You might also like

- Systems of First Order Differential Equations ExplainedDocument16 pagesSystems of First Order Differential Equations ExplainedakshayNo ratings yet

- Systems of First Order Differential Equations: Department of Mathematics IIT GuwahatiDocument18 pagesSystems of First Order Differential Equations: Department of Mathematics IIT GuwahatiAwais Mehmood BhattiNo ratings yet

- Systems of Differential Equations ExplainedDocument10 pagesSystems of Differential Equations ExplainedNand SinghNo ratings yet

- MTH212 (Chap2) l12Document41 pagesMTH212 (Chap2) l12俄狄浦斯No ratings yet

- Economics 600: Department of Economics University of MarylandDocument15 pagesEconomics 600: Department of Economics University of MarylandrokhannnNo ratings yet

- ODEs II CompletoDocument11 pagesODEs II CompletoJosué David Regalado LópezNo ratings yet

- Differential Equations - Ordinary Differential Equations - Systems of First Order Differential Equations and Linear Systems of Differential EquationsDocument6 pagesDifferential Equations - Ordinary Differential Equations - Systems of First Order Differential Equations and Linear Systems of Differential EquationsMaxEconomicsNo ratings yet

- Systems of Linear Equations: 1 Matrix FunctionsDocument12 pagesSystems of Linear Equations: 1 Matrix FunctionsSeow Khaiwen KhaiwenNo ratings yet

- Using ode45 to solve ODEs (40Document4 pagesUsing ode45 to solve ODEs (40Souar KhalilNo ratings yet

- 04-Random ProcessesDocument39 pages04-Random ProcessesGetahun Shanko KefeniNo ratings yet

- T X T X T X: Using Ode45 To Solve Ordinary Differential EquationsDocument4 pagesT X T X T X: Using Ode45 To Solve Ordinary Differential EquationsSouar KhalilNo ratings yet

- Linear Systems: Dr. T. PhaneendraDocument7 pagesLinear Systems: Dr. T. PhaneendraParth VijayNo ratings yet

- Chapter 2Document27 pagesChapter 2Ralph Justine GuintoNo ratings yet

- Rabies ModelDocument12 pagesRabies Modelarajara16No ratings yet

- 9 Spin Stabilization: 9.1 StabilityDocument8 pages9 Spin Stabilization: 9.1 StabilityMBNo ratings yet

- Chapter6Document48 pagesChapter6Cristian LopezNo ratings yet

- Lecture 4Document23 pagesLecture 4kirilNo ratings yet

- Function of Stochastic ProcessDocument58 pagesFunction of Stochastic ProcessbiruckNo ratings yet

- Introduction To Stochastic Processes: Master INVESMAT 2017-2018 Unit 3Document50 pagesIntroduction To Stochastic Processes: Master INVESMAT 2017-2018 Unit 3Ainhoa AzorinNo ratings yet

- Lecture 713 PDFDocument6 pagesLecture 713 PDFtayeNo ratings yet

- Sheet 2Document1 pageSheet 2ahmedmohamedn92No ratings yet

- Convergence of VIM for ODE systemsDocument10 pagesConvergence of VIM for ODE systemsErno ScheiberNo ratings yet

- Signal System AssignmentDocument5 pagesSignal System Assignment21ELB370MOHAMMAD AREEB HASAN KHANNo ratings yet

- Linear ODESDocument12 pagesLinear ODESAdi SubbuNo ratings yet

- Eee 2502 Control Engineering Notes 2015Document55 pagesEee 2502 Control Engineering Notes 2015powertechenteprisesNo ratings yet

- Ls 6Document7 pagesLs 6Razia JanNo ratings yet

- MA 2213 - Tutorial 1Document3 pagesMA 2213 - Tutorial 1Manas AmbatiNo ratings yet

- Boyce W.E., DiPrima R.C. Elementary Differential Equations and Boundary Value Problems 2009-Pages-454-464Document11 pagesBoyce W.E., DiPrima R.C. Elementary Differential Equations and Boundary Value Problems 2009-Pages-454-464Nurul Rafiqah NasutionNo ratings yet

- Special Solutions and Stability AnalysisDocument18 pagesSpecial Solutions and Stability AnalysisDiana OctavianiNo ratings yet

- System of Linear EquationsDocument19 pagesSystem of Linear EquationsAditya SrivatsavNo ratings yet

- Differential Equations - Ordinary Differential Equations - Linear Systems of Differential EquationsDocument4 pagesDifferential Equations - Ordinary Differential Equations - Linear Systems of Differential EquationsMaxEconomicsNo ratings yet

