You might also like

- 14-8-2018 Nikhil Mehta &sons (HUF) & Ors vs. Ms. AMR Infrastuctures LTD - 2Document2 pages14-8-2018 Nikhil Mehta &sons (HUF) & Ors vs. Ms. AMR Infrastuctures LTD - 2Abhijit TripathiNo ratings yet

- Barrons - January 1 2024Document50 pagesBarrons - January 1 2024Abhijit TripathiNo ratings yet

- Hindu Law 1966Document62 pagesHindu Law 1966GANESH MANJHINo ratings yet

- 125 CR - PC Citations, Judgements PDFDocument56 pages125 CR - PC Citations, Judgements PDFAbhijit Tripathi100% (1)

- Code of Civil Procedure by Justice B S ChauhanDocument142 pagesCode of Civil Procedure by Justice B S Chauhannahar_sv1366100% (1)

- Handbook of Frauds Scams and Swindles PDFDocument414 pagesHandbook of Frauds Scams and Swindles PDFswathivishnuNo ratings yet

- Complaint Against The Borrower MDocument3 pagesComplaint Against The Borrower MAbhijit TripathiNo ratings yet

- Notes On Criminal LawDocument5 pagesNotes On Criminal LawAbhijit TripathiNo ratings yet

- 4 Notices Legal MetrologyDocument4 pages4 Notices Legal MetrologyAbhijit TripathiNo ratings yet

- Application For MaintenanceDocument12 pagesApplication For MaintenanceAbhijit TripathiNo ratings yet

- Justice SystemDocument8 pagesJustice SystemAbhijit TripathiNo ratings yet

- M Vijaya PradaDocument3 pagesM Vijaya PradaAbhijit TripathiNo ratings yet

- Constitution PDFDocument69 pagesConstitution PDFharshad nickNo ratings yet

- Form MGT-9 2016Document6 pagesForm MGT-9 2016Abhijit TripathiNo ratings yet

- FAQ For CustomersDocument1 pageFAQ For CustomersAbhijit TripathiNo ratings yet

- Synopsis of Writ PetitionDocument5 pagesSynopsis of Writ PetitionAbhijit TripathiNo ratings yet

- (Established by The State Legislature Act XII of 1956) ("A" Grade, NAAC Accredited)Document1 page(Established by The State Legislature Act XII of 1956) ("A" Grade, NAAC Accredited)Abhijit TripathiNo ratings yet

- Priyadarshini Spinning Mills Ltd-Winding Up NoticeDocument3 pagesPriyadarshini Spinning Mills Ltd-Winding Up NoticeAbhijit TripathiNo ratings yet

- BalasahebDocument2 pagesBalasahebAbhijit TripathiNo ratings yet

- +status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedDocument2 pages+status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedAbhijit TripathiNo ratings yet

- Your Reference STCON ERROR DATED - / - /2015Document1 pageYour Reference STCON ERROR DATED - / - /2015Abhijit TripathiNo ratings yet

- Priyadarshini Spinning Mills Ltd-Winding Up NoticeDocument3 pagesPriyadarshini Spinning Mills Ltd-Winding Up NoticeAbhijit TripathiNo ratings yet

- FAQ For CustomersDocument1 pageFAQ For CustomersAbhijit TripathiNo ratings yet

- Analysis BriberyDocument14 pagesAnalysis BriberyPang Siew ChuNo ratings yet

- Your Reference STCON ERROR DATED - / - /2015Document1 pageYour Reference STCON ERROR DATED - / - /2015Abhijit TripathiNo ratings yet

- Art Dealers - The Other Vincent Van Gogh June 2010 PDFDocument11 pagesArt Dealers - The Other Vincent Van Gogh June 2010 PDFAbhijit TripathiNo ratings yet

- Arun Jaitley Vs Arvind Kejriwal On 12 December, 2017Document5 pagesArun Jaitley Vs Arvind Kejriwal On 12 December, 2017Abhijit TripathiNo ratings yet

- Motor Vehicle Claims Thesis With JudgementsDocument28 pagesMotor Vehicle Claims Thesis With JudgementsAbhijit TripathiNo ratings yet

- How To Write Great EssaysDocument127 pagesHow To Write Great Essaysa100% (25)

