You might also like

- Carpenters Vacation Fund 2007Document8 pagesCarpenters Vacation Fund 2007Latisha WalkerNo ratings yet

- Union Security Trust Fund 2007Document10 pagesUnion Security Trust Fund 2007Latisha WalkerNo ratings yet

- Carpenters Welfare Fund 2007Document18 pagesCarpenters Welfare Fund 2007Latisha WalkerNo ratings yet

- Carpenters Vacation Fund 2006Document14 pagesCarpenters Vacation Fund 2006Latisha WalkerNo ratings yet

- Carpenters Welfare Fund 2006Document16 pagesCarpenters Welfare Fund 2006Latisha WalkerNo ratings yet

- Retirement & Pension Plan For NYCDCC Employees 2007Document13 pagesRetirement & Pension Plan For NYCDCC Employees 2007Latisha WalkerNo ratings yet

- Union Security Trust Fund 2006Document10 pagesUnion Security Trust Fund 2006Latisha WalkerNo ratings yet

- Retirement Plan of Trustees 2007Document14 pagesRetirement Plan of Trustees 2007Latisha WalkerNo ratings yet

- Carpenters Annuity Fund 2007Document19 pagesCarpenters Annuity Fund 2007Latisha WalkerNo ratings yet

- Retirement Plan of Trustees 2006Document13 pagesRetirement Plan of Trustees 2006Latisha WalkerNo ratings yet

- 2007 Form 5500 Carpenter Pension PlanDocument21 pages2007 Form 5500 Carpenter Pension PlanLatisha WalkerNo ratings yet

- Retirement & Pension Plan For NYCDCC Employees 2006Document13 pagesRetirement & Pension Plan For NYCDCC Employees 2006Latisha WalkerNo ratings yet

- Carpenters Annuity Fund 2006Document20 pagesCarpenters Annuity Fund 2006Latisha WalkerNo ratings yet

- 5305A-SEP: Salary Reduction Simplified Employee Pension - Individual Retirement Accounts Contribution AgreementDocument8 pages5305A-SEP: Salary Reduction Simplified Employee Pension - Individual Retirement Accounts Contribution AgreementIRSNo ratings yet

- 2006 Form 5500 Carpenter Pension PlanDocument22 pages2006 Form 5500 Carpenter Pension PlanLatisha WalkerNo ratings yet

- Scheme Member'S Request For Fund Transfer Form (for self-employed person, personal account holder or employee ceasing employment) 計 劃 成 員 資 金 轉 移 申 請 表Document4 pagesScheme Member'S Request For Fund Transfer Form (for self-employed person, personal account holder or employee ceasing employment) 計 劃 成 員 資 金 轉 移 申 請 表olimNo ratings yet

- Notice of Situation or Change of Situation or Discontinuation of Situation, of Place Where Foreign Register Shall Be KeptDocument8 pagesNotice of Situation or Change of Situation or Discontinuation of Situation, of Place Where Foreign Register Shall Be KeptNavneetNo ratings yet

- Help Kit D.P.T-3Document9 pagesHelp Kit D.P.T-3Harmeet SinghNo ratings yet

- Form MGT-7A HelpDocument17 pagesForm MGT-7A HelpDNo ratings yet

- F 5304 SimDocument6 pagesF 5304 SimIRSNo ratings yet

- US Internal Revenue Service: I4720 - 1996Document8 pagesUS Internal Revenue Service: I4720 - 1996IRSNo ratings yet

- F 5305 SepDocument2 pagesF 5305 SepIRSNo ratings yet

- Instruction Kit For Eform Dpt-3Document12 pagesInstruction Kit For Eform Dpt-3NavneetNo ratings yet

- US Internal Revenue Service: I8390 - 1996Document2 pagesUS Internal Revenue Service: I8390 - 1996IRSNo ratings yet

- US Internal Revenue Service: I3468 - 1996Document3 pagesUS Internal Revenue Service: I3468 - 1996IRSNo ratings yet

- US Internal Revenue Service: I5500sp - 2003Document1 pageUS Internal Revenue Service: I5500sp - 2003IRSNo ratings yet

- DD 0879Document2 pagesDD 0879Ahmed IbrahimNo ratings yet

- MGT-14 Filing InstructionsDocument14 pagesMGT-14 Filing InstructionsPrathap ChowdaryNo ratings yet

- General OperationalDocument32 pagesGeneral OperationalSANJAY AGARWALNo ratings yet

- Notes To Transfer of Benefits by Scheme Member (For Self-Employed Person, Personal Account Holder or Employee Ceasing Employment)Document7 pagesNotes To Transfer of Benefits by Scheme Member (For Self-Employed Person, Personal Account Holder or Employee Ceasing Employment)LouisNo ratings yet

- Instruction Kit EForm IEPF-5Document9 pagesInstruction Kit EForm IEPF-5Anisha bhalaNo ratings yet