- Chapter III SiteDocument100 pagesChapter III SiteRahul SaxenaNo ratings yet

- Mathematical Methods for Macroeconomics: Solving Differential EquationsDocument20 pagesMathematical Methods for Macroeconomics: Solving Differential EquationsAvijit PuriNo ratings yet

- FALLSEM2019-20 ECE1004 ETH VL2019201003919 Reference Material V 02-Aug-2019 Ref 31Document82 pagesFALLSEM2019-20 ECE1004 ETH VL2019201003919 Reference Material V 02-Aug-2019 Ref 31Haren ShylakNo ratings yet

- 1 A Dash On Moments: Moments, Moment-Generating Functions, and Method-Of-Moments EstimatorsDocument10 pages1 A Dash On Moments: Moments, Moment-Generating Functions, and Method-Of-Moments EstimatorsAbraham desieNo ratings yet

- 17 - Systems of Linear First-Order Differential EquationsDocument17 pages17 - Systems of Linear First-Order Differential EquationsTaye DejeneNo ratings yet

- Lyapunov Indirect Method for Nonautonomous SystemDocument2 pagesLyapunov Indirect Method for Nonautonomous SystemNator17No ratings yet

- Enae 641Document6 pagesEnae 641bob3173No ratings yet

- Quiz III B MA1001Document2 pagesQuiz III B MA1001Wolf shadowNo ratings yet

- Math 20D - Fall 2011 - Final Exam TopicsDocument4 pagesMath 20D - Fall 2011 - Final Exam TopicsFasius TucklerNo ratings yet

- Dr. Igor Zelenko, Fall 2017Document7 pagesDr. Igor Zelenko, Fall 2017ybNo ratings yet

- System of First Order Differential EquationsDocument24 pagesSystem of First Order Differential EquationsKaniel OutisNo ratings yet

- 18AN62 - Control Systems - Unit 5 Lecture Notes Introduction To State Space Analysis (For Private Circulation Only)Document49 pages18AN62 - Control Systems - Unit 5 Lecture Notes Introduction To State Space Analysis (For Private Circulation Only)MD SHAHRIARMAHMUDNo ratings yet

- 340 Week 15 Monday QuizDocument2 pages340 Week 15 Monday QuizSekar PrasetyaNo ratings yet

- Introduction to Random Processes (Part 1Document8 pagesIntroduction to Random Processes (Part 1Brian HughesNo ratings yet

- Runge-Kutta Rao-Mechanical VibrationsDocument4 pagesRunge-Kutta Rao-Mechanical VibrationsSaulo Marcondes de MouraNo ratings yet

- Stat2602b Topic 1Document27 pagesStat2602b Topic 1wingszet24No ratings yet

- ODE Equations ExplainedDocument16 pagesODE Equations ExplainedYanira EspinozaNo ratings yet

- Acta Mathematica Vietnamica 251 Volume 23, Number 3, 2000, Pp. 251-260Document10 pagesActa Mathematica Vietnamica 251 Volume 23, Number 3, 2000, Pp. 251-260Nguyễn Hữu Điển100% (2)

- Signals and Systems Laboratory 5Document11 pagesSignals and Systems Laboratory 5Kthiha CnNo ratings yet

- sns_2021_중간(온라인)Document2 pagessns_2021_중간(온라인)juyeons0204No ratings yet

- Differential Equations: Associate Professor Pham Huu Anh NgocDocument69 pagesDifferential Equations: Associate Professor Pham Huu Anh Ngocde santosNo ratings yet

- O DenotesDocument69 pagesO DenotesMustafa Hikmet Bilgehan UçarNo ratings yet

- Tutorial 2 - Systems (Exercises)Document3 pagesTutorial 2 - Systems (Exercises)LEIDYDANNYTSNo ratings yet

- Lecture 14Document10 pagesLecture 14Cosmin M-escuNo ratings yet

- Lecture 6 - Fall 2023Document38 pagesLecture 6 - Fall 2023tarunya724No ratings yet

- WS 6 For 09 11Document4 pagesWS 6 For 09 11Beth RankinNo ratings yet

- Principles of CommunicationDocument42 pagesPrinciples of CommunicationSachin DoddamaniNo ratings yet

- Tables of Generalized Airy Functions for the Asymptotic Solution of the Differential Equation: Mathematical Tables SeriesFrom EverandTables of Generalized Airy Functions for the Asymptotic Solution of the Differential Equation: Mathematical Tables SeriesNo ratings yet

