheques - Rajya Sabha TVDipesh Chandra BaruaNo ratings yet

- WSG Type Modular Expansion Joints A StudDocument74 pagesWSG Type Modular Expansion Joints A StudDipesh Chandra BaruaNo ratings yet

- Govt Eyes Mandatory Cashless Payments of Wages in Some Sectors - LivemintDocument6 pagesGovt Eyes Mandatory Cashless Payments of Wages in Some Sectors - LivemintDipesh Chandra BaruaNo ratings yet

- Govt Clears Ordinance, Companies Can Now Pay Salary Via E-Mode, Cheques - The Indian ExpressDocument12 pagesGovt Clears Ordinance, Companies Can Now Pay Salary Via E-Mode, Cheques - The Indian ExpressDipesh Chandra BaruaNo ratings yet

- How To Profit From Gold Prices - Profit Hunter NewsletterDocument2 pagesHow To Profit From Gold Prices - Profit Hunter NewsletterDipesh Chandra BaruaNo ratings yet

- Government Clarification On Amendment To Payment of Wages ActDocument2 pagesGovernment Clarification On Amendment To Payment of Wages ActDipesh Chandra BaruaNo ratings yet

- Govt Extend Exemptions 14nov2016Document1 pageGovt Extend Exemptions 14nov2016Dipesh Chandra BaruaNo ratings yet

- Bill Summary - Payment of WagesDocument1 pageBill Summary - Payment of WagesDipesh Chandra BaruaNo ratings yet

- StockSelect Order PageDocument43 pagesStockSelect Order PageDipesh Chandra BaruaNo ratings yet

- In The Customs Excise & Service Tax Appellate Tribunal West Block No.2, R. K. Puram, New Delhi-110066Document10 pagesIn The Customs Excise & Service Tax Appellate Tribunal West Block No.2, R. K. Puram, New Delhi-110066Dipesh Chandra BaruaNo ratings yet

- Government Clarification On Amendment To Payment of Wages Act - The Synthetic & Rayon Textiles Export Promotion CouncilDocument4 pagesGovernment Clarification On Amendment To Payment of Wages Act - The Synthetic & Rayon Textiles Export Promotion CouncilDipesh Chandra BaruaNo ratings yet

- grivanceFAQ PGPORTAL PDFDocument4 pagesgrivanceFAQ PGPORTAL PDFALOK SHUKLANo ratings yet

- WA0032 RBI NotificationDocument3 pagesWA0032 RBI NotificationPGurusNo ratings yet

- Explanatory NoteDocument6 pagesExplanatory NoteDipesh Chandra BaruaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Suparco+ KRL Test Ques For Electrical EngrzDocument5 pagesSuparco+ KRL Test Ques For Electrical Engrzمحمد فصیح آفتابNo ratings yet

- Gpa 2145Document15 pagesGpa 2145Sergio David Ruiz100% (1)

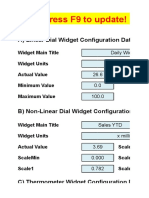

- Excel Dashboard WidgetsDocument47 pagesExcel Dashboard WidgetskhincowNo ratings yet

- Disney Channel JRDocument14 pagesDisney Channel JRJonna Parane TrongcosoNo ratings yet

- MCQ in Services MarketingDocument83 pagesMCQ in Services Marketingbatuerem0% (1)

- Artikel Jurnal - Fundamental Differences of Transition To Industry 4.0 From Previous Industrial RevolutionsDocument9 pagesArtikel Jurnal - Fundamental Differences of Transition To Industry 4.0 From Previous Industrial RevolutionsJohny DoelNo ratings yet

- Builder's Greywater Guide Branched DrainDocument4 pagesBuilder's Greywater Guide Branched DrainGreen Action Sustainable Technology GroupNo ratings yet

- Aesculap: F E S SDocument28 pagesAesculap: F E S SEcole AcharafNo ratings yet

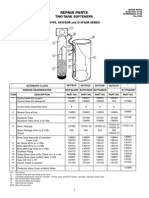

- Star S07FS32DR Water Softener Repair PartsDocument1 pageStar S07FS32DR Water Softener Repair PartsBillNo ratings yet

- JonWeisseBUS450 04 HPDocument3 pagesJonWeisseBUS450 04 HPJonathan WeisseNo ratings yet

- Smart Lighting Market Analysis and Forecast 2025 by Global Marketing InsightsDocument5 pagesSmart Lighting Market Analysis and Forecast 2025 by Global Marketing InsightsEko Hadi Susanto100% (1)

- !K Kanji Kaku - StrokesDocument18 pages!K Kanji Kaku - StrokeschingkakaNo ratings yet

- Product Data Sheet: Linear Switch - iSSW - 2 C/O - 20A - 250 V AC - 3 PositionsDocument2 pagesProduct Data Sheet: Linear Switch - iSSW - 2 C/O - 20A - 250 V AC - 3 PositionsMR. TNo ratings yet

- Panama Canal Requirements N10-2018Document11 pagesPanama Canal Requirements N10-2018Anca Geanina100% (1)

- Numerical Ability - Data Interpretation 3: 25 QuestionsDocument6 pagesNumerical Ability - Data Interpretation 3: 25 QuestionsAvishek01No ratings yet

- G12gasa Group5 PR2Document7 pagesG12gasa Group5 PR2Lizley CordovaNo ratings yet

- Eurocode 6 How To Design Masonry Structures 19-1-09Document1 pageEurocode 6 How To Design Masonry Structures 19-1-09Mohamed Omer HassanNo ratings yet

- Model Railroad Plans and DrawingsDocument7 pagesModel Railroad Plans and DrawingsBán ZoltánNo ratings yet

- Mobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 SeriesDocument3 pagesMobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 Series Mobil Pegasus™ 1100 SeriesMudabbir Shan AhmedNo ratings yet

- BQ Mechanical (Sirim)Document7 pagesBQ Mechanical (Sirim)mohd farhan ariff zaitonNo ratings yet

- How The Draganflyer Flies: So How Does It Work?Document5 pagesHow The Draganflyer Flies: So How Does It Work?sav33No ratings yet

- Basicline BL 21t9stDocument28 pagesBasicline BL 21t9stgabriel6276No ratings yet

- 6303A HP Flare Drain DrumDocument16 pages6303A HP Flare Drain DrumMohammad MohseniNo ratings yet

- Enclosed Product Catalogue 2012Document24 pagesEnclosed Product Catalogue 2012Jon BerryNo ratings yet

- Prepositions-Of-place Worksheet Azucena SalasDocument3 pagesPrepositions-Of-place Worksheet Azucena SalasAndreia SimõesNo ratings yet

- Application for Assistant Engineer PostDocument3 pagesApplication for Assistant Engineer PostKandasamy Pandian SNo ratings yet

- Process Thermodynamic Steam Trap PDFDocument9 pagesProcess Thermodynamic Steam Trap PDFhirenkumar patelNo ratings yet

- Strength of A440 Steel Joints Connected With A325 Bolts PublicatDocument52 pagesStrength of A440 Steel Joints Connected With A325 Bolts Publicathal9000_mark1No ratings yet

- Hublit Limphaire Leaflet India PDFDocument2 pagesHublit Limphaire Leaflet India PDFAkshay RaiNo ratings yet