You might also like

- Harvest StrategyDocument3 pagesHarvest StrategyAkash NelsonNo ratings yet

- Nokia 139cm 55 Inch Ultra HD 4K LED Smart Android TV With Sound by JBLDocument1 pageNokia 139cm 55 Inch Ultra HD 4K LED Smart Android TV With Sound by JBLDevNo ratings yet

- ThetaEarner AlgoReportDocument2 pagesThetaEarner AlgoReportSabah SaleemNo ratings yet

- Business PlanDocument13 pagesBusiness PlanKaushik singhNo ratings yet

- OD427743863842473100Document1 pageOD427743863842473100Srivatsa JoisNo ratings yet

- The Mavericks - Moody's Case Study - FinalDocument67 pagesThe Mavericks - Moody's Case Study - Finalabcd_123425No ratings yet

- PassiveIncomeEarner AlgoReportDocument2 pagesPassiveIncomeEarner AlgoReportSabah SaleemNo ratings yet

- Od329890418224625100 1Document1 pageOd329890418224625100 1aks.gdg1No ratings yet

- OD429147449876975100Document1 pageOD429147449876975100jbalapragashpathi2005No ratings yet

- Invoice OD116706386055987000Document1 pageInvoice OD116706386055987000Chirag Gupta100% (1)

- Biology NotesDocument1 pageBiology Notesranjeet3098photo2No ratings yet

- TP-Link Archer C64 AC1200 Gigabit MU-MIMO 1200 Mbps Router: Grand Total 1814.00Document1 pageTP-Link Archer C64 AC1200 Gigabit MU-MIMO 1200 Mbps Router: Grand Total 1814.00Abhik TestNo ratings yet

- Boat Power BankDocument1 pageBoat Power Banktuhinpaul098No ratings yet

- 1805 PCSCL DGDocument1 page1805 PCSCL DGAjay SinghNo ratings yet

- HakunaMatata TATA Token Whitepaper v1.3.5Document25 pagesHakunaMatata TATA Token Whitepaper v1.3.5Kraft DinnerNo ratings yet

- Highlander Men's Printed Casual Shirt: Grand Total 516.00Document1 pageHighlander Men's Printed Casual Shirt: Grand Total 516.00prachiNo ratings yet

- Whitepaper V.: Tokenised Hedge FundDocument19 pagesWhitepaper V.: Tokenised Hedge FundaKNo ratings yet

- Od 226190120715633000Document1 pageOd 226190120715633000rajeshbhramaNo ratings yet

- Sawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketDocument10 pagesSawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketbodaiNo ratings yet

- Wa0035.Document1 pageWa0035.computeraa998No ratings yet

- Welcome To: Cloud MiningDocument1 pageWelcome To: Cloud MiningSatish YadavNo ratings yet

- Toaz - Info Flipkart Fake Bill PRDocument1 pageToaz - Info Flipkart Fake Bill PRimrankhan.org1No ratings yet

- Micromax Video 2 (Grey) : Grand TotalDocument2 pagesMicromax Video 2 (Grey) : Grand TotalMeraj MominNo ratings yet

- InvoiceDocument2 pagesInvoicengrsharksNo ratings yet

- IAS Trade Zone - 427 - 19-09-2023Document1 pageIAS Trade Zone - 427 - 19-09-2023Engr Muhammad Haider AliNo ratings yet

- Od112909739888474000 PDFDocument1 pageOd112909739888474000 PDFJatin PatelNo ratings yet

- Acer Swift 3 - InvoiceDocument2 pagesAcer Swift 3 - InvoiceSambhav MEHTANo ratings yet

- Od 119349285774530000Document1 pageOd 119349285774530000RISHABH YADAVNo ratings yet

- Fastrack Reflex Play+ 1.3 AMOLED Display - BT Calling - 25+ Sports Modes - Smartwatch SmartwatchDocument1 pageFastrack Reflex Play+ 1.3 AMOLED Display - BT Calling - 25+ Sports Modes - Smartwatch SmartwatchSanju MondalNo ratings yet

- Sovrenn Times 8 Aug 2023Document28 pagesSovrenn Times 8 Aug 2023ReparatedNo ratings yet

- Od115470184212908000 PDFDocument1 pageOd115470184212908000 PDFAnonymous 5jDXmFPNo ratings yet

