You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Legal Memorandum SampleDocument6 pagesLegal Memorandum SampleMonica Cajucom91% (35)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Executive Protection Travel ChecklistDocument4 pagesExecutive Protection Travel Checklistcpadimitris100% (5)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Subprime Meltdown Case Analysis on US Housing CrisisDocument3 pagesSubprime Meltdown Case Analysis on US Housing Crisiscstellou22No ratings yet

- 01-JUN-2019 - 30-JUN-2019 (1) - UnlockedDocument3 pages01-JUN-2019 - 30-JUN-2019 (1) - UnlockedSwethasri KNo ratings yet

- Basics of Indirect ContemptDocument3 pagesBasics of Indirect ContemptMarie Mariñas-delos ReyesNo ratings yet

- Elements of Indirect ContemptDocument1 pageElements of Indirect ContemptMarie Mariñas-delos ReyesNo ratings yet

- Basics of Indirect ContemptDocument3 pagesBasics of Indirect ContemptMarie Mariñas-delos ReyesNo ratings yet

- 47129rmc No. 45-2009 (Letter of Intent - SAMPLE)Document1 page47129rmc No. 45-2009 (Letter of Intent - SAMPLE)rain06021992No ratings yet

- Conflict of Laws GuideDocument1 pageConflict of Laws GuideMarie Mariñas-delos ReyesNo ratings yet

- R.A. No. 10173 Data Privacy Act of 2012Document9 pagesR.A. No. 10173 Data Privacy Act of 2012Rovan Gionald LimNo ratings yet

- Banking LawsDocument36 pagesBanking LawsMarie Mariñas-delos ReyesNo ratings yet

- Aaafdhjewrggc dhfgjcghhjsaDVJafghcxdasfdghasgDocument1 pageAaafdhjewrggc dhfgjcghhjsaDVJafghcxdasfdghasgMarie Mariñas-delos ReyesNo ratings yet

- Legal FormsDocument77 pagesLegal FormsKatrina Montes98% (65)

- RA 11038 - ENIPAS Protected AreasDocument4 pagesRA 11038 - ENIPAS Protected AreasMarie Mariñas-delos ReyesNo ratings yet

- Quality Manual On Case Management - Revision 0Document15 pagesQuality Manual On Case Management - Revision 0Marie Mariñas-delos ReyesNo ratings yet

- Philippine Theft Case Against Lorenzo MatibagDocument2 pagesPhilippine Theft Case Against Lorenzo MatibagMarie Mariñas-delos Reyes100% (1)

- CRIMINAL LAW QUESTIONS FROM THE 2016 PHILIPPINE BAR EXAMDocument8 pagesCRIMINAL LAW QUESTIONS FROM THE 2016 PHILIPPINE BAR EXAMMarie Mariñas-delos ReyesNo ratings yet

- DAO 1992-29 - IRR of RA6969Document27 pagesDAO 1992-29 - IRR of RA6969Pacific Spectrum100% (1)

- 1 AlbaDocument4 pages1 AlbaMarie Mariñas-delos ReyesNo ratings yet

- August 2017 Civil Law Review Cases - CollatedDocument2 pagesAugust 2017 Civil Law Review Cases - CollatedMarie Mariñas-delos ReyesNo ratings yet

- DOJ Circular No. 70Document3 pagesDOJ Circular No. 70Sharmen Dizon Gallenero100% (1)

- Property CasesDocument105 pagesProperty CasesMarie Mariñas-delos ReyesNo ratings yet

- Enrile Petition Against Plunder Charge DenialDocument12 pagesEnrile Petition Against Plunder Charge DenialMarie Mariñas-delos ReyesNo ratings yet

- DAAN vs. SANDIGANBAYANDocument4 pagesDAAN vs. SANDIGANBAYANMarie Mariñas-delos ReyesNo ratings yet

- Practice Court 1Document3 pagesPractice Court 1Marie Mariñas-delos ReyesNo ratings yet

- Assignment in Labor Law ReviewDocument1 pageAssignment in Labor Law ReviewMarie Mariñas-delos ReyesNo ratings yet

- Wills and Succession Syllabus BreakdownDocument15 pagesWills and Succession Syllabus BreakdownMarie Mariñas-delos ReyesNo ratings yet

- ABC Bank's motion to dismiss on improper venueDocument9 pagesABC Bank's motion to dismiss on improper venueMarie Mariñas-delos ReyesNo ratings yet

- Petition For ReplevinDocument4 pagesPetition For ReplevinMarie Mariñas-delos ReyesNo ratings yet

- Sample Format - Articles of IncorporationDocument8 pagesSample Format - Articles of IncorporationMarie Mariñas-delos ReyesNo ratings yet