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)From EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)No ratings yet

- The Fourier transform of sin(ω0t) is:Fsin(ω0t) = πδ(ω - ω0) - δ(ω + ω0)This follows from the fact that sin(ω0t) = (e^{jω0t} - e^{-jω0t})/2j and the Fourier transform property Fe^{jωt} = 2πδ(ω - ω0Document38 pagesThe Fourier transform of sin(ω0t) is:Fsin(ω0t) = πδ(ω - ω0) - δ(ω + ω0)This follows from the fact that sin(ω0t) = (e^{jω0t} - e^{-jω0t})/2j and the Fourier transform property Fe^{jωt} = 2πδ(ω - ω0Chernet TugeNo ratings yet

- Some Immunological Test: Presented by Alaa Faeiz Ashwaaq Dyaa Aseel Abd AL-Razaq Supervised by D.FerasDocument33 pagesSome Immunological Test: Presented by Alaa Faeiz Ashwaaq Dyaa Aseel Abd AL-Razaq Supervised by D.FerasChernet TugeNo ratings yet

- Dms Chap5 Slide 1Document19 pagesDms Chap5 Slide 1Chernet TugeNo ratings yet

- FourierDocument105 pagesFourierChernet TugeNo ratings yet

- Stefani 2Document309 pagesStefani 2Chernet TugeNo ratings yet

- Dms Chap5 Slide 1Document19 pagesDms Chap5 Slide 1Chernet TugeNo ratings yet

- Solution Manual Stefani 4th EdDocument309 pagesSolution Manual Stefani 4th EdFURQAN85% (13)

- LaplaceDocument33 pagesLaplaceravindarsinghNo ratings yet

- Block Diagram Representations of Dynamic Systems (MScDocument74 pagesBlock Diagram Representations of Dynamic Systems (MScChernet TugeNo ratings yet

- DELAYED COURNOT STABILITYDocument20 pagesDELAYED COURNOT STABILITYChernet TugeNo ratings yet

- LaplaceDocument33 pagesLaplaceravindarsinghNo ratings yet

- Chapter 3 Mechanical Systems - Part1 - ForclassDocument39 pagesChapter 3 Mechanical Systems - Part1 - ForclassAlberto darianNo ratings yet

- Nonlinear Differential EquationsDocument8 pagesNonlinear Differential EquationsManali PatilNo ratings yet

- Chap 1part1dmsDocument16 pagesChap 1part1dmsChernet TugeNo ratings yet

- Nonlinear Differential EquationsDocument8 pagesNonlinear Differential EquationsManali PatilNo ratings yet

- 19.1 Complex ExponentsDocument2 pages19.1 Complex ExponentsChernet TugeNo ratings yet

- Notes PhasePlane PDFDocument28 pagesNotes PhasePlane PDFSol NascimentoNo ratings yet

- Introduction To Generalized Functions With Applications in Aerodynamics and AeroacousticsDocument53 pagesIntroduction To Generalized Functions With Applications in Aerodynamics and AeroacousticsSilviu100% (1)

- Introduction To Statistics Lesson 1Document82 pagesIntroduction To Statistics Lesson 1Chernet TugeNo ratings yet

- L Yap Fun C ConstructDocument3 pagesL Yap Fun C ConstructChernet TugeNo ratings yet

- Peer LearningDocument16 pagesPeer LearningChernet Tuge100% (1)

- Mechanics 1Document3 pagesMechanics 1Chernet TugeNo ratings yet

- Study On The Dynamic Model of A Duopoly Game With Delay in PDFDocument10 pagesStudy On The Dynamic Model of A Duopoly Game With Delay in PDFChernet TugeNo ratings yet

- Peer LearningDocument16 pagesPeer LearningChernet Tuge100% (1)

- 25.1 Contour IntegralsDocument4 pages25.1 Contour IntegralsChernet TugeNo ratings yet

- AME-562 Analytic FunctionsDocument3 pagesAME-562 Analytic FunctionsParveen SwamiNo ratings yet

- Stable RegionsmainDocument19 pagesStable RegionsmainChernet TugeNo ratings yet

- Lecture 36Document33 pagesLecture 36Chernet TugeNo ratings yet

- MarkeevDocument17 pagesMarkeevChernet TugeNo ratings yet

- Detailed Lesson Plan in Empowerment TechnologyDocument8 pagesDetailed Lesson Plan in Empowerment TechnologyNelson Tapales100% (1)