- Samsung 6.5 KG Activwash+ Fully Automatic Top Load Grey: 048P5Pbn100022Document1 pageSamsung 6.5 KG Activwash+ Fully Automatic Top Load Grey: 048P5Pbn100022Ravindar aNo ratings yet

- p6364MktHi - 1704996985825 - Trimmer BillDocument1 pagep6364MktHi - 1704996985825 - Trimmer BillKhandani ZayeqaNo ratings yet

- ACCA P4 Mock Exam QuestionsDocument13 pagesACCA P4 Mock Exam QuestionsGeo DonNo ratings yet

- Redmi 3S (Grey, 16Gb) : #FABA6P1800724654Document1 pageRedmi 3S (Grey, 16Gb) : #FABA6P1800724654Meraj MominNo ratings yet

- ReserveDocument2 pagesReserverashishanandNo ratings yet

- Nokia 6.1 Copper, Black, 32 GB: Grand Total 6999.00Document2 pagesNokia 6.1 Copper, Black, 32 GB: Grand Total 6999.00anon_174779098No ratings yet

- Alpha GPTDocument1 pageAlpha GPTwww.auwarlahmard9068No ratings yet

- Petronas Gas Berhad: Off To A Good Start - 30/08/2010Document3 pagesPetronas Gas Berhad: Off To A Good Start - 30/08/2010Rhb InvestNo ratings yet

- Bill To: Apple Iphone 7 (Silver)Document1 pageBill To: Apple Iphone 7 (Silver)Anonymous 5c39IeGNo ratings yet

- ST WilfredDocument1 pageST WilfredVimlaNo ratings yet

- Dizo Watch D2 With 1.91 Inch Super Big Display, BT Calling (By Realme Techlife)Document2 pagesDizo Watch D2 With 1.91 Inch Super Big Display, BT Calling (By Realme Techlife)Prateek PalNo ratings yet

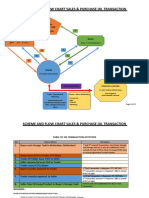

- FINAL - REVISED. Scheme and Flow Chart OIL TransactionDocument4 pagesFINAL - REVISED. Scheme and Flow Chart OIL TransactionPebb PondNo ratings yet

- MCQ 6019 TestDocument38 pagesMCQ 6019 TestpathiranapremabanduNo ratings yet

- Invoice OD111025894559836000Document1 pageInvoice OD111025894559836000Husen GhoriNo ratings yet

- Od 329531885760562100Document1 pageOd 329531885760562100pharmacy2029No ratings yet

- Asus ROG Strix G Core I5 9th Gen - 8 GB/1 TB HDD /windows 10 Home/4 GB Graphics G531GD-BQ036T Gaming LaptopDocument1 pageAsus ROG Strix G Core I5 9th Gen - 8 GB/1 TB HDD /windows 10 Home/4 GB Graphics G531GD-BQ036T Gaming Laptopsaajid rock'sNo ratings yet

- Mi 20000 Mah Power Bank (Plm06Zm, 2I) : Grand Total 1499.00Document1 pageMi 20000 Mah Power Bank (Plm06Zm, 2I) : Grand Total 1499.00Mel Vin PinNo ratings yet

- Invoice OD212378379192868000Document1 pageInvoice OD212378379192868000Shadaab HamidiNo ratings yet

- Flipkart Invoice 24 - 10 - 2020Document1 pageFlipkart Invoice 24 - 10 - 2020imrankhan.org1No ratings yet

- OD427749033708254100Document1 pageOD427749033708254100ANSARI MOHD MOKARRAM ZAINUL ABD-CSE SORTNo ratings yet

- Qun SagarDocument1 pageQun SagarPANKAJ RAJNo ratings yet

- Celestron 94244 Enhance Your Experience Telescope Filter, 8"Document1 pageCelestron 94244 Enhance Your Experience Telescope Filter, 8"MONIL NARANGNo ratings yet

- Important Questions For Icai BCKDocument1 pageImportant Questions For Icai BCKproopa698No ratings yet

- Smartwatch InvoiceDocument1 pageSmartwatch InvoiceM IrajNo ratings yet

- Invoice OD122302741189254000Document1 pageInvoice OD122302741189254000vkoritalaNo ratings yet

- Cardano vs. PolkadotDocument24 pagesCardano vs. PolkadotsfjsNo ratings yet

- AllRounder AlgoReportDocument2 pagesAllRounder AlgoReportSabah SaleemNo ratings yet

