You might also like

- Moral Hazard TotalDocument29 pagesMoral Hazard TotalSHREYA SAHNo ratings yet

- Chapter 17Document15 pagesChapter 17Raphael CorbiNo ratings yet

- Prin AgDocument11 pagesPrin AgLukasz HorzelaNo ratings yet

- Micro W4 CDocument4 pagesMicro W4 CJulia LopezNo ratings yet

- Bonds With Warrants and Convertible Bonds (Gor and Cha)Document4 pagesBonds With Warrants and Convertible Bonds (Gor and Cha)Eleina Bea BernardoNo ratings yet

- Solutions To Session 6 Practice ProblemsDocument3 pagesSolutions To Session 6 Practice ProblemsKeshav soodNo ratings yet

- Concepts of Value and ReturnDocument38 pagesConcepts of Value and Returnravi anandNo ratings yet

- Sappington 1991 Incentives in Principal Agent RelationshipDocument23 pagesSappington 1991 Incentives in Principal Agent Relationshipsurna lastriNo ratings yet

- Uncertainty, Risk Aversion and Multiple TasksDocument29 pagesUncertainty, Risk Aversion and Multiple TasksRaphael CorbiNo ratings yet

- 2 Fixed or Variable Pay?Document7 pages2 Fixed or Variable Pay?Satish Kumar SatishNo ratings yet

- Dynamic Contracts: 1 Risk SharingDocument30 pagesDynamic Contracts: 1 Risk SharingZehua WuNo ratings yet

- CA Inter FM-ECO Chapter 6 Key ConceptsDocument23 pagesCA Inter FM-ECO Chapter 6 Key ConceptsAejaz MohamedNo ratings yet

- Lecture 8 PP SolutionsDocument3 pagesLecture 8 PP SolutionsAashiNo ratings yet

- Topic 9 - Incentive System - 2023 - For StudentsDocument42 pagesTopic 9 - Incentive System - 2023 - For StudentsNguyet Vy Dao NguyenNo ratings yet

- Calculating Cost of Capital for Various SourcesDocument6 pagesCalculating Cost of Capital for Various SourcessachinrdkhNo ratings yet

- 10 tips for negotiating your salary like a proDocument1 page10 tips for negotiating your salary like a provenkat_09No ratings yet

- CH 14Document13 pagesCH 14leisurelarry999100% (1)

- Midterm ECON 3110 SPRING 22Document2 pagesMidterm ECON 3110 SPRING 22Ali ZaidiNo ratings yet

- Salanie Principal Agent 2Document10 pagesSalanie Principal Agent 2example3335273No ratings yet

- Concepts of Value and ReturnDocument38 pagesConcepts of Value and ReturnSahil Aggarwal100% (1)

- 2013 Chapter 09Document35 pages2013 Chapter 09Rohyana Nur IsnaenyNo ratings yet

- Chapter 10Document31 pagesChapter 10FebNo ratings yet

- Time Value of Money and Return CalculationsDocument38 pagesTime Value of Money and Return Calculationskhushi vaswaniNo ratings yet

- Moral HazardDocument17 pagesMoral HazardhishamsaukNo ratings yet

- CH - 02 - Time Value of MoneyDocument38 pagesCH - 02 - Time Value of MoneyAlwin SebastianNo ratings yet

- ProfitDocument17 pagesProfitSharandeep KaurNo ratings yet

- Chapte R: Value and ReturnDocument38 pagesChapte R: Value and Returnkhushi vaswaniNo ratings yet

- Econ of Info - Principal-Agent FrameworkDocument32 pagesEcon of Info - Principal-Agent FrameworkPriya R ChourasiaNo ratings yet

- Sample Exam II PDFDocument2 pagesSample Exam II PDFArsen DuisenbayNo ratings yet

- Promotions As IncentivesDocument13 pagesPromotions As IncentivesyizzyNo ratings yet

- Contracting, Governance and Organizational Form: Moral HazardDocument29 pagesContracting, Governance and Organizational Form: Moral HazardMaribeth LubaoNo ratings yet

- Week 011-Module Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 001Document7 pagesWeek 011-Module Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 001Jieann BalicocoNo ratings yet

