You might also like

- Key Elements of KYC Policy and Anti-Money Laundering GuidelinesDocument7 pagesKey Elements of KYC Policy and Anti-Money Laundering Guidelinestalrejajyoti73% (11)

- Kyc Aml McqsDocument9 pagesKyc Aml McqspraveenkumarNo ratings yet

- Question Paper On KYCDocument9 pagesQuestion Paper On KYCNaresh JoshiNo ratings yet

- MCQs On KYCDocument7 pagesMCQs On KYCParmila Choudhary50% (2)

- AML& KYC QuestionsDocument93 pagesAML& KYC QuestionsNiranjan ReddyNo ratings yet

- AML-KYC-Sample Questions by MuruganDocument67 pagesAML-KYC-Sample Questions by Muruganpetre86% (56)

- How money laundering risks affect countries and financial institutionsDocument42 pagesHow money laundering risks affect countries and financial institutionsAbidRazaca88% (16)

- AMLQuestionDocument9 pagesAMLQuestionVicky Joshi59% (44)

- What is forgery of a cheque and other key conceptsDocument501 pagesWhat is forgery of a cheque and other key conceptsVikasSharma80% (15)

- AMLDocument26 pagesAMLGowdham M Krishnan100% (1)

- E TestDocument58 pagesE TestShivam Jain100% (4)

- Money laundering stages and detection methodsDocument4 pagesMoney laundering stages and detection methodsSrishtikumawat20% (5)

- ICICI Bank PO Exam 2010 - Computer General Awareness Banking and CareerDocument7 pagesICICI Bank PO Exam 2010 - Computer General Awareness Banking and Careerkapeed_sup29% (7)

- Foundation Course On Anti-Money Laundering - IndiaDocument4 pagesFoundation Course On Anti-Money Laundering - IndiaSeema Patil80% (5)

- Anti Money Laundering (1) Suresh PDFDocument12 pagesAnti Money Laundering (1) Suresh PDFkomal81% (69)

- Anti Money Laundering..... KeyDocument8 pagesAnti Money Laundering..... Keychat2giridharan68% (22)

- Icici Ethics..Document26 pagesIcici Ethics..Rohit P100% (1)

- Answer Key DDocument231 pagesAnswer Key DAbhisek Mukherjee0% (1)

- Information SecurityDocument6 pagesInformation SecurityKarthi Karthik45% (38)

- Code of Business Conduct EthicsDocument32 pagesCode of Business Conduct EthicsVinayak Shetty67% (3)

- Code of Business Conduct Ethics PDFDocument26 pagesCode of Business Conduct Ethics PDFChauhan Chetan67% (3)

- Aml Learning Matrix KeyDocument6 pagesAml Learning Matrix Keyshivakumar59% (17)

- KYC AML VIGILANCE MASTERDocument25 pagesKYC AML VIGILANCE MASTERprashant pradhan100% (3)

- Aml Answer SheetDocument6 pagesAml Answer SheetVasu DevaNo ratings yet

- Mandatory E Learning Pre IBankerDocument3 pagesMandatory E Learning Pre IBankerB. S NityaNo ratings yet

- ANTLMONEY LAUNDERING INNDIADocument12 pagesANTLMONEY LAUNDERING INNDIAanila rathodaNo ratings yet

- Anti Money Laundering (1) Anil PDFDocument12 pagesAnti Money Laundering (1) Anil PDFAnil ponnamaneni PhotographyNo ratings yet

- LC of Group Code of Business Conduct and EthicsDocument6 pagesLC of Group Code of Business Conduct and EthicsPoovizhi.s100% (4)

- Test 1Document12 pagesTest 1digital sevaNo ratings yet

- Icici Group Code of Business Conduct and Ethics 2017Document31 pagesIcici Group Code of Business Conduct and Ethics 2017shreyas patil67% (6)

- Anti Money LaunderingDocument5 pagesAnti Money LaunderingGaurav ChoudharyNo ratings yet

- Aml ManipalDocument8 pagesAml ManipalRavi AnandNo ratings yet

- E Learning AnswersDocument55 pagesE Learning AnswersJyoti Ranjan Roul50% (2)

- LC of Group Code of Business Conduct and EthicsDocument6 pagesLC of Group Code of Business Conduct and EthicsAnuj KumarNo ratings yet

