You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Calculating WACC using book value and market value proportionsDocument11 pagesCalculating WACC using book value and market value proportionsanshul dyundiNo ratings yet

- Solved Problem 14.1: The Above Is Obtained Using The Following StepsDocument3 pagesSolved Problem 14.1: The Above Is Obtained Using The Following StepsArjun Jaideep BhatnagarNo ratings yet

- Chapter - 9: Solutions - To - End - of - Chapter - 9 - Problems - On - Estimating - Cost - of - CapitalDocument7 pagesChapter - 9: Solutions - To - End - of - Chapter - 9 - Problems - On - Estimating - Cost - of - CapitalMASPAKNo ratings yet

- Cost of Capital AnalysisDocument5 pagesCost of Capital AnalysisIqbal BaihaqiNo ratings yet

- Financial Management Theory and Practice 2nd Edition Brigham Solutions ManualDocument24 pagesFinancial Management Theory and Practice 2nd Edition Brigham Solutions Manualexsect.drizzlezu100% (16)

- Calculating Cost of CapitalDocument10 pagesCalculating Cost of CapitalMelissaNo ratings yet

- Ch09 Solutions ManualDocument10 pagesCh09 Solutions ManualwangyuNo ratings yet

- Wacc SolutionsDocument8 pagesWacc SolutionssrassmasoodNo ratings yet

- Cost of Capital CalculationsDocument9 pagesCost of Capital CalculationsTalha JavedNo ratings yet

- Kewangan Korporat LatihanDocument4 pagesKewangan Korporat LatihanfahmiyyahNo ratings yet

- Suggested Answer - Syl12 - Dec13 - Paper 14 Final Examination: Suggested Answers To QuestionsDocument18 pagesSuggested Answer - Syl12 - Dec13 - Paper 14 Final Examination: Suggested Answers To QuestionsMudit AgarwalNo ratings yet

- Solutions To End-Of-Chapter ProblemsDocument7 pagesSolutions To End-Of-Chapter ProblemsYaam MedwedNo ratings yet

- Answers To Problem Sets: Risk and The Cost of CapitalDocument7 pagesAnswers To Problem Sets: Risk and The Cost of Capitalpriyanka GayathriNo ratings yet

- Cost ofDocument14 pagesCost ofrajjoNo ratings yet

- Corporate Finance Study Guide Spring 2013 Part 2Document20 pagesCorporate Finance Study Guide Spring 2013 Part 2Ehab M. Abdel HadyNo ratings yet

- Chapter 12 - ET3Document6 pagesChapter 12 - ET3anthony.schzNo ratings yet

- New Microsoft Word DocumentDocument5 pagesNew Microsoft Word Documentjgfjhf arwtrNo ratings yet

- Engineering Economy 8th Edition Blank Solutions ManualDocument38 pagesEngineering Economy 8th Edition Blank Solutions Manualleogreenetxig100% (17)

- Engineering Economy 8th Edition Blank Solutions Manual Full Chapter PDFDocument45 pagesEngineering Economy 8th Edition Blank Solutions Manual Full Chapter PDFaffreightlaurer5isc100% (12)

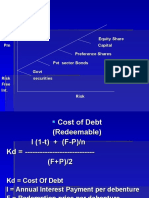

- Risk Equity Share PM Capital Preference Shares PVT Sector Bonds Govt Risk Securities Free Int. RiskDocument12 pagesRisk Equity Share PM Capital Preference Shares PVT Sector Bonds Govt Risk Securities Free Int. RiskrajjoNo ratings yet

- Quiz 3 SolDocument54 pagesQuiz 3 SolBekpasha DursunovNo ratings yet

- Solutions For Credit RiskDocument3 pagesSolutions For Credit RiskTuan Tran VanNo ratings yet

- Long QuestionsDocument18 pagesLong Questionssaqlainra50% (2)

- Chapter 14. The Cost of CapitalDocument15 pagesChapter 14. The Cost of Capitalmy backup1No ratings yet

- Answers To Problem Sets: Risk and The Cost of CapitalDocument7 pagesAnswers To Problem Sets: Risk and The Cost of CapitalSriram BharadwajNo ratings yet

- Cost of Capital Concept and MeasurementDocument37 pagesCost of Capital Concept and MeasurementAkshat SinghNo ratings yet

- Huzaima Jamal-1Document11 pagesHuzaima Jamal-1Fatima ZehraNo ratings yet

- CH19Document8 pagesCH19Lyana Del Arroyo OliveraNo ratings yet

- Spring 1999: Problem 1Document30 pagesSpring 1999: Problem 1ShubhamNo ratings yet

- 5 - Cost of CapitalDocument6 pages5 - Cost of CapitaloryzanoviaNo ratings yet

- Market Capitalization WeightDocument2 pagesMarket Capitalization WeightrishiNo ratings yet

- Solutions To End-Of-Chapter Problems 11Document6 pagesSolutions To End-Of-Chapter Problems 11weeeeeshNo ratings yet

- Calculating WACC and growth rateDocument12 pagesCalculating WACC and growth raterajjoNo ratings yet