- CH 02 RevisedDocument38 pagesCH 02 RevisedZia AhmadNo ratings yet

- Extra CM1A April 2021Document4 pagesExtra CM1A April 2021devanshmehta220No ratings yet

- JshdkjahsdDocument188 pagesJshdkjahsdBea Czarina NavarroNo ratings yet

- Methods and Types of Wage Payment SystemsDocument26 pagesMethods and Types of Wage Payment SystemsNarendra RawatNo ratings yet

- Williamson TheoryDocument8 pagesWilliamson TheorysaraNo ratings yet

- Cost of ProductionDocument8 pagesCost of ProductionPhương Thảo NguyễnNo ratings yet

- Lecture 05Document15 pagesLecture 05Menard MendozaNo ratings yet

- Machine Learning For NLPDocument58 pagesMachine Learning For NLPvothaianh18081997No ratings yet

- Stock Investing Mastermind - Zebra Learn-111Document2 pagesStock Investing Mastermind - Zebra Learn-111RGNitinDevaNo ratings yet

- FINANCIAL ECONOMICS NPVDocument29 pagesFINANCIAL ECONOMICS NPVQuyen Thanh NguyenNo ratings yet

- Delegation, Monitoring, and Relational Contracts: Susanne Goldlücke and Sebastian Kranz April 24, 2012Document8 pagesDelegation, Monitoring, and Relational Contracts: Susanne Goldlücke and Sebastian Kranz April 24, 2012José Miguel CarrascoNo ratings yet

- Chapter-01 (Pay Model) )Document35 pagesChapter-01 (Pay Model) )Rahat KhanNo ratings yet

- Roles of An Effective ManagerDocument15 pagesRoles of An Effective ManagerMarin, Nicole DondoyanoNo ratings yet

- 2new Risk Theory of Profit 2.Document22 pages2new Risk Theory of Profit 2.ilyasriyazNo ratings yet

- Selected Ratios DOCSDocument1 pageSelected Ratios DOCSanon_851202775No ratings yet

- PAKIAO WORKERS EXPLAINEDDocument4 pagesPAKIAO WORKERS EXPLAINEDgemma acostaNo ratings yet

- EC334 Assessment Instructions: Please Complete All ProblemsDocument4 pagesEC334 Assessment Instructions: Please Complete All ProblemsMiiwKotiramNo ratings yet

- Limited Liability and Incentive QNTR T With Ex-Ante Action HDocument23 pagesLimited Liability and Incentive QNTR T With Ex-Ante Action HscottlinyupengNo ratings yet

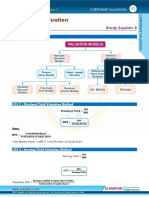

- Corporate ValuationDocument7 pagesCorporate ValuationVaibhav GandhiNo ratings yet

- IAS 37 Provisions, Contingent Liabilities and Contingent AssetsDocument7 pagesIAS 37 Provisions, Contingent Liabilities and Contingent AssetsMd Mahmudul HassanNo ratings yet

- DMMO (1) HiddenActionDocument69 pagesDMMO (1) HiddenActionJohnny SinsNo ratings yet

- Investment in Debt SecuritiesDocument10 pagesInvestment in Debt SecuritiesSUBA, Michagail D.No ratings yet

- ECON254 Lecture9 Managerial TheoriesDocument40 pagesECON254 Lecture9 Managerial TheoriesKhalid JassimNo ratings yet

- Actuarial 4Document21 pagesActuarial 4Rochana RamanayakaNo ratings yet

- Franchise Accounting Notes and QuizzerDocument10 pagesFranchise Accounting Notes and QuizzerAman SinayaNo ratings yet

- Compensation and Benefits Comparison among Bangladeshi CompaniesDocument9 pagesCompensation and Benefits Comparison among Bangladeshi CompaniesShahrukh HossainNo ratings yet

- How To Employ Your Own Boss THE ULTIMATE GUIDE How To Move From Being An Employee to EmployerFrom EverandHow To Employ Your Own Boss THE ULTIMATE GUIDE How To Move From Being An Employee to EmployerNo ratings yet

- COBIT5-Assessment-Scoping-ToolDocument42 pagesCOBIT5-Assessment-Scoping-ToolasalihovicNo ratings yet

