You might also like

- An Introduction to Forex Trading: A Guide for BeginnersFrom EverandAn Introduction to Forex Trading: A Guide for BeginnersRating: 4 out of 5 stars4/5 (6)

- Chapter 10 - Measuring Exposure To Exchange Rate FluctuationsDocument30 pagesChapter 10 - Measuring Exposure To Exchange Rate FluctuationsJeffrey StrachanNo ratings yet

- Foreign Exchange Risk 2Document3 pagesForeign Exchange Risk 2Raima DollNo ratings yet

- Chase Bank Statement 1 LatestDocument3 pagesChase Bank Statement 1 LatestRoe Computer50% (2)

- Assignment of Banking LawDocument24 pagesAssignment of Banking LawTOON TEMPLENo ratings yet

- Financial Management Assignment: Prepared By, Rahul Pareek IMI, New DelhiDocument72 pagesFinancial Management Assignment: Prepared By, Rahul Pareek IMI, New Delhipareek2020100% (1)

- Foreign Exchange Risk & Exposure: Kameshwar RaoDocument22 pagesForeign Exchange Risk & Exposure: Kameshwar RaoHarish HunterNo ratings yet

- Foreign ExchangeDocument12 pagesForeign ExchangeMadhurGuptaNo ratings yet

- Exchange Rate Exposure and HedgingDocument17 pagesExchange Rate Exposure and HedgingRavihara D.G.KNo ratings yet

- Expo RiskDocument21 pagesExpo RiskNaresh VemisettiNo ratings yet

- Assignment 2Document16 pagesAssignment 2Aaqib NawazNo ratings yet

- Foreign Exchange Risk ManagementDocument17 pagesForeign Exchange Risk ManagementPraseem KulshresthaNo ratings yet

- Foreign Exchange RiskDocument18 pagesForeign Exchange RiskAyush GaurNo ratings yet

- International Finance - Module VDocument38 pagesInternational Finance - Module VVishnu VishnuNo ratings yet

- IFM Question AnsDocument19 pagesIFM Question Anssunil routNo ratings yet

- Chapter 2 Different Types of Foreign Exchange Transactions and Associated RisksDocument24 pagesChapter 2 Different Types of Foreign Exchange Transactions and Associated RisksAmlan BoraNo ratings yet

- FSD14Document2 pagesFSD14Leo the BulldogNo ratings yet

- Unit-5 Managing Foreign Exchange ExposureDocument3 pagesUnit-5 Managing Foreign Exchange ExposureLeo the BulldogNo ratings yet

- Foreign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ADocument3 pagesForeign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ASonali RawatNo ratings yet

- Foreign Exchange Rate ExposureDocument3 pagesForeign Exchange Rate Exposuretulasinad123No ratings yet

- Foreign Exchange Risk ManagementDocument5 pagesForeign Exchange Risk Managementpriya JNo ratings yet

- Rolls Royce and Aston MartinDocument8 pagesRolls Royce and Aston MartinVero NgatiaNo ratings yet

- Types of Foreign ExchangeDocument6 pagesTypes of Foreign ExchangeBasavarajNo ratings yet

- MA0042Document11 pagesMA0042Mrinal KalitaNo ratings yet

- Foreign Exchange Risk: Class NotesDocument2 pagesForeign Exchange Risk: Class Notesgoyal_divya18No ratings yet

- Hjjjjif-2risk & Exposure Lec 13-14Document74 pagesHjjjjif-2risk & Exposure Lec 13-14PriyahemaniNo ratings yet

- Harshika 1Document32 pagesHarshika 1Neha SharmaNo ratings yet

- Final FX Risk & Exposure ManagementDocument33 pagesFinal FX Risk & Exposure ManagementkarunaksNo ratings yet

- International Finance 20012 PDFDocument10 pagesInternational Finance 20012 PDFKishan GoudNo ratings yet

- Foreign Exchange RiskDocument7 pagesForeign Exchange RiskDeepika WilsonNo ratings yet

- Unit 3 Foreign Exchange Risk LimitDocument16 pagesUnit 3 Foreign Exchange Risk Limitaryait099No ratings yet

