You might also like

- Quants MMDocument65 pagesQuants MMTu DuongNo ratings yet

- Risk Analysis in Capital Investment DecisionsDocument57 pagesRisk Analysis in Capital Investment Decisionsanindya_kundu100% (1)

- Topic 4 Financial FunctionsDocument21 pagesTopic 4 Financial FunctionsLê Thiên Giang 2KT-19No ratings yet

- CSI FormulasDocument8 pagesCSI Formulasgrz7gtqq9bNo ratings yet

- Corporate Finance Professional Certificate MOOC Course 2, The Free Cash Flow Method For Firm Valuation Module 4, Relative ValuationDocument1 pageCorporate Finance Professional Certificate MOOC Course 2, The Free Cash Flow Method For Firm Valuation Module 4, Relative ValuationtotiNo ratings yet

- 2022 LI QuantMethodsDocument109 pages2022 LI QuantMethodssharma02decNo ratings yet

- Basic Finance FormulasDocument1 pageBasic Finance Formulasmafe moraNo ratings yet

- C1M1 QRG PDFDocument1 pageC1M1 QRG PDFRamen ACCANo ratings yet

- Summary Notes Columbia Uni PDFDocument1 pageSummary Notes Columbia Uni PDFNIKHIL SODHINo ratings yet

- Corporate Finance Professional Certificate MOOCDocument1 pageCorporate Finance Professional Certificate MOOCEmmanuel PonceNo ratings yet

- Corporate Finance Professional Certificate MOOCDocument1 pageCorporate Finance Professional Certificate MOOCkolya viktorNo ratings yet

- C1M1 QRG PDFDocument1 pageC1M1 QRG PDFRamen ACCANo ratings yet

- Microsoft Word - Module 1 Cheat Sheet UpdatedDocument1 pageMicrosoft Word - Module 1 Cheat Sheet UpdatedJose NavarroNo ratings yet

- Financial Reading 3 - ScribdDocument3 pagesFinancial Reading 3 - ScribdSanjay KumarNo ratings yet

- FinalsheetDocument1 pageFinalsheetdgfnjmfgNo ratings yet

- Introduction To Valuation - The Time Value of MoneyDocument8 pagesIntroduction To Valuation - The Time Value of MoneyPia AlcantaraNo ratings yet

- Chapter3 EFA2 NPVDocument29 pagesChapter3 EFA2 NPVDương DươngNo ratings yet

- Corporate Finance Professional Certificate MOOC: Quick Reference GuideDocument1 pageCorporate Finance Professional Certificate MOOC: Quick Reference GuideShivani AgarwalNo ratings yet

- 1riskanalysisincapitalbudgeting 150514064344 Lva1 App6892Document70 pages1riskanalysisincapitalbudgeting 150514064344 Lva1 App6892Perarasi b lNo ratings yet

- Salt Cfa Level 1 Formulasheet 2022 3Document21 pagesSalt Cfa Level 1 Formulasheet 2022 3Sam SoranNo ratings yet

- Wharton On Coursera: Introduction To Corporate Finance: DiscountingDocument7 pagesWharton On Coursera: Introduction To Corporate Finance: Discountingjhon doeNo ratings yet

- Financing Your GrowthDocument81 pagesFinancing Your Growthtidiane.syNo ratings yet

- 365+corporate Finance FormulasDocument6 pages365+corporate Finance FormulasSouradeep MondalNo ratings yet

- ENECON ReviewerDocument5 pagesENECON ReviewerJomeljames Campaner PanganibanNo ratings yet

- BM2102 Lecture 7Document48 pagesBM2102 Lecture 7shahnaz chNo ratings yet

- Finmar FormulaDocument2 pagesFinmar FormulaCPAs AccountNo ratings yet

- ch1 Notes CfaDocument18 pagesch1 Notes Cfaashutosh JhaNo ratings yet

- C2 Revision of Concepts v1Document11 pagesC2 Revision of Concepts v1Umer FarooqNo ratings yet

- FINMAR - Time Value of MoneyDocument2 pagesFINMAR - Time Value of MoneySean Patrick C. WONGNo ratings yet

- Time Value of Money Cheat Sheet: by ViaDocument3 pagesTime Value of Money Cheat Sheet: by ViaTechbotix AppsNo ratings yet

- Finanical Management Ch4Document60 pagesFinanical Management Ch4Chucky ChungNo ratings yet

- Chapter 2 - Time Value of Money and Its ApplicationDocument69 pagesChapter 2 - Time Value of Money and Its ApplicationQUYÊN VŨ THỊ THUNo ratings yet

- Capital Budgeting: Factors of Consideration Net Investments Net Returns Cost of CapitalDocument2 pagesCapital Budgeting: Factors of Consideration Net Investments Net Returns Cost of CapitalMary Hazell Victori100% (1)