- The Cost of Capital: Answers To End-Of-Chapter QuestionsDocument13 pagesThe Cost of Capital: Answers To End-Of-Chapter QuestionsRissa VillarinNo ratings yet

- Solution Maf603 Jun 2019Document11 pagesSolution Maf603 Jun 2019Hadi DahalanNo ratings yet

- 14 Additional Solved Problems 13Document17 pages14 Additional Solved Problems 13PIYUSH CHANDRAVANSHINo ratings yet

- Chapter 11 - Cost of CapitalDocument18 pagesChapter 11 - Cost of CapitalTajrian RahmanNo ratings yet

- Answers To Practice Questions: Capital Budgeting and RiskDocument8 pagesAnswers To Practice Questions: Capital Budgeting and Risksharktale2828No ratings yet

- Ebook Corporate Finance A Focused Approach 5Th Edition Ehrhardt Solutions Manual Full Chapter PDFDocument43 pagesEbook Corporate Finance A Focused Approach 5Th Edition Ehrhardt Solutions Manual Full Chapter PDFquachhaitpit100% (9)

- Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions ManualDocument38 pagesCorporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manualdoraphillipsooeot100% (16)

- Paper14 SolutionDocument25 pagesPaper14 SolutionGregorio VidadNo ratings yet

- Chapter 9. Tool Kit For The Cost of CapitalDocument14 pagesChapter 9. Tool Kit For The Cost of CapitalasimqaiserNo ratings yet

- December 20 FTFM PracticeDocument54 pagesDecember 20 FTFM PracticerajanikanthNo ratings yet

- Solution Manual Cost of Capital: Question 1: Refer To The Book For The Question. Solution 1Document11 pagesSolution Manual Cost of Capital: Question 1: Refer To The Book For The Question. Solution 1subbuNo ratings yet

- 7 Cost of Capital CTDI October 2013Document85 pages7 Cost of Capital CTDI October 2013Diane SerranoNo ratings yet

- ASSIGNMENT 2 - FIN 6000 GROUPS 5 - Attempt - 2022-07-19-20-37-46 - GROUP 5 FIN 6000 - ASSIGNMENT 2Document8 pagesASSIGNMENT 2 - FIN 6000 GROUPS 5 - Attempt - 2022-07-19-20-37-46 - GROUP 5 FIN 6000 - ASSIGNMENT 2Bellindah wNo ratings yet

- Assignment 1 Kelompok 3Document15 pagesAssignment 1 Kelompok 3iyanNo ratings yet

- Chapter 4: Risk Measurement and Hurdle Rates in PracticeDocument10 pagesChapter 4: Risk Measurement and Hurdle Rates in PracticeOsama bin adnanNo ratings yet

- Meseleler 100Document9 pagesMeseleler 100Elgun ElgunNo ratings yet

- The Cost of Capital: Answers To End-Of-Chapter QuestionsDocument21 pagesThe Cost of Capital: Answers To End-Of-Chapter QuestionsMiftahul FirdausNo ratings yet

- Tugas Accounting and Finance Bab 2 Setelah UtsDocument6 pagesTugas Accounting and Finance Bab 2 Setelah UtsbogitugasNo ratings yet

- FM COE FineDocument14 pagesFM COE FineBenzon Agojo OndovillaNo ratings yet

- Cost of Capital Tut. MemoDocument2 pagesCost of Capital Tut. MemoSEKEETHA DE NOBREGANo ratings yet

- Ch09 - Cost of Capital 12112020 125813pmDocument13 pagesCh09 - Cost of Capital 12112020 125813pmMuhammad Umar BashirNo ratings yet

- FIN 202 Homework 4 QuestionsDocument5 pagesFIN 202 Homework 4 QuestionsmosesNo ratings yet

- CFM4 Solns Chap 08Document5 pagesCFM4 Solns Chap 08Sultan AlghamdiNo ratings yet

- Lahore School of Economics Financial Management II The Cost of CapitalDocument3 pagesLahore School of Economics Financial Management II The Cost of CapitalDaniyal AliNo ratings yet

- PL M18 FM Student Mark Plan WebDocument9 pagesPL M18 FM Student Mark Plan WebIQBAL MAHMUDNo ratings yet

- Submit This Assignment Electronically To The Instructor by The Due DateDocument2 pagesSubmit This Assignment Electronically To The Instructor by The Due Datezordan rizvyNo ratings yet

- Project Management Chapter 10 THE COST OF CAPITAL Math SolutionsDocument4 pagesProject Management Chapter 10 THE COST OF CAPITAL Math Solutionszordan rizvyNo ratings yet

- Place Branding of Cox's Bazar - Final Term PaperDocument18 pagesPlace Branding of Cox's Bazar - Final Term Paperzordan rizvy100% (2)

- Babylon Garments Internship Report Brac UniversityDocument43 pagesBabylon Garments Internship Report Brac Universityzordan rizvyNo ratings yet

- Answers To End of Chapter QuestionsDocument4 pagesAnswers To End of Chapter Questionszordan rizvyNo ratings yet