- UFXBank Forex EbookDocument25 pagesUFXBank Forex EbookMohammed IliyashNo ratings yet

- Economic ExposureDocument7 pagesEconomic ExposureChi NguyenNo ratings yet

- The Best Instrument Against Currency Risk.Document13 pagesThe Best Instrument Against Currency Risk.Hanane KoyakoNo ratings yet

- Currency Translation RiskDocument2 pagesCurrency Translation RiskRubab KanwalNo ratings yet

- Exposure Management in Foreign ExchangeDocument10 pagesExposure Management in Foreign ExchangeGoutami Lakshetti - 11No ratings yet

- Foreign Exchange Risk Management - International Financial Environment, International Business - EduRev NotesDocument8 pagesForeign Exchange Risk Management - International Financial Environment, International Business - EduRev Notesswatisin93No ratings yet

- Econometrics ProjectDocument16 pagesEconometrics ProjectDinesh SharmaNo ratings yet

- Quiz - 3Document6 pagesQuiz - 3anon_652192649100% (1)

- Measuring Exposure To Exchange Rate FluctuationsDocument35 pagesMeasuring Exposure To Exchange Rate FluctuationsarifNo ratings yet

- AssignmetDocument4 pagesAssignmetHumza SarwarNo ratings yet

- Foreign Exchange IssuesDocument9 pagesForeign Exchange IssuesPopoola KehindeNo ratings yet

- Currency RiskDocument65 pagesCurrency RiskBilal AhmadNo ratings yet

- 1 Forex Hedge Accounting TreatmentDocument37 pages1 Forex Hedge Accounting TreatmentPuneet_behki100% (1)

- Foreign Currency RiskDocument13 pagesForeign Currency Riskkenedy simwingaNo ratings yet

- Foreign Exchange Risk: Types of ExposureDocument2 pagesForeign Exchange Risk: Types of ExposurepilotNo ratings yet

- Trading Forex With TradeStation PDFDocument45 pagesTrading Forex With TradeStation PDFelisaNo ratings yet

- International Business 3Document13 pagesInternational Business 3Rahul DewakarNo ratings yet

- Module 7 MANAGEMENT OF FOREIGN OPERATIONS AND INTERNATIONAL TRADE PDFDocument7 pagesModule 7 MANAGEMENT OF FOREIGN OPERATIONS AND INTERNATIONAL TRADE PDFRica SolanoNo ratings yet

- Subject: International Financial Management: An Assignment On TopicDocument24 pagesSubject: International Financial Management: An Assignment On TopicSejal SinghNo ratings yet

- Final ForexDocument28 pagesFinal Forexravinmehta1990No ratings yet

- Foreign Exchange Risk ManagementDocument65 pagesForeign Exchange Risk ManagementBhanu Pratap Singh Bisht100% (2)

- IFM Home AssignmentDocument6 pagesIFM Home AssignmentAnshita GargNo ratings yet

- MS 509 - IFM - Foreign Exchange Risk Exposure - GSKDocument6 pagesMS 509 - IFM - Foreign Exchange Risk Exposure - GSKShaaz AdnanNo ratings yet

- Foundations of Multinational Financial Management 6th Edition Shapiro Solutions ManualDocument30 pagesFoundations of Multinational Financial Management 6th Edition Shapiro Solutions Manualfinificcodille6d3h100% (20)

- Nature of Exchange Rate Risk & ExposureDocument67 pagesNature of Exchange Rate Risk & ExposureDebNo ratings yet

- Unit 4 NotesDocument16 pagesUnit 4 NotesDeva BeharaNo ratings yet

- Exchange Risk MNGTDocument28 pagesExchange Risk MNGTHassaniNo ratings yet

- A Project Report ON Advanced Issues in International Business FORDocument14 pagesA Project Report ON Advanced Issues in International Business FORrohanNo ratings yet

- ConclusionDocument9 pagesConclusionDhawal DamaniNo ratings yet

- CW ReportDocument6 pagesCW ReportZainab SarfrazNo ratings yet

- Foreign ExchangeDocument15 pagesForeign ExchangeAnuranjanSinha100% (1)

