You might also like

- TDS Rates Chart Fy 2020 21 Ay 2021 22Document6 pagesTDS Rates Chart Fy 2020 21 Ay 2021 22Brijendra SinghNo ratings yet

- Financial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Document2 pagesFinancial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Mahesh Shinde100% (1)

- TDS Rate Chart For Financial Year 2020 21Document1 pageTDS Rate Chart For Financial Year 2020 21Arun RajaNo ratings yet

- List of Benefits Available To Salaried PersonsDocument46 pagesList of Benefits Available To Salaried PersonsSaR aSNo ratings yet

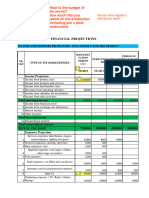

- Proiectie Financiara Saroa-Tradusa Copie (1) 2-1Document7 pagesProiectie Financiara Saroa-Tradusa Copie (1) 2-1p6nnqdnsttNo ratings yet

- Preview Copy Do Not File: Profit or Loss From BusinessDocument1 pagePreview Copy Do Not File: Profit or Loss From BusinessRon KnightNo ratings yet

- Robinhood Markets Inc 85 Willow Road Menlo Park, CA 94025 650-940-2700Document10 pagesRobinhood Markets Inc 85 Willow Road Menlo Park, CA 94025 650-940-2700maicolo1No ratings yet

- Proiectie Financiara Saroa-Tradusa Copie (1) 2Document7 pagesProiectie Financiara Saroa-Tradusa Copie (1) 2p6nnqdnsttNo ratings yet

- National Income and Its AggregatesDocument2 pagesNational Income and Its AggregatesAditya GuptaNo ratings yet

- T.D.S./Tcs Tax Challan: Tax Deducted/Collected at Source From (0020) COMPANY (0021) NON-COMPANY Deductees DeducteesDocument2 pagesT.D.S./Tcs Tax Challan: Tax Deducted/Collected at Source From (0020) COMPANY (0021) NON-COMPANY Deductees DeducteesSURABHI PATRANo ratings yet

- CURRENT ISSUES IN ACCOUNTING Final Exam Dec 22Document14 pagesCURRENT ISSUES IN ACCOUNTING Final Exam Dec 22Fungai MajuriraNo ratings yet

- Form 1621032023 201318 PDFDocument3 pagesForm 1621032023 201318 PDFManvendraNo ratings yet

- Profit or Loss From Business: Edwin Der 353-46-3457 PhotographerDocument2 pagesProfit or Loss From Business: Edwin Der 353-46-3457 PhotographerJames100% (1)

- List of Useful Codes With Descriptions To Be Used As Reference Status of TaxpayerDocument5 pagesList of Useful Codes With Descriptions To Be Used As Reference Status of TaxpayerJayNo ratings yet

- Form PDF 875130970240819Document6 pagesForm PDF 875130970240819Mahendra LakkavaramNo ratings yet

- ITR-2 AY 2010-11 UpdatedDocument24 pagesITR-2 AY 2010-11 Updatedmujeeb1985No ratings yet

- Cma-Krishnaveni Upvc Profiles PDFDocument22 pagesCma-Krishnaveni Upvc Profiles PDFtechnopreneurvizagNo ratings yet

- 12 Additional Solved Problems 11Document17 pages12 Additional Solved Problems 11jjayakumar_vj100% (1)

- Revised TDS Wef 14.05.20Document7 pagesRevised TDS Wef 14.05.20MANAN KOTHARINo ratings yet

- Homework 2Document3 pagesHomework 2gracie sNo ratings yet

- Profit Or: Loss From BusinessDocument2 pagesProfit Or: Loss From BusinessBryan Pasqueci100% (2)

- Schedule C Form With AnnexDocument4 pagesSchedule C Form With Annexgirma1299No ratings yet

- Robinhood Markets Inc 85 Willow Road Menlo Park, CA 94025 650-940-2700Document30 pagesRobinhood Markets Inc 85 Willow Road Menlo Park, CA 94025 650-940-2700bob LastNo ratings yet

- Tax Deduction at SourceDocument13 pagesTax Deduction at SourceSwati SumanNo ratings yet

- Information and Initial Excise Tax Return For Black Lung Benefit Trusts and Certain Related PersonsDocument3 pagesInformation and Initial Excise Tax Return For Black Lung Benefit Trusts and Certain Related PersonsIRSNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 754167410271120 Assessment Year: 2020-21Document8 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 754167410271120 Assessment Year: 2020-21Manish MishraNo ratings yet