- Information Security Awaremess AnsDocument6 pagesInformation Security Awaremess AnsNikhil Singh72% (189)

- Business Code of ConductDocument5 pagesBusiness Code of ConductPrabhavathi NeelamsettiNo ratings yet

- Think Privacy AnsDocument7 pagesThink Privacy AnsRasmi Ranjan RoutNo ratings yet

- Sexual Harassment at WorkplaceDocument3 pagesSexual Harassment at Workplaceyoyoabcd60% (5)

- Banking Section OverviewDocument2 pagesBanking Section Overviewarpitgupta100% (1)

- Information Security and Risk Management QuizDocument13 pagesInformation Security and Risk Management Quizgintokidmc50% (2)

- Think PrivacyDocument1 pageThink PrivacyRAGHUNATH SHANMUGAMNo ratings yet

- E Learning Answer KeyDocument22 pagesE Learning Answer Keysai raj75% (4)

- CodeDocument15 pagesCodeAnkur Pandey75% (203)

- Think Privacy 2Document7 pagesThink Privacy 2Avijit Parida78% (40)

- Code of Business Conduct EthicsDocument22 pagesCode of Business Conduct Ethicsdrashish_verma75% (4)

- Think Privacy 1 1Document15 pagesThink Privacy 1 1satish82% (77)

- PDF 5Document7 pagesPDF 5Manish SainNo ratings yet

- College student decision making scenariosDocument6 pagesCollege student decision making scenariosAASEEN ALAM0% (1)

- Code of Business Conduct EthicsDocument34 pagesCode of Business Conduct EthicsNeha JaiswalNo ratings yet

- Evaluation I For Skills and Attitude at Workplace: Aread Alcud Draw HighlDocument11 pagesEvaluation I For Skills and Attitude at Workplace: Aread Alcud Draw HighlDIWAKAR KUMAR50% (2)

- Personal Loan Video AnswersDocument4 pagesPersonal Loan Video AnswersSaikrishna DyagalaNo ratings yet

- 9 MCQ On Third Party Products With Ans.Document4 pages9 MCQ On Third Party Products With Ans.Nitin MalikNo ratings yet

- JaiibprinciplesbankingmodulesabquestionsDocument59 pagesJaiibprinciplesbankingmodulesabquestionssanjaykv98100% (1)

- AMLA Multiple Choice QuestionsDocument6 pagesAMLA Multiple Choice QuestionsLeny Joy DupoNo ratings yet

- MargdarshniDocument185 pagesMargdarshniRahul Singh100% (1)

- 1) A Bank Accepts A Deposit From A Corporate House.: B) Mortgage of The TractorDocument17 pages1) A Bank Accepts A Deposit From A Corporate House.: B) Mortgage of The TractoramitatforeNo ratings yet

- Financial Awareness Questions Fro oNgCDocument6 pagesFinancial Awareness Questions Fro oNgCFreudestein UditNo ratings yet

- 1000MCQ With Answer On Accounts & Finance For BankersDocument182 pages1000MCQ With Answer On Accounts & Finance For BankersCITIZEN2No ratings yet

- Jaiib I 50q-PrinciplesDocument33 pagesJaiib I 50q-PrinciplessharmilaNo ratings yet

- JIIB Test PpersDocument51 pagesJIIB Test PpersPriyanka LincolnNo ratings yet

- A Financial Ratio Analysis of Hindustan Unilever Limited (HUL)Document5 pagesA Financial Ratio Analysis of Hindustan Unilever Limited (HUL)Santosh KumarNo ratings yet

- Bosch Performance by Ratio AnalysisDocument34 pagesBosch Performance by Ratio AnalysisSantosh KumarNo ratings yet

- Payment Bank: What They Can and Can't DoDocument3 pagesPayment Bank: What They Can and Can't DoSantosh KumarNo ratings yet

- THE Fortune at The Bottom of The Pyramid: Eradicating Poverty Through ProfitsDocument12 pagesTHE Fortune at The Bottom of The Pyramid: Eradicating Poverty Through ProfitsSantosh KumarNo ratings yet

- Jatayu Season2 Idea-Solution Presentation TemplateDocument15 pagesJatayu Season2 Idea-Solution Presentation TemplateHarika RavitlaNo ratings yet

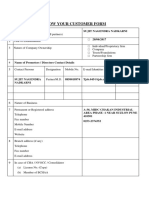

- Know Your Customer FormDocument2 pagesKnow Your Customer FormSushil ShailNo ratings yet