- 12 - Chapter 5Document51 pages12 - Chapter 5Shubham GithalaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Overview of Stock Transfer Process in SAP WMDocument11 pagesOverview of Stock Transfer Process in SAP WMMiguel TalaricoNo ratings yet

- Yujuico vs. Far East Bank and Trust Company DigestDocument4 pagesYujuico vs. Far East Bank and Trust Company DigestEmir MendozaNo ratings yet

- Agency TheoryDocument2 pagesAgency TheoryAmeh SundayNo ratings yet

- Od-2017 Ed.1.7Document28 pagesOd-2017 Ed.1.7Tung Nguyen AnhNo ratings yet

- PARCOR-SIMILARITIESDocument2 pagesPARCOR-SIMILARITIESHoney Lizette SunthornNo ratings yet

- Tax Invoice: U64204GJ2008PTC054111 24AADCG1959N1ZA 9984 GJDocument1 pageTax Invoice: U64204GJ2008PTC054111 24AADCG1959N1ZA 9984 GJMrugesh Joshi50% (2)

- Credit Card ConfigurationDocument5 pagesCredit Card ConfigurationdaeyongNo ratings yet

- New ISO 29990 2010 As Value Added To Non-Formal Education Organization in The FutureDocument13 pagesNew ISO 29990 2010 As Value Added To Non-Formal Education Organization in The Futuremohamed lashinNo ratings yet

- Corrección Miro - Zrepmir7Document19 pagesCorrección Miro - Zrepmir7miguelruzNo ratings yet

- SAP ResumeDocument4 pagesSAP ResumesriabcNo ratings yet

- International Marketing Research (DR - Meenakshi SharmaDocument21 pagesInternational Marketing Research (DR - Meenakshi Sharmashweta shuklaNo ratings yet

- Aplicatie Practica Catapulta TUVDocument26 pagesAplicatie Practica Catapulta TUVwalaNo ratings yet

- 703 07s 05 SCMDocument12 pages703 07s 05 SCMDiana Leonita FajriNo ratings yet

- A Case Study QuestionsDocument2 pagesA Case Study QuestionsMarrion MostarNo ratings yet

- Notes On b2b BusinessDocument7 pagesNotes On b2b Businesssneha pathakNo ratings yet

- Investor PDFDocument3 pagesInvestor PDFHAFEZ ALINo ratings yet

- Risk Chapter 6Document27 pagesRisk Chapter 6Wonde BiruNo ratings yet

- Resolution No 003 2020 LoanDocument4 pagesResolution No 003 2020 LoanDexter Bernardo Calanoga TignoNo ratings yet

- President Uhuru Kenyatta's Madaraka Day SpeechDocument8 pagesPresident Uhuru Kenyatta's Madaraka Day SpeechState House Kenya100% (1)

- Capstone Project Final Report - PatanjaliDocument60 pagesCapstone Project Final Report - PatanjaliSharvarish Nandanwar0% (1)

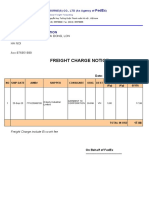

- Freight Charge Notice: To: Garment 10 CorporationDocument4 pagesFreight Charge Notice: To: Garment 10 CorporationThuy HoangNo ratings yet

- History Nestle Pakistan LTDDocument20 pagesHistory Nestle Pakistan LTDMuhammad Khurram Waheed RajaNo ratings yet

- How To Use Oracle Account Generator For Project Related TransactionsDocument40 pagesHow To Use Oracle Account Generator For Project Related Transactionsapnambiar88No ratings yet

- Intermediate Accounting 14th Edition Kieso Test BankDocument25 pagesIntermediate Accounting 14th Edition Kieso Test BankReginaGallagherjkrb100% (58)

- G2 Group5 FMCG Products Fair & Lovely - Ver1.1Document20 pagesG2 Group5 FMCG Products Fair & Lovely - Ver1.1intesharmemonNo ratings yet

- English 8 - Q3 - Las 1 RTP PDFDocument4 pagesEnglish 8 - Q3 - Las 1 RTP PDFKim Elyssa SalamatNo ratings yet

- Guide To Importing in ZimbabweDocument22 pagesGuide To Importing in ZimbabweMandla DubeNo ratings yet

- Section 114-118Document8 pagesSection 114-118ReiZen UelmanNo ratings yet

- Case Study 1Document6 pagesCase Study 1Narendra VaidyaNo ratings yet