You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chapter 2 - Foundations of Individual BehaviourDocument19 pagesChapter 2 - Foundations of Individual BehaviourSyeda najiaNo ratings yet

- Noman Khan Internship ReportDocument37 pagesNoman Khan Internship ReportnomanNo ratings yet

- L2 - HRM in IndiaDocument11 pagesL2 - HRM in IndiaAbdul Hani MohammedNo ratings yet

- TheShipMastersBusinessCompanion Part CDocument26 pagesTheShipMastersBusinessCompanion Part CMuhammadNo ratings yet

- MTI-International Sponsorship - Updated Guidance For Trusts - April 2018Document3 pagesMTI-International Sponsorship - Updated Guidance For Trusts - April 2018ifeanyiukNo ratings yet

- DT20218615600 ApplicationDocument5 pagesDT20218615600 Applicationsrikanth Muthyala68No ratings yet

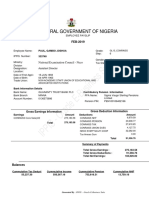

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument18 pagesIPPIS - Oracle E-Business Suite: Federal Government of Nigeriamustapha kamilu100% (1)

- Ch21 - Summary of Leadership Theory PDFDocument38 pagesCh21 - Summary of Leadership Theory PDFPrasetiyadi PrasNo ratings yet

- HRM - Group 7 FinalDocument15 pagesHRM - Group 7 FinalsoumyaNo ratings yet

- Ethical Issues in BusinessDocument20 pagesEthical Issues in BusinessSuraj ChoudharyNo ratings yet

- Technical Communication A Practical Approach 8th Edition Pfeiffer Test BankDocument5 pagesTechnical Communication A Practical Approach 8th Edition Pfeiffer Test BankMatthewBaileypnmig100% (16)

- New York Senate Aging Committee Long-Term Care Workforce Hearing ReportDocument40 pagesNew York Senate Aging Committee Long-Term Care Workforce Hearing ReportState Senator Rachel MayNo ratings yet

- Supply ChainDocument20 pagesSupply ChainRizwan KhanNo ratings yet

- AKAT Company ProfileDocument8 pagesAKAT Company ProfileAnonymous mFPtAEa8100% (1)

- 2021 05 EN Ulkomaalaisena Tyontekijana Suomessa PDFDocument20 pages2021 05 EN Ulkomaalaisena Tyontekijana Suomessa PDFSt JakobNo ratings yet

- SYLLABUS ECONOMICS 105 "History of Economic Thought" Summer 2009Document7 pagesSYLLABUS ECONOMICS 105 "History of Economic Thought" Summer 2009Amy AdamsNo ratings yet

- HRM - Unit 2 - PPT - VJDocument14 pagesHRM - Unit 2 - PPT - VJVijay prasadNo ratings yet

- 1 Prelim Introduction To EconomicsDocument51 pages1 Prelim Introduction To EconomicsLovely Jane MercadoNo ratings yet

- Unit 1 HRM 2021Document70 pagesUnit 1 HRM 2021Shreya ChauhanNo ratings yet

- ppt132 eDocument2 pagesppt132 eLucasNo ratings yet

- Degrowth Vocabulary - Introduction Degrowth - Kallis Demaria Dalisa PDFDocument19 pagesDegrowth Vocabulary - Introduction Degrowth - Kallis Demaria Dalisa PDFrickyigbyNo ratings yet

- ODOC Meet 7 PDFDocument28 pagesODOC Meet 7 PDFDyanNo ratings yet

- Performance Appraisal Practices in Hospitality Industry in New Delhi An Exploratory Study Ijariie1738Document12 pagesPerformance Appraisal Practices in Hospitality Industry in New Delhi An Exploratory Study Ijariie1738AviJainNo ratings yet

- Kumplan Kuiz Mis ChatrinDocument28 pagesKumplan Kuiz Mis ChatrinRizki PurbaNo ratings yet

- Sandu v. Sum Total Systems (Complaint)Document36 pagesSandu v. Sum Total Systems (Complaint)bamlawcaNo ratings yet

- Cost Management: A Strategic EmphasisDocument48 pagesCost Management: A Strategic EmphasisTubagus Donny SyafardanNo ratings yet

- Fisher Happiness at Work ReviewDocument31 pagesFisher Happiness at Work Reviewผศ.ดร.ทวิพันธ์ พัวสรรเสริญNo ratings yet

- 11 Eni Supplier Code of Conduct - ENGDocument16 pages11 Eni Supplier Code of Conduct - ENGSenthil KumarNo ratings yet

- COCP Policy - 2022Document7 pagesCOCP Policy - 2022PrasannaNo ratings yet

- According To L. F. URWICK, " Business Houses AreDocument19 pagesAccording To L. F. URWICK, " Business Houses AreKajal Vikash SinghNo ratings yet