- Invoice OD211779487755330000Document1 pageInvoice OD211779487755330000chinna rajaNo ratings yet

- Beardo Trimer Invoice PDFDocument1 pageBeardo Trimer Invoice PDFSanjay SinghNo ratings yet

- Awais Ahmed Awan BBA 6B 1711267 HRM Project On NestleDocument11 pagesAwais Ahmed Awan BBA 6B 1711267 HRM Project On NestleQadirNo ratings yet

- Purchase Order TemplateDocument8 pagesPurchase Order TemplateromeeNo ratings yet

- HRM & Finance-Jivraj TeaDocument88 pagesHRM & Finance-Jivraj TeaYash KothariNo ratings yet

- Fauji Fertilizer Company LimitedDocument74 pagesFauji Fertilizer Company LimitedAnaya Choudhry75% (4)

- Organisational CultureDocument26 pagesOrganisational CultureAditi Basnet100% (1)

- Call Center Metrics Paper Staff IDocument27 pagesCall Center Metrics Paper Staff Imaka.palma7404100% (1)

- Entrep Quiz 2Document20 pagesEntrep Quiz 2encarNo ratings yet

- Business Case Ppt-CorporateDocument24 pagesBusiness Case Ppt-Corporatesambaran PGPM17No ratings yet

- Sample Problems On Relevant CostsDocument9 pagesSample Problems On Relevant CostsJames Ryan AlzonaNo ratings yet

- Marketing Research Final PresentationDocument14 pagesMarketing Research Final Presentationcarlos sepulvedaNo ratings yet

- List of Ledgers and It's Under Group in TallyDocument5 pagesList of Ledgers and It's Under Group in Tallyrachel KujurNo ratings yet

- Frist Pacific Mining Lao Co.,LTD 27-28 Invoice (USD)Document2 pagesFrist Pacific Mining Lao Co.,LTD 27-28 Invoice (USD)thanakorn phetxaysyNo ratings yet

- Faisal WorksheetDocument5 pagesFaisal WorksheetAbdul MateenNo ratings yet

- 哈佛商业评论 (Harvard Business Review)Document7 pages哈佛商业评论 (Harvard Business Review)h68f9trq100% (1)

- Dubois Et Fils Shareholder BenefitsDocument5 pagesDubois Et Fils Shareholder BenefitsCrowdfundInsiderNo ratings yet

- Lesson 4-7Document79 pagesLesson 4-7marivic franciscoNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- AFAR 1 SyllabusDocument12 pagesAFAR 1 SyllabusJamaica DavidNo ratings yet

- RocheDocument5 pagesRochePrattouNo ratings yet

- Family OfficeDocument1 pageFamily OfficeTurcan Ciprian Sebastian100% (1)

- Internal Audit: How To Perform Internal Audit of Manufacturing CompaniesDocument19 pagesInternal Audit: How To Perform Internal Audit of Manufacturing CompaniesNilesh MandlikNo ratings yet

- ACCOUNTS (858) : Class XiDocument4 pagesACCOUNTS (858) : Class XiYour Laptop GuideNo ratings yet

- Factura Comercial RealizadaDocument1 pageFactura Comercial Realizadafernando jose chuquijajas rodriguezNo ratings yet

- Integrity Pledge - DPWH DO 086 - S2013Document2 pagesIntegrity Pledge - DPWH DO 086 - S2013Arangkada Philippines94% (17)

- The Consumer Protection ActDocument4 pagesThe Consumer Protection ActRijurahul Agarwal SinghNo ratings yet

- Intro - S4HANA - Using - Global - Bike - Case - Study - PP - Fiori - en - v3.3 (Step 10)Document5 pagesIntro - S4HANA - Using - Global - Bike - Case - Study - PP - Fiori - en - v3.3 (Step 10)Rodrigo Alonso Rios AlcantaraNo ratings yet

- MGT 263 Assignment 1Document8 pagesMGT 263 Assignment 1Aysha Muhammad ShahzadNo ratings yet

- Financial Analysis and Valuation of TREATT PLCDocument71 pagesFinancial Analysis and Valuation of TREATT PLCPanagiotis TzavidasNo ratings yet

- Formal Negotiating: Some Questions Answered in This Chapter AreDocument24 pagesFormal Negotiating: Some Questions Answered in This Chapter AreNguyễn Phi YếnNo ratings yet