- The Time Value of MoneyDocument2 pagesThe Time Value of Moneypier AcostaNo ratings yet

- Time Value of MoneyDocument7 pagesTime Value of Moneysincere sincereNo ratings yet

- Green Abstract Things Your Need To Analyze InfographicDocument2 pagesGreen Abstract Things Your Need To Analyze InfographicAmira AffendyNo ratings yet

- MB - Group Assignent 1Document32 pagesMB - Group Assignent 1Doan BùiNo ratings yet

- Present Values and Future ValuesDocument50 pagesPresent Values and Future Valueskaylakshmi8314100% (1)

- What Is The Absolute Valuation Model?Document37 pagesWhat Is The Absolute Valuation Model?Eric McLaughlinNo ratings yet

- Time ValueDocument9 pagesTime ValueBenita BijuNo ratings yet

- L1 2024 Formula SheetDocument17 pagesL1 2024 Formula SheetfofyibaydoNo ratings yet

- Business Valuation: Introduction To Financial MethodsDocument23 pagesBusiness Valuation: Introduction To Financial MethodsfrancescoabcNo ratings yet

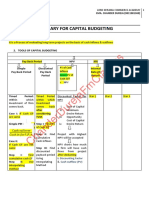

- Chanderdurejafmclasses: Summary For Capital BudgetingDocument5 pagesChanderdurejafmclasses: Summary For Capital BudgetingShiva AroraNo ratings yet

- Discounting Cash FlowsDocument5 pagesDiscounting Cash FlowsDriton BinaNo ratings yet

- Ufanpv Irr1.2Document45 pagesUfanpv Irr1.2mayankNo ratings yet

- Managerial Economics: An Analysis of Business IssuesDocument25 pagesManagerial Economics: An Analysis of Business IssuesMamta GanatwarNo ratings yet

- Module 1 - Basic Finance ConceptsDocument1 pageModule 1 - Basic Finance ConceptsJeniffer FrançaNo ratings yet

- Capital Budgeting V2 - Click Read Only To View DocumentDocument40 pagesCapital Budgeting V2 - Click Read Only To View Documentzia hussain100% (1)

- Quantitative Methods 2345Document21 pagesQuantitative Methods 2345Cristina RiveraNo ratings yet

- The Time Value of MoneyDocument43 pagesThe Time Value of MoneykamleshNo ratings yet

- Damodaran On ValuationDocument102 pagesDamodaran On Valuationgioro_mi100% (4)

- Level 1 2022 Formula SheetDocument16 pagesLevel 1 2022 Formula SheetxxNo ratings yet

- Chapter Three PDFDocument46 pagesChapter Three PDFSeyoum LeulNo ratings yet

- MM L1 Formula SheetDocument20 pagesMM L1 Formula SheetMlungisi MalazaNo ratings yet

- Capital Budgeting V2 - Click Read Only To View DocumentDocument40 pagesCapital Budgeting V2 - Click Read Only To View DocumentSamantha Meril PandithaNo ratings yet

- Lab PKSB Session 1 - BlankDocument34 pagesLab PKSB Session 1 - Blankalanablues1No ratings yet

- Engr 222 NotesDocument89 pagesEngr 222 NotesnandiniNo ratings yet

- Engineering Economy Module 5Document2 pagesEngineering Economy Module 5Mark Renbel ParanNo ratings yet

- Financing Your Business: Start-Up BriefingDocument4 pagesFinancing Your Business: Start-Up BriefingANASNo ratings yet

- Cfa QuantsDocument102 pagesCfa QuantsANASNo ratings yet

- Sample Management LetterDocument9 pagesSample Management LetterAdil MahmudNo ratings yet

- K-AP-1 - Fixed Assets and DepreciationDocument12 pagesK-AP-1 - Fixed Assets and DepreciationANAS100% (1)

- Changes in The Sales Tax Act 1990Document13 pagesChanges in The Sales Tax Act 1990ANASNo ratings yet

- Income Tax NotesDocument17 pagesIncome Tax NotesANASNo ratings yet

- Audit Study SequenceDocument2 pagesAudit Study SequenceANASNo ratings yet

- University of Karachi: M.A. Economics & Finance Management Theory and PracticeDocument1 pageUniversity of Karachi: M.A. Economics & Finance Management Theory and PracticeANASNo ratings yet

- Marketing Your Business: Start-Up BriefingDocument4 pagesMarketing Your Business: Start-Up BriefingANASNo ratings yet

- Classical Theories (Part I-01)Document6 pagesClassical Theories (Part I-01)ANASNo ratings yet

- University of Karachi: M.A. Economics & Finance Management Theory and PracticeDocument1 pageUniversity of Karachi: M.A. Economics & Finance Management Theory and PracticeANASNo ratings yet

- Mind Map 13 - ETHICS PDFDocument1 pageMind Map 13 - ETHICS PDFsaeed_r2000422No ratings yet