- 2019 Eir Special Report Co2 Redux Is MurderDocument64 pages2019 Eir Special Report Co2 Redux Is MurderMcCrenNo ratings yet

- Accounting CaDocument9 pagesAccounting CatejaswiNo ratings yet

- Chernigov Complete Guide With Secrets From Monasteries Past and Minerals - EgDocument474 pagesChernigov Complete Guide With Secrets From Monasteries Past and Minerals - EgO TΣΑΡΟΣ ΤΗΣ ΑΝΤΙΒΑΡΥΤΗΤΑΣ ΛΙΑΠΗΣ ΠΑΝΑΓΙΩΤΗΣNo ratings yet

- Multiple Choice QuestionsDocument6 pagesMultiple Choice QuestionsCandy DollNo ratings yet

- Comparison Report On HIL, Everest and Visaka IndustriesDocument4 pagesComparison Report On HIL, Everest and Visaka IndustriesHItesh priyhianiNo ratings yet

- #17 Dividends and Stock RightsDocument4 pages#17 Dividends and Stock RightsZaaavnn VannnnnNo ratings yet

- Power of Attorney RevocationDocument2 pagesPower of Attorney RevocationRoberto Monterrosa100% (2)

- Financial SectFinancial Sector Reforms in Nepal - What Works What Does Notor Reforms in Nepal - What Works What Does NotDocument40 pagesFinancial SectFinancial Sector Reforms in Nepal - What Works What Does Notor Reforms in Nepal - What Works What Does NotSanjeev AcharyaNo ratings yet

- Clarification Regarding Special Offer - FAQDocument3 pagesClarification Regarding Special Offer - FAQShekhar PrasadNo ratings yet

- Invoice IXITRS185875952789718Document1 pageInvoice IXITRS185875952789718PatriotNo ratings yet

- AudithaccDocument3 pagesAudithaccTk KimNo ratings yet

- Dissolution of PartnershipDocument17 pagesDissolution of PartnershipJASKARANNo ratings yet

- Period End ChecklistDocument4 pagesPeriod End Checklistsneel.bw3636No ratings yet

- HDFC Bank Ltd. HDFC Bank Ltd. HDFC Bank LTD.: Fee Receipt Fee Receipt Fee ReceiptDocument1 pageHDFC Bank Ltd. HDFC Bank Ltd. HDFC Bank LTD.: Fee Receipt Fee Receipt Fee ReceiptaNo ratings yet

- Securitization Act of 2004Document6 pagesSecuritization Act of 2004Talina BinondoNo ratings yet

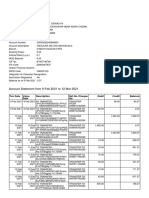

- Account Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceABHINAV DEWALIYANo ratings yet

- Universiti Teknologi Mara Final Assessment: Instructions To CandidatesDocument6 pagesUniversiti Teknologi Mara Final Assessment: Instructions To CandidatesINTAN NOOR AMIRA ROSDINo ratings yet

- Overview of ValuationDocument16 pagesOverview of ValuationFrimpong Gabriel100% (1)

- M-PESA ChargesDocument3 pagesM-PESA ChargesGIDEONNo ratings yet

- Chapter 14Document40 pagesChapter 14Zoe LamNo ratings yet

- Assign-01 (Math341) Fall 2016-17Document4 pagesAssign-01 (Math341) Fall 2016-17Rida Shah0% (1)

- Computational ProblemsDocument272 pagesComputational ProblemslalalalaNo ratings yet

- FWD Funds Daily 06 10 2019Document2 pagesFWD Funds Daily 06 10 2019Donita Asuncion100% (1)

- ICMApdfDocument6 pagesICMApdfToni MartinezNo ratings yet

- I LRD 3 L HF 78 W9 NBDWDocument3 pagesI LRD 3 L HF 78 W9 NBDWBIKRAM KUMAR BEHERANo ratings yet

- Exim Bank of IndiaDocument49 pagesExim Bank of IndiaShruti Vikram0% (1)

- Purchase Price Agreens in Private M&ADocument20 pagesPurchase Price Agreens in Private M&AMeghalsi TarekNo ratings yet