- Know Your CustomerDocument3 pagesKnow Your CustomerMardi RahardjoNo ratings yet

- Ezbob SME Digital Lending Product DescriptionDocument34 pagesEzbob SME Digital Lending Product DescriptionMinhminh NguyenNo ratings yet

- Industrial Development Bank of PakistanDocument12 pagesIndustrial Development Bank of PakistanSyeda Sani100% (1)

- KPMG Cracking Crypto CurrencyDocument24 pagesKPMG Cracking Crypto Currencywedbee1No ratings yet

- Know Your CustomerDocument2 pagesKnow Your CustomerSAMEERNo ratings yet

- Branchless Banking in Pakistan: An Overview of Models and RegulationsDocument11 pagesBranchless Banking in Pakistan: An Overview of Models and RegulationsSyed Ozair RizviNo ratings yet

- PRUlink Withdrawal Form For Corporate PolicyownerDocument2 pagesPRUlink Withdrawal Form For Corporate PolicyownerMarjorie Clarise MendozaNo ratings yet

- Efficient Client Onboarding: The Key To Empowering BanksDocument9 pagesEfficient Client Onboarding: The Key To Empowering BanksCognizantNo ratings yet

- Training Material From Clerk To S 1 2015-16 PROMOTION-STUDY-MATERIAL-2015 For ClericalsDocument298 pagesTraining Material From Clerk To S 1 2015-16 PROMOTION-STUDY-MATERIAL-2015 For Clericalsvikasm4uNo ratings yet

- Financing Small and Medium Enterprise: A Case Study of BASIC Bank LTDDocument20 pagesFinancing Small and Medium Enterprise: A Case Study of BASIC Bank LTDAhsan ali riazNo ratings yet

- Customer Application Form: Personal DetailsDocument19 pagesCustomer Application Form: Personal DetailsAKNo ratings yet

- Iibf - Publication List Sr. No. Examination Medium Name of The Book Edition Published by Price (RS.)Document8 pagesIibf - Publication List Sr. No. Examination Medium Name of The Book Edition Published by Price (RS.)YogeshNo ratings yet

- SGV Anti-Money Laundering (AML) and Counter Terrorist Financing (CTF) Seminar Series For The Year 2020Document4 pagesSGV Anti-Money Laundering (AML) and Counter Terrorist Financing (CTF) Seminar Series For The Year 2020jayrenielNo ratings yet

- Launch a Digital Asset Exchange in 4 StepsDocument7 pagesLaunch a Digital Asset Exchange in 4 Stepsnormand67No ratings yet

- PWCDocument9 pagesPWCKhalid MahmoodNo ratings yet

- Collection of ChequesDocument7 pagesCollection of Cheques28-RPavan raj. BNo ratings yet

- BCG Corporate Treasury Insights 2015Document19 pagesBCG Corporate Treasury Insights 2015thesrajesh7120100% (1)

- HDFC Bk. - RAR 2015Document32 pagesHDFC Bk. - RAR 2015Moneylife FoundationNo ratings yet

- Gohil DharmadeepsinhDocument79 pagesGohil DharmadeepsinhNikhil KapoorNo ratings yet

- AML KYC LowDocument8 pagesAML KYC Lowpremgaur007184No ratings yet

- Financial UnderwritingDocument19 pagesFinancial UnderwritingPritish PatnaikNo ratings yet

- What Is KYCDocument3 pagesWhat Is KYCPrateek LoganiNo ratings yet

- FINTECH in Myanmar PDFDocument4 pagesFINTECH in Myanmar PDFRiza Zausa CuarteroNo ratings yet

- NIB Annual Report 2015Document216 pagesNIB Annual Report 2015Asif RafiNo ratings yet

- Aml& Kyc PDFDocument133 pagesAml& Kyc PDFmayur kulkarniNo ratings yet

- Financial Inclusion in IndiaDocument25 pagesFinancial Inclusion in IndiaMitul RawatNo ratings yet

- Tackling The Menace of Shell Companies in India: A StudyDocument6 pagesTackling The Menace of Shell Companies in India: A StudyArghyaNo ratings yet

- Customer Onboarding and Origination PDFDocument16 pagesCustomer Onboarding and Origination PDFgraycellNo ratings yet