- MTH601 Final Term Solved Mega File by RizwanDocument80 pagesMTH601 Final Term Solved Mega File by RizwanEver GreenNo ratings yet

- Branch and BoundDocument6 pagesBranch and Boundsantosh.parsaNo ratings yet

- Kaolin by Oxalic Acid in Bench-Scale Stirred-Tank ReactorDocument8 pagesKaolin by Oxalic Acid in Bench-Scale Stirred-Tank ReactorValentin GnoumouNo ratings yet

- Dynamic Stiffness Optimization Using Radioss PDFDocument11 pagesDynamic Stiffness Optimization Using Radioss PDFGovindSahuNo ratings yet

- Dynamics of Mechatronics System PDFDocument350 pagesDynamics of Mechatronics System PDFronaldbolorbaral8809No ratings yet

- OCCAM2DDocument12 pagesOCCAM2Daoeuaoeu8No ratings yet

- Microeconomics 1st Edition Acemoglu Test Bank 1Document35 pagesMicroeconomics 1st Edition Acemoglu Test Bank 1russell100% (50)

- Math 180.1 ModellingDocument19 pagesMath 180.1 Modellinglucy heartfiliaNo ratings yet

- Conceptos Básicos de Optimización v2Document31 pagesConceptos Básicos de Optimización v2Andres Milquez100% (1)

- Calculation of Portal Frame DeflectionDocument3 pagesCalculation of Portal Frame DeflectionKonstantinos KalemisNo ratings yet

- Agregate Planning Methods - 2 (Con.)Document10 pagesAgregate Planning Methods - 2 (Con.)Kl OteenNo ratings yet

- Arena OptQuest User's GuideDocument52 pagesArena OptQuest User's GuideFrancisco GimenezNo ratings yet

- Elegance-Open-19 11 19Document2 pagesElegance-Open-19 11 19eajNo ratings yet

- Design Exploration Users GuideDocument296 pagesDesign Exploration Users GuideAnonymous scnl9rH100% (2)

- BBA 2nd Semester Course DetailsDocument14 pagesBBA 2nd Semester Course DetailsKunal SharmaNo ratings yet

- Spe 169366 MSDocument20 pagesSpe 169366 MSEdgar GonzalezNo ratings yet

- Can We Make Genetic Algorithms Work in High-Dimensionality Problems?Document17 pagesCan We Make Genetic Algorithms Work in High-Dimensionality Problems?kilo929756No ratings yet

- Distribution Network ReinforcementDocument6 pagesDistribution Network ReinforcementDan SloboNo ratings yet

- Unit CommitmentDocument53 pagesUnit CommitmentShofi FahizNo ratings yet

- Manufacturing Technology (ME461) Lecture29Document14 pagesManufacturing Technology (ME461) Lecture29Jayant Raj SauravNo ratings yet

- OrCAD PSpice Advanced AnalysisDocument2 pagesOrCAD PSpice Advanced AnalysisdavkavkaNo ratings yet

- Transportation ProblemDocument27 pagesTransportation ProblemAthiraNo ratings yet

- Test Bank For Business Analytics 3rd by EvansDocument5 pagesTest Bank For Business Analytics 3rd by Evansjezebelrosabella17pgNo ratings yet

- Optimal Capacitor Placement Using EtapDocument8 pagesOptimal Capacitor Placement Using Etapjoydeep_d3232No ratings yet

- Benchmark Functions For CEC 2015 Special Session and Competition On Dynamic Multi-Objective OptimizationDocument7 pagesBenchmark Functions For CEC 2015 Special Session and Competition On Dynamic Multi-Objective OptimizationAmreen KhanNo ratings yet

- 13 Chapter-5Document88 pages13 Chapter-5RevanKumarBattuNo ratings yet

- CB2203 2023-24 Sem A Assignment 2Document4 pagesCB2203 2023-24 Sem A Assignment 2jackychan3118No ratings yet

- A Hierarchical Architecture For Human-Robot Cooperation ProcessesDocument20 pagesA Hierarchical Architecture For Human-Robot Cooperation ProcessesnykaelNo ratings yet

- Optimisation of Diesel and Gasoline Blending OperationsDocument181 pagesOptimisation of Diesel and Gasoline Blending Operationsrameshkarthik810No ratings yet