- Instruction Kit For Eform Msc-3: Page 1 of 8Document8 pagesInstruction Kit For Eform Msc-3: Page 1 of 8LokiNo ratings yet

- US Internal Revenue Service: I5500sp - 2004Document1 pageUS Internal Revenue Service: I5500sp - 2004IRSNo ratings yet

- Instructions For Form 1066: U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnDocument6 pagesInstructions For Form 1066: U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnIRSNo ratings yet

- Form No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Document2 pagesForm No. 3ae: Audit Report Under Section 35D (4) /35E (6) of The Income-Tax Act, 1961Anonymous 2evaoXKKdNo ratings yet

- US Internal Revenue Service: f5500 - 1995Document6 pagesUS Internal Revenue Service: f5500 - 1995IRSNo ratings yet

- Application by Company To ROC For Removing Its Name From Register of CompaniesDocument9 pagesApplication by Company To ROC For Removing Its Name From Register of CompaniesDNo ratings yet

- Notification Form For Substantial Shareholder (S) / Unitholder (S) in Respect of Interests in SecuritiesDocument15 pagesNotification Form For Substantial Shareholder (S) / Unitholder (S) in Respect of Interests in SecuritiestestNo ratings yet

- eForm CHG-4 Filing InstructionsDocument9 pageseForm CHG-4 Filing InstructionsDushyant SinghNo ratings yet

- FCGPR Guidance NoteDocument3 pagesFCGPR Guidance NoteBijay KumarNo ratings yet

- US Internal Revenue Service: I5500sb - 2004Document9 pagesUS Internal Revenue Service: I5500sb - 2004IRSNo ratings yet

- Certification of Intent To Adopt A Pre-Approved Plan: MM DD YyyyDocument2 pagesCertification of Intent To Adopt A Pre-Approved Plan: MM DD YyyyIRSNo ratings yet

- Instructions For Form 5500: Annual Return/Report of Employee Benefit Plan (With 100 or More Participants)Document21 pagesInstructions For Form 5500: Annual Return/Report of Employee Benefit Plan (With 100 or More Participants)IRSNo ratings yet

- Kansai Nerolac Software TDSDocument17 pagesKansai Nerolac Software TDSkumargaurav21281No ratings yet

- Payment Services Regulations 2019Document48 pagesPayment Services Regulations 2019asdNo ratings yet

- 2.VSP-67 - Addendum-1Document13 pages2.VSP-67 - Addendum-1Hitesh KoolwalNo ratings yet

- Instruction - Kit - Eform MGT-15Document8 pagesInstruction - Kit - Eform MGT-15NavneetNo ratings yet

- Instruction Kit For Eform Adt - 2: Page 1 of 8Document8 pagesInstruction Kit For Eform Adt - 2: Page 1 of 8maddy14350No ratings yet

- Opening of Bank Account and Shops and Establishment Registration Number)Document12 pagesOpening of Bank Account and Shops and Establishment Registration Number)yashNo ratings yet

- Securities and Exchange Commission (SEC) - Forms-8Document10 pagesSecurities and Exchange Commission (SEC) - Forms-8highfinanceNo ratings yet

- Intimation of Director Identification Number by The Company To The RegistrarDocument10 pagesIntimation of Director Identification Number by The Company To The RegistrarantopradeepNo ratings yet

- Regd. With A.D. C-11 Survey/Blockno.89, Near Rto, Sutagatti Road, Navanagar, Hubballi-580025 (Karnataka)Document2 pagesRegd. With A.D. C-11 Survey/Blockno.89, Near Rto, Sutagatti Road, Navanagar, Hubballi-580025 (Karnataka)AshtadeepakNo ratings yet

- Tendernotice 1Document7 pagesTendernotice 1Monish MNo ratings yet

- Inland Revenue Board of Malaysia: Date of Publication: 19 November 2019Document35 pagesInland Revenue Board of Malaysia: Date of Publication: 19 November 2019Ah SangNo ratings yet

- Esic CertificateDocument2 pagesEsic Certificateayush.guptaNo ratings yet

- US Internal Revenue Service: f5500 - 1996Document6 pagesUS Internal Revenue Service: f5500 - 1996IRSNo ratings yet

- CENTERPOINT ENERGY INC 8-K (Events or Changes Between Quarterly Reports) 2009-02-24Document15 pagesCENTERPOINT ENERGY INC 8-K (Events or Changes Between Quarterly Reports) 2009-02-24http://secwatch.comNo ratings yet

- Aem Holding Sla Aamplc Asial 280918 Form 3 FinalDocument11 pagesAem Holding Sla Aamplc Asial 280918 Form 3 FinalNic LeeNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Annual Income Statement Report Name: Laporan Laba Rugi / Nama / Ery Abd Nasir PelupessyDocument2 pagesAnnual Income Statement Report Name: Laporan Laba Rugi / Nama / Ery Abd Nasir PelupessyErry Abdul Nasir PelupessyNo ratings yet