- Advertising: Start-Up BriefingDocument4 pagesAdvertising: Start-Up BriefingANASNo ratings yet

- 03 - Organization and Types (Part III-01)Document3 pages03 - Organization and Types (Part III-01)ANASNo ratings yet

- DirectorsDocument1 pageDirectorsANASNo ratings yet

- F7 Mock DEC 2013Document14 pagesF7 Mock DEC 2013ANASNo ratings yet

- f8 TocDocument41 pagesf8 TocANASNo ratings yet

- TOC and SP PDFDocument33 pagesTOC and SP PDFANAS0% (1)

- ACCA Answer BookletDocument1 pageACCA Answer BookletM Muneeb Saeed0% (1)

- Ethical Threats To IndependenceDocument4 pagesEthical Threats To IndependenceANASNo ratings yet

- Mind Map 1 - GovernanceDocument1 pageMind Map 1 - GovernanceTisha Laetitia ChinNo ratings yet

- Audit IDocument1 pageAudit IANASNo ratings yet

- Acca F8 LecturesDocument143 pagesAcca F8 LecturesANASNo ratings yet

- S0cial & Environmental AccountingDocument1 pageS0cial & Environmental AccountingANASNo ratings yet

- Mind Map 1 - GovernanceDocument1 pageMind Map 1 - GovernanceTisha Laetitia ChinNo ratings yet

- Mind Map 3 - Corporate GovernanceDocument1 pageMind Map 3 - Corporate GovernanceANASNo ratings yet

- Mind Map 1 - GovernanceDocument1 pageMind Map 1 - GovernanceTisha Laetitia ChinNo ratings yet

- Part 1 Introduction To P1Document14 pagesPart 1 Introduction To P1ANASNo ratings yet

- Bus Route KarachiDocument39 pagesBus Route KarachiAsif HussainNo ratings yet

- Mean Mode and MedianDocument6 pagesMean Mode and MedianUransh MunjalNo ratings yet

- AssignmentDocument8 pagesAssignmentMartin gufNo ratings yet

- Measures of Relative SkewnessDocument32 pagesMeasures of Relative SkewnessKarl VillegasNo ratings yet

- Itae002 Test 2Document150 pagesItae002 Test 2Nageshwar SinghNo ratings yet

- Rescaled Range Analysis - A Comparative Study On Bombay Stock Exchange and National Stock ExchangeDocument12 pagesRescaled Range Analysis - A Comparative Study On Bombay Stock Exchange and National Stock ExchangeNandita IyerNo ratings yet

- 2016CFA一级强化班 数量Document313 pages2016CFA一级强化班 数量Mario XieNo ratings yet

- Quantitative AnalysisDocument47 pagesQuantitative AnalysisPhương TrinhNo ratings yet

- SASADocument4 pagesSASAlonely ylenolNo ratings yet

- Hasil SPSSDocument28 pagesHasil SPSSFebri ZuanNo ratings yet

- Biostat Lec Part 4 (SV)Document3 pagesBiostat Lec Part 4 (SV)Claudelle MangubatNo ratings yet

- SSC CGL Syllabus Revised 93Document8 pagesSSC CGL Syllabus Revised 93Ashish MehraNo ratings yet

- Multivariate Jump Diffusion Models For The Foreign Exchange MarketDocument33 pagesMultivariate Jump Diffusion Models For The Foreign Exchange MarketSui Kai WongNo ratings yet

- Skew KurtosisDocument7 pagesSkew KurtosiscastjamNo ratings yet

- MachineLearningNotes PDFDocument299 pagesMachineLearningNotes PDFKarthik selvamNo ratings yet

- Syllabus For B.A./ B.Sc. I, II, IIIDocument21 pagesSyllabus For B.A./ B.Sc. I, II, IIIGuru GuroorNo ratings yet

- CBRC Let Review (Assessment of Learning)Document8 pagesCBRC Let Review (Assessment of Learning)Alondra SambajonNo ratings yet

- R MHWDocument189 pagesR MHWIsaias PrestesNo ratings yet

- 4315 Written Project 4 Report Monte Carlo SimulationDocument9 pages4315 Written Project 4 Report Monte Carlo SimulationVictor Marcos Hyslop100% (1)

- Anderson Sweeney Williams Anderson Sweeney WilliamsDocument104 pagesAnderson Sweeney Williams Anderson Sweeney WilliamsElaine MagbuhatNo ratings yet

- J. K. Sharma - Business Statistics-Pearson Education (2007)Document752 pagesJ. K. Sharma - Business Statistics-Pearson Education (2007)Shahryar ahmed92% (37)

- Fitting The Variogram Model of Nickel Laterite UsiDocument11 pagesFitting The Variogram Model of Nickel Laterite Usiis mailNo ratings yet

- Econ3016: Empirical Finance WEEK 3/4Document31 pagesEcon3016: Empirical Finance WEEK 3