- TDS ChartDocument4 pagesTDS ChartjaoceelectricalNo ratings yet

- Reduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Document6 pagesReduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Kranthi Kumar KatamreddyNo ratings yet

- Final CMADocument6 pagesFinal CMAManjari AgrawalNo ratings yet

- Tax Card 2017Document26 pagesTax Card 2017Mohsin EhsanNo ratings yet

- Tax Deposit-Challan 281-Excel FormatDocument5 pagesTax Deposit-Challan 281-Excel FormatpreetNo ratings yet

- TDS - and - TCS Rate Chart 2025Document5 pagesTDS - and - TCS Rate Chart 2025jsparakhNo ratings yet

- Business Income Tax DeclarationDocument2 pagesBusiness Income Tax Declarationmagarsa hirphaNo ratings yet

- Finalized Schedule EDocument2 pagesFinalized Schedule EMira HuNo ratings yet

- US Internal Revenue Service: f8844 - 1994Document3 pagesUS Internal Revenue Service: f8844 - 1994IRSNo ratings yet

- Milkiy FF 2011Document263 pagesMilkiy FF 2011Asfawosen Dingama100% (1)

- Important: Please See Notes Overleaf Before Filling UpDocument3 pagesImportant: Please See Notes Overleaf Before Filling UpgalorebayNo ratings yet

- Equantance RollDocument6 pagesEquantance RollNEERAJ KUMARNo ratings yet

- T.D.S./Tcs Tax ChallanDocument3 pagesT.D.S./Tcs Tax ChallanRukmani GuptaNo ratings yet

- Tax Deducted at SourceDocument3 pagesTax Deducted at SourceShivam SharmaNo ratings yet

- MIC-12 Controller Interfacing Card Traffic Light: Salicon Nano Technology Pvt. LTDDocument22 pagesMIC-12 Controller Interfacing Card Traffic Light: Salicon Nano Technology Pvt. LTDkanchankonwarNo ratings yet

- BIT INFO NEPAL - Economics - ECO155-2079Document2 pagesBIT INFO NEPAL - Economics - ECO155-2079meropriyaaNo ratings yet

- Shail End RaDocument24 pagesShail End Rabharat khandelwalNo ratings yet

- Hkcee Economics - 4.5 Short Run and Long Run - P.1Document4 pagesHkcee Economics - 4.5 Short Run and Long Run - P.1peter wongNo ratings yet

- Class Work AnshikaDocument2 pagesClass Work AnshikaRupanshi AnandNo ratings yet

- FinanceDocument7 pagesFinanceِAli IsmailNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- TDS - and - TCS Rate Chart 2024Document5 pagesTDS - and - TCS Rate Chart 2024Taxation KTPL (Kalyani Techpark Taxation)No ratings yet

- Assessment of Working Capital Requirements Form Ii-Operating StatementDocument9 pagesAssessment of Working Capital Requirements Form Ii-Operating Statementdeshrajji75% (4)

- TDS and TCS-rate-chart-2023 RemovedDocument4 pagesTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65No ratings yet

- TDS and TCS Rate Chart 2023Document5 pagesTDS and TCS Rate Chart 2023DEEPAK SHARMANo ratings yet

- Exhibit 1 Comparative Information On The Seven Largest Polypropylene Plants in EuropeDocument10 pagesExhibit 1 Comparative Information On The Seven Largest Polypropylene Plants in EuropeFadlan AfandiNo ratings yet

- Test 3 Tax SolutionsDocument17 pagesTest 3 Tax SolutionsManjulaNo ratings yet

- Assignment Sheet PGDM, SIBMDocument3 pagesAssignment Sheet PGDM, SIBMDovena CareNo ratings yet

- 02 - Assignment Integration Exercise - SolutionDocument4 pages02 - Assignment Integration Exercise - SolutionAgustín RosalesNo ratings yet

- Shivam Hsse A3Document5 pagesShivam Hsse A3Officially RoastingNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 992002830030121 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 992002830030121 Assessment Year: 2020-21Shweta ShirsatNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Connector Industry: A Profile of the European Connector Industry - Market Prospects to 1999From EverandConnector Industry: A Profile of the European Connector Industry - Market Prospects to 1999No ratings yet