- 3rd Consolidated Statement-2011 Al Arafah Islami BankDocument1 page3rd Consolidated Statement-2011 Al Arafah Islami Bankzordan rizvyNo ratings yet

- Analysis of Option Combination StrategiesDocument10 pagesAnalysis of Option Combination Strategieszordan rizvyNo ratings yet

- Relation of Sociology with other social sciencesDocument4 pagesRelation of Sociology with other social sciencesBheeya BhatiNo ratings yet

- Global GovernanceDocument20 pagesGlobal GovernanceSed LenNo ratings yet

- Concepts of Cavity Prep PDFDocument92 pagesConcepts of Cavity Prep PDFChaithra Shree0% (1)

- Introduction To Mass Communication Solved MCQs (Set-3)Document5 pagesIntroduction To Mass Communication Solved MCQs (Set-3)Abdul karim MagsiNo ratings yet

- Performance Requirements For Organic Coatings Applied To Under Hood and Chassis ComponentsDocument31 pagesPerformance Requirements For Organic Coatings Applied To Under Hood and Chassis ComponentsIBR100% (2)

- It - Unit 14 - Assignment 2 1Document8 pagesIt - Unit 14 - Assignment 2 1api-669143014No ratings yet

- Otis, Elisha Graves REPORTDocument7 pagesOtis, Elisha Graves REPORTrmcclary76No ratings yet

- GST Project ReportDocument29 pagesGST Project ReportHENA KHANNo ratings yet

- Mar 2021Document2 pagesMar 2021TanNo ratings yet

- Fact-Sheet Pupils With Asperger SyndromeDocument4 pagesFact-Sheet Pupils With Asperger SyndromeAnonymous Pj6OdjNo ratings yet

- FeistGorman - 1998-Psychology of Science-Integration of A Nascent Discipline - 2Document45 pagesFeistGorman - 1998-Psychology of Science-Integration of A Nascent Discipline - 2Josué SalvadorNo ratings yet

- Proceedings of The 2012 PNLG Forum: General AssemblyDocument64 pagesProceedings of The 2012 PNLG Forum: General AssemblyPEMSEA (Partnerships in Environmental Management for the Seas of East Asia)No ratings yet

- Initial Data Base (Narrative)Document11 pagesInitial Data Base (Narrative)LEBADISOS KATE PRINCESSNo ratings yet

- Dwnload Full Fundamentals of Human Neuropsychology 7th Edition Kolb Test Bank PDFDocument12 pagesDwnload Full Fundamentals of Human Neuropsychology 7th Edition Kolb Test Bank PDFprindivillemaloriefx100% (12)

- Modern Dental Assisting 11Th Edition Bird Test Bank Full Chapter PDFDocument37 pagesModern Dental Assisting 11Th Edition Bird Test Bank Full Chapter PDFRichardThompsonpcbd100% (9)

- Dalit LiteratureDocument16 pagesDalit LiteratureVeena R NNo ratings yet

- C++ Project On Library Management by KCDocument53 pagesC++ Project On Library Management by KCkeval71% (114)

- 5528 L1 L2 Business Admin Unit Pack v4Document199 pages5528 L1 L2 Business Admin Unit Pack v4Yousef OlabiNo ratings yet

- The Emergence of India's Pharmaceutical IndustryDocument41 pagesThe Emergence of India's Pharmaceutical Industryvivekgupta2jNo ratings yet

- Compatibility Testing: Week 5Document33 pagesCompatibility Testing: Week 5Bridgette100% (1)

- IAS 8 Tutorial Question (SS)Document2 pagesIAS 8 Tutorial Question (SS)Given RefilweNo ratings yet

- GVP College of Engineering (A) 2015Document3 pagesGVP College of Engineering (A) 2015Abhishek SunilNo ratings yet

- Angel Turns 18 Debut ScriptDocument2 pagesAngel Turns 18 Debut ScriptChristian Jorge Lenox100% (1)

- GRADE 8 English Lesson on Indian LiteratureDocument3 pagesGRADE 8 English Lesson on Indian LiteratureErold TarvinaNo ratings yet

- Noise Blinking LED: Circuit Microphone Noise Warning SystemDocument1 pageNoise Blinking LED: Circuit Microphone Noise Warning Systemian jheferNo ratings yet

- Brinker Insider Trading SuitDocument5 pagesBrinker Insider Trading SuitDallasObserverNo ratings yet

- Something About UsDocument18 pagesSomething About UsFercho CarrascoNo ratings yet

- 2006 - Bykovskii - JPP22 (6) Continuous Spin DetonationsDocument13 pages2006 - Bykovskii - JPP22 (6) Continuous Spin DetonationsLiwei zhangNo ratings yet

- W220 Engine Block, Oil Sump and Cylinder Liner DetailsDocument21 pagesW220 Engine Block, Oil Sump and Cylinder Liner DetailssezarNo ratings yet

- Endoplasmic ReticulumDocument4 pagesEndoplasmic Reticulumnikki_fuentes_1100% (1)