- Criminal Investigation (LEA) Use CaseDocument2 pagesCriminal Investigation (LEA) Use CaseDewa AsmaraNo ratings yet

- Hawassa University IOT RUP Software ProcessDocument17 pagesHawassa University IOT RUP Software ProcessZobahaa HorunkuNo ratings yet

- Unit 1: 1.1 Microprocessors and MicrocontrollersDocument13 pagesUnit 1: 1.1 Microprocessors and Microcontrollerssachin tupeNo ratings yet

- MC-2 SERIES OPERATION MANUALDocument21 pagesMC-2 SERIES OPERATION MANUALsergio paulo chavesNo ratings yet

- Statistics with R — A practical guide for beginnersDocument101 pagesStatistics with R — A practical guide for beginnersPedro PereiraNo ratings yet

- Integrating Computational Chemistry (Molecular Modeling) Into The General Chemistry CurriculumDocument12 pagesIntegrating Computational Chemistry (Molecular Modeling) Into The General Chemistry CurriculumDevi Vianisa UliviaNo ratings yet

- STS WiFi (MAR2011v2)Document27 pagesSTS WiFi (MAR2011v2)Hoang NguyenNo ratings yet

- Trader Dale'S Vwap Quick GuideDocument8 pagesTrader Dale'S Vwap Quick GuideRui LopesNo ratings yet

- Section 1Document35 pagesSection 1Bhargav HathiNo ratings yet

- ChatDocument5 pagesChatJOKER GAMINGNo ratings yet

- Computer Science Textbook Solutions - 24Document30 pagesComputer Science Textbook Solutions - 24acc-expertNo ratings yet

- ManualDocument24 pagesManualAnonymous 2I6zroTNo ratings yet

- DBMS Practical File DBMS Practical FileDocument39 pagesDBMS Practical File DBMS Practical FileNisarga NaikNo ratings yet

- Y Dale A Tu Hogar Una Nueva Vida: CF: 12000-Mcco03h CF: 12000-Mcco03h TF: 12000-Do - 001Document165 pagesY Dale A Tu Hogar Una Nueva Vida: CF: 12000-Mcco03h CF: 12000-Mcco03h TF: 12000-Do - 001jezreelNo ratings yet

- Genetic Programming: A Seminar OnDocument23 pagesGenetic Programming: A Seminar OnZatin GuptaNo ratings yet

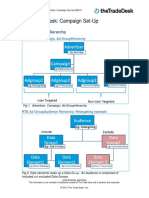

- The Trade DeskDocument13 pagesThe Trade DeskAmpLiveNo ratings yet

- Jiayin Li 1pageresumeDocument1 pageJiayin Li 1pageresumeapi-356910091No ratings yet

- 4 Semester Syllabus BTECH - CSE - 13.03Document61 pages4 Semester Syllabus BTECH - CSE - 13.03Chandan productionNo ratings yet

- Velocio Builder: Velocio Networks Vbuilder Logic ProgrammingDocument265 pagesVelocio Builder: Velocio Networks Vbuilder Logic ProgrammingalinupNo ratings yet

- Project Management Assignment - 01: Pranav Dosjah 2016DA01004Document15 pagesProject Management Assignment - 01: Pranav Dosjah 2016DA01004Savita Wadhawan100% (1)

- Tracer Overview BrochureDocument8 pagesTracer Overview BrochureWoodrow FoxNo ratings yet

- ESXTOP Vsphere6 PDFDocument1 pageESXTOP Vsphere6 PDFSuman RagiNo ratings yet

- Cyber Forensics Principles: Jayaram P CdacDocument54 pagesCyber Forensics Principles: Jayaram P CdacMartin HumphreyNo ratings yet

- File Transfer Protocol (FTP) : Mcgraw-Hill ©the Mcgraw-Hill Companies, Inc., 2000Document25 pagesFile Transfer Protocol (FTP) : Mcgraw-Hill ©the Mcgraw-Hill Companies, Inc., 2000GauravgNo ratings yet

- CCC AntisurgeDocument2 pagesCCC AntisurgeDamian Wahlig100% (1)

- Es Model ExamDocument3 pagesEs Model ExamAarun ArasanNo ratings yet

- Figure 4-35. Modelsim Altera Starter Edition: Hello World!Document5 pagesFigure 4-35. Modelsim Altera Starter Edition: Hello World!ali alilouNo ratings yet

- Chapter 7 pdf-1Document27 pagesChapter 7 pdf-1Tora SarkarNo ratings yet