- Shipping WeightDocument17 pagesShipping Weightmoinahmed99No ratings yet

- Supply Chain Create ValueDocument31 pagesSupply Chain Create Valuemoinahmed99No ratings yet

- Budget Brief 2008 (WEB)Document75 pagesBudget Brief 2008 (WEB)moinahmed99No ratings yet

- 04-Behavioral Factors InfluencingDocument12 pages04-Behavioral Factors Influencingmoinahmed99No ratings yet

- Project Milestones - Simplicable PDFDocument13 pagesProject Milestones - Simplicable PDFmoinahmed99No ratings yet

- Airaf Umair Moin Akbar Ijlal: Presenting byDocument21 pagesAiraf Umair Moin Akbar Ijlal: Presenting bymoinahmed99No ratings yet

- External Stakeholders - SimplicableDocument11 pagesExternal Stakeholders - Simplicablemoinahmed99No ratings yet

- Project Description With Reasons of Failure: Gulshan Campus - IIDocument2 pagesProject Description With Reasons of Failure: Gulshan Campus - IImoinahmed99No ratings yet

- Internal Stakeholders - SimplicableDocument16 pagesInternal Stakeholders - Simplicablemoinahmed99No ratings yet

- Event Planning Business Plan ExampleDocument22 pagesEvent Planning Business Plan Examplemoinahmed990% (1)

- Spice Maker Mccormick & Co. Builds A World-Class Supply ChainDocument4 pagesSpice Maker Mccormick & Co. Builds A World-Class Supply Chainmoinahmed99No ratings yet

- Investor'S Briefing: October 15, 2019 Avari Hotel KarachiDocument23 pagesInvestor'S Briefing: October 15, 2019 Avari Hotel Karachimoinahmed99No ratings yet

- Chapter 2 WACCDocument32 pagesChapter 2 WACCmoinahmed99No ratings yet

- Development of Packaging Facility (A Project) : Gulshan Campus - IIDocument5 pagesDevelopment of Packaging Facility (A Project) : Gulshan Campus - IImoinahmed99No ratings yet

- Airaf - Uzair Hamza - Taimoor Hasan - Moin: Mr. Osama Bashir SoomroDocument10 pagesAiraf - Uzair Hamza - Taimoor Hasan - Moin: Mr. Osama Bashir Soomromoinahmed99No ratings yet

- Surge Arrester - 385360 - IP - BC - TT - 60-100-350Document2 pagesSurge Arrester - 385360 - IP - BC - TT - 60-100-350moinahmed99No ratings yet

- IQDocument16 pagesIQmoinahmed99No ratings yet

- SRO 1160 of 2015 - Amendment in NBFC Notified Entities Regulations 2008Document70 pagesSRO 1160 of 2015 - Amendment in NBFC Notified Entities Regulations 2008moinahmed99No ratings yet

- Faysal Bank Double SpreadDocument118 pagesFaysal Bank Double Spreadmoinahmed99No ratings yet

- CPIS GuidelinesDocument6 pagesCPIS Guidelinesmoinahmed99No ratings yet

- 40 Ahadeeth-Arabic OnlyDocument4 pages40 Ahadeeth-Arabic Onlymoinahmed99No ratings yet

- Persian Phonetic KeyboardDocument2 pagesPersian Phonetic Keyboardmoinahmed99No ratings yet

- Lease Accounting IAS17Document10 pagesLease Accounting IAS17moinahmed99No ratings yet

- 1916 South American Championship Squads - WikipediaDocument6 pages1916 South American Championship Squads - WikipediaCristian VillamayorNo ratings yet

- Lesson Plan For Implementing NETSDocument5 pagesLesson Plan For Implementing NETSLisa PizzutoNo ratings yet

- Axera D06Document2 pagesAxera D06Cristián Fernando Cristóbal RoblesNo ratings yet

- Beyond "The Arc of Freedom and Prosperity": Debating Universal Values in Japanese Grand StrategyDocument9 pagesBeyond "The Arc of Freedom and Prosperity": Debating Universal Values in Japanese Grand StrategyGerman Marshall Fund of the United StatesNo ratings yet

- General Chemistry 2 Q1 Lesson 5 Endothermic and Exotheric Reaction and Heating and Cooling CurveDocument19 pagesGeneral Chemistry 2 Q1 Lesson 5 Endothermic and Exotheric Reaction and Heating and Cooling CurveJolo Allexice R. PinedaNo ratings yet