- Political Law - Defunis vs. OdegaardDocument29 pagesPolitical Law - Defunis vs. OdegaardMarie Mariñas-delos ReyesNo ratings yet

- Tanada vs. TuveraDocument14 pagesTanada vs. TuveraMarie Mariñas-delos ReyesNo ratings yet

- IBP vs. ZamoraDocument33 pagesIBP vs. ZamoraMarie Mariñas-delos ReyesNo ratings yet

- Forward RatesDocument2 pagesForward RatesTiso Blackstar GroupNo ratings yet

- Simulated Document CheckDocument6 pagesSimulated Document CheckAlok Pathak100% (1)

- CFG Accounting and Finance Considerations PWC Winter 2014Document39 pagesCFG Accounting and Finance Considerations PWC Winter 2014timevalueNo ratings yet

- Medical Services Recruitment Board (MRB) : Government of Tamil Nadu, Chennai - 6. Website: WWW - MRB.TN - Gov.inDocument19 pagesMedical Services Recruitment Board (MRB) : Government of Tamil Nadu, Chennai - 6. Website: WWW - MRB.TN - Gov.inguruyasNo ratings yet

- LBG Sandbox API GuideDocument18 pagesLBG Sandbox API Guidepavithra2No ratings yet

- 201244WAR1Document716 pages201244WAR1Sam MaurerNo ratings yet

- Karthikeyan G - Updated ResumeDocument7 pagesKarthikeyan G - Updated ResumeKarthikeyan GangadharanNo ratings yet

- Financial Development, Financial Inclusion, and Informality: New International EvidenceDocument36 pagesFinancial Development, Financial Inclusion, and Informality: New International EvidencececaNo ratings yet

- Quiz 1 - Intacc 2Document9 pagesQuiz 1 - Intacc 2Eleina SwiftNo ratings yet

- Kolkata MetroDocument39 pagesKolkata MetroArjun PalNo ratings yet

- The Interest Act, 1978 consolidates and amends interest lawsDocument2 pagesThe Interest Act, 1978 consolidates and amends interest lawsvivek1280No ratings yet

- Bank Islam Personal Loan-Repayment-TableDocument4 pagesBank Islam Personal Loan-Repayment-TableKhairi ZainNo ratings yet

- Subject Verb AgreementDocument5 pagesSubject Verb AgreementHarish Yadav100% (1)

- K-Electric SukukDocument16 pagesK-Electric SukukAlaikaNo ratings yet

- Fixed and Floating Exchange RatesDocument22 pagesFixed and Floating Exchange Ratesmeghasingh_09No ratings yet

- Research Journal On Commerce and EconomicsDocument114 pagesResearch Journal On Commerce and EconomicsSkandh NathamNo ratings yet

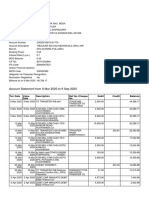

- Bank Statement09-2020Document6 pagesBank Statement09-2020Tnt SolutionsNo ratings yet

- NSDL Project Report PDFDocument72 pagesNSDL Project Report PDFravikumarreddyt100% (3)

- Prospectus BedmuthaIndustriesDocument380 pagesProspectus BedmuthaIndustriesMurali KrishnaNo ratings yet

- Group 2Document26 pagesGroup 2Hyunjin imtreeeNo ratings yet

- "People's Co-Operative Bank, Veraval": "A Study On Analysis of Cash Management"Document55 pages"People's Co-Operative Bank, Veraval": "A Study On Analysis of Cash Management"Dave JimitNo ratings yet

- pdfGenerateNewCustomer SAOAO1020618564Reciept SAOAO1020618564ResidentAccountOpenFormDocument11 pagespdfGenerateNewCustomer SAOAO1020618564Reciept SAOAO1020618564ResidentAccountOpenFormpavan reddyNo ratings yet

- Walter BagehotDocument4 pagesWalter BagehotdantevantesNo ratings yet

- Habib Bank Limited (HBL) : HBL Was The First Commercial Bank To Be Established in Pakistan in 1947Document7 pagesHabib Bank Limited (HBL) : HBL Was The First Commercial Bank To Be Established in Pakistan in 1947Muhammad ShakeelNo ratings yet

- Customer Satisfaction at Western UnionDocument85 pagesCustomer Satisfaction at Western UnionRonak Surana100% (3)

- PGIMER Mortuary Upgradation TenderDocument38 pagesPGIMER Mortuary Upgradation TenderPhotostat CenterNo ratings yet

- Internship Report On Credit Management of MTBLDocument61 pagesInternship Report On Credit Management of MTBLtanvir100% (1)