You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Capital and Revenue ExpenditureDocument2 pagesCapital and Revenue Expenditureyaivna gopeeNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Unit 3: Bad Debts, Allowance For Doubtful Debts, Accruals and PrepaymentsDocument12 pagesUnit 3: Bad Debts, Allowance For Doubtful Debts, Accruals and Prepaymentsyaivna gopee100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Unit 2: Accounting Concepts and Trial BalanceDocument12 pagesUnit 2: Accounting Concepts and Trial Balanceyaivna gopeeNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Unit 1: Role OF Accounting Information AND Recording and Summarising TransactionsDocument11 pagesUnit 1: Role OF Accounting Information AND Recording and Summarising Transactionsyaivna gopeeNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Margarine InfoDocument2 pagesMargarine Infoyaivna gopee100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- History of Nestle: The LogoDocument4 pagesHistory of Nestle: The Logoyaivna gopeeNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Csec Poa: Page 8 of 24Document1 pageCsec Poa: Page 8 of 24Tori GeeNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Cheap Air Tickets Online, International Flights To India, Cheap International Flight Deals - SpiceJet Airlines PDFDocument2 pagesCheap Air Tickets Online, International Flights To India, Cheap International Flight Deals - SpiceJet Airlines PDFkrissregionNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Standard Accounts: IntroducingDocument24 pagesStandard Accounts: IntroducingsathishNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- S.no Customer Name Prospect / Lead Name Contact Number Decision Maker / Influencer / HelperDocument4 pagesS.no Customer Name Prospect / Lead Name Contact Number Decision Maker / Influencer / Helperaptude solNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Naval Dockyard CoDocument45 pagesNaval Dockyard CoUmesh Gaikwad100% (2)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- PBP II Chapter 14 Installment PurchasesDocument53 pagesPBP II Chapter 14 Installment PurchasesJorge Luna RamirezNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Banking Sector in CambodiaDocument44 pagesBanking Sector in CambodiaChanrithy Sok100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Receivables TheoriesDocument8 pagesReceivables TheoriesIris MnemosyneNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Study On A Financial Performance Analysis of Private Banks in IndiaDocument26 pagesA Study On A Financial Performance Analysis of Private Banks in Indiashrisha sharma100% (1)

- Westmont Bank V OngDocument4 pagesWestmont Bank V Ongmodernelizabennet100% (4)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Lebanese Crisis PDFDocument4 pagesLebanese Crisis PDFgeorges khairallahNo ratings yet

- Newsearchalgorithm PDFDocument15 pagesNewsearchalgorithm PDFYogesh PrasadNo ratings yet

- ATM Banking System (18192203029)Document4 pagesATM Banking System (18192203029)Md. Monir Hossain029321No ratings yet

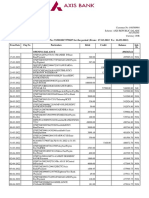

- Statement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Document7 pagesStatement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Om Namah ShivayNo ratings yet

- BilledStatements 4806 16-10-22 18.18Document2 pagesBilledStatements 4806 16-10-22 18.18Harsh NawariaNo ratings yet

- NBFC Module 2 CompletedDocument27 pagesNBFC Module 2 CompletedAneesha AkhilNo ratings yet

- IslamicDocument4 pagesIslamicSarawathi ThulasiNo ratings yet

- DocxDocument358 pagesDocxAina AguirreNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Chanda Kochhar SlidesDocument28 pagesChanda Kochhar SlidesBhawna DhamijaNo ratings yet

- Friendly Loan MouDocument6 pagesFriendly Loan Mouabdullah maknojiaNo ratings yet

- Module 2Document41 pagesModule 2Sujata SarkarNo ratings yet

- Consolidated Plywood Industries VsDocument2 pagesConsolidated Plywood Industries VsDavid Lawrenz Samonte100% (2)

- Banks and Banking System-1Document13 pagesBanks and Banking System-1polmulitriNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Yojana May 2017 PDFDocument80 pagesYojana May 2017 PDFApekshaNo ratings yet

- Audit of Cash Bank ReconDocument8 pagesAudit of Cash Bank ReconPaul Mc AryNo ratings yet

- CSX Inv SS PDFDocument1 pageCSX Inv SS PDFimdad aliNo ratings yet

- Invoice SHPL 22-23 055 2023-03-31Document2 pagesInvoice SHPL 22-23 055 2023-03-31vconceiveNo ratings yet

- Subiecte Engleza Economie Iulie 2021Document7 pagesSubiecte Engleza Economie Iulie 2021Fishu FishuNo ratings yet

- Role of RbiDocument4 pagesRole of Rbitejas1989No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)