- Expression of Interest (Consultancy) (BDC)Document4 pagesExpression of Interest (Consultancy) (BDC)Brave zizNo ratings yet

- COURTESY Reception Good MannersDocument1 pageCOURTESY Reception Good MannersGulzina ZhumashevaNo ratings yet

- Water Pump 250 Hrs Service No Unit: Date: HM: ShiftDocument8 pagesWater Pump 250 Hrs Service No Unit: Date: HM: ShiftTLK ChannelNo ratings yet

- BackgroundsDocument13 pagesBackgroundsRaMinah100% (8)

- Mosharaf HossainDocument2 pagesMosharaf HossainRuhul RajNo ratings yet

- Comparison of PubMed, Scopus, Web of Science, and Google Scholar - Strengths and WeaknessesDocument5 pagesComparison of PubMed, Scopus, Web of Science, and Google Scholar - Strengths and WeaknessesMostafa AbdelrahmanNo ratings yet

- Binge Eating Disorder ANNADocument12 pagesBinge Eating Disorder ANNAloloasbNo ratings yet

- CS8CHP EletricalDocument52 pagesCS8CHP EletricalCristian ricardo russoNo ratings yet

- 1.water, Acids, Bases, Buffer Solutions in BiochemistryDocument53 pages1.water, Acids, Bases, Buffer Solutions in BiochemistryÇağlaNo ratings yet

- BLP#1 - Assessment of Community Initiative (3 Files Merged)Document10 pagesBLP#1 - Assessment of Community Initiative (3 Files Merged)John Gladhimer CanlasNo ratings yet

- Ritesh Agarwal: Presented By: Bhavik Patel (Iu1981810008) ABHISHEK SHARMA (IU1981810001) VISHAL RATHI (IU1981810064)Document19 pagesRitesh Agarwal: Presented By: Bhavik Patel (Iu1981810008) ABHISHEK SHARMA (IU1981810001) VISHAL RATHI (IU1981810064)Abhi SharmaNo ratings yet

- Network Fundamentas ITEC90Document5 pagesNetwork Fundamentas ITEC90Psychopomp PomppompNo ratings yet

- GE 7 ReportDocument31 pagesGE 7 ReportMark Anthony FergusonNo ratings yet

- T5 B11 Victor Manuel Lopez-Flores FDR - FBI 302s Re VA ID Cards For Hanjour and Almihdhar 195Document11 pagesT5 B11 Victor Manuel Lopez-Flores FDR - FBI 302s Re VA ID Cards For Hanjour and Almihdhar 1959/11 Document Archive100% (2)

- Artificial Intelligence Techniques For Encrypt Images Based On The Chaotic System Implemented On Field-Programmable Gate ArrayDocument10 pagesArtificial Intelligence Techniques For Encrypt Images Based On The Chaotic System Implemented On Field-Programmable Gate ArrayIAES IJAINo ratings yet

- ENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesDocument8 pagesENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesAbu Ammar Al-hakimNo ratings yet

- 3 Diversion&CareDocument2 pages3 Diversion&CareRyan EncomiendaNo ratings yet

- Upes School of Law Lac & Adr Association: PresentsDocument7 pagesUpes School of Law Lac & Adr Association: PresentsSuvedhya ReddyNo ratings yet

- Instructions For Preparing Manuscript For Ulunnuha (2019 Template Version) Title (English and Arabic Version)Document4 pagesInstructions For Preparing Manuscript For Ulunnuha (2019 Template Version) Title (English and Arabic Version)Lailatur RahmiNo ratings yet

- Who Trs 993 Web FinalDocument284 pagesWho Trs 993 Web FinalAnonymous 6OPLC9UNo ratings yet

- EAC Inquiry SDCDocument9 pagesEAC Inquiry SDCThe Sustainable Development Commission (UK, 2000-2011)No ratings yet

- PP Master Data Version 002Document34 pagesPP Master Data Version 002pranitNo ratings yet

- 1 Bacterial DeseaseDocument108 pages1 Bacterial DeseasechachaNo ratings yet

- Roxas City For Revision Research 7 Q1 MELC 23 Week2Document10 pagesRoxas City For Revision Research 7 Q1 MELC 23 Week2Rachele DolleteNo ratings yet

- IcarosDesktop ManualDocument151 pagesIcarosDesktop ManualAsztal TavoliNo ratings yet