- Aircraft Budgeting TemplateDocument5 pagesAircraft Budgeting TemplateFaisal ZeinNo ratings yet

- Harsh Mini ProjectDocument178 pagesHarsh Mini ProjectHarsh Kumar100% (1)

- 00 r5kl1 g2 CPBJ 2022.stpDocument4,747 pages00 r5kl1 g2 CPBJ 2022.stp1573183290No ratings yet

- M-2 Boq - Rakesh RDocument16 pagesM-2 Boq - Rakesh RNidhi MehtaNo ratings yet

- Principles of Macroeconomics 6th Edition Frank Test Bank 1Document36 pagesPrinciples of Macroeconomics 6th Edition Frank Test Bank 1cynthiasheltondegsypokmj100% (24)

- WAT Topics EGDocument19 pagesWAT Topics EGnikiNo ratings yet

- 1.630 ATP 2023-24 GR 9 EMS FinalDocument4 pages1.630 ATP 2023-24 GR 9 EMS FinalNeliNo ratings yet

- The Composable Commerce Cheat Sheet: How To Sell The Commerce Solution of Your Dreams To Your Business PeersDocument4 pagesThe Composable Commerce Cheat Sheet: How To Sell The Commerce Solution of Your Dreams To Your Business PeersSaurabh PantNo ratings yet

- Quotation Element 09012023 Jose 145Document3 pagesQuotation Element 09012023 Jose 145Element ConstructionsNo ratings yet

- Wel-Come TODocument201 pagesWel-Come TOgirma guddeNo ratings yet

- Chinese ForeignRelations Power Policy SinceCWDocument447 pagesChinese ForeignRelations Power Policy SinceCWThanh ThảoNo ratings yet

- Business Administration: Passed By: Castillo, Carmela Passed To: Sir Marjeric BuenafeDocument6 pagesBusiness Administration: Passed By: Castillo, Carmela Passed To: Sir Marjeric BuenafeCarmela CastilloNo ratings yet

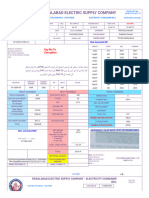

- FESCO July BILLDocument2 pagesFESCO July BILLacademic.kashifNo ratings yet

- Psychology of Trading: Controlling Emotions is KeyDocument4 pagesPsychology of Trading: Controlling Emotions is KeyjoseluisvazquezNo ratings yet

- Managing: Jonathan Liebenau MG 305 LSE, 20 OCT 2020Document36 pagesManaging: Jonathan Liebenau MG 305 LSE, 20 OCT 2020Prakash SinghNo ratings yet

- Strategic Marketing 1st Edition Mooradian Test BankDocument9 pagesStrategic Marketing 1st Edition Mooradian Test Bankmeganfloresyfwemzsrdp100% (15)

- HISTORIC BOND PRICE LISTDocument4 pagesHISTORIC BOND PRICE LISTGustavo RedondoNo ratings yet

- Fraudulent TransferDocument3 pagesFraudulent TransferSeenu SeenuNo ratings yet

- InvoiceDocument1 pageInvoiceKumudini RanaNo ratings yet

- Cambridge TheoryDocument11 pagesCambridge Theoryced apeNo ratings yet

- Franklin Fan Company Case StudyDocument6 pagesFranklin Fan Company Case StudyImani ImaniNo ratings yet

- Documemt - UCO BankDocument68 pagesDocumemt - UCO BankRahul Kumar VishwakarmaNo ratings yet

- Tahi - HatiDocument53 pagesTahi - HatiZhanra Therese Arnaiz100% (1)

- Transport Policies and Development: Policy Research Working Paper 7366Document45 pagesTransport Policies and Development: Policy Research Working Paper 7366Sudhir GotaNo ratings yet

- Operations Management 11th Edition Stevenson Solutions ManualDocument32 pagesOperations Management 11th Edition Stevenson Solutions Manualeiranguyenrd8t100% (23)

- Module 3 - The Marketing EnvironmentDocument34 pagesModule 3 - The Marketing EnvironmentBùi Thị Thu HồngNo ratings yet

- DSInnovate Startup Report 2021Document93 pagesDSInnovate Startup Report 2021Erde ClinicNo ratings yet

- 新世界集团 广州东塔周大福金融中心k11艺术购物中心招商手册 201401 p44Document44 pages新世界集团 广州东塔周大福金融中心k11艺术购物中心招商手册 201401 p44Tazza ChenNo ratings yet

- Comfort Class Transport: Submitted To: Prof. Aravind Panicker Submitted By: Team MobileatyDocument10 pagesComfort Class Transport: Submitted To: Prof. Aravind Panicker Submitted By: Team MobileatyYash Umang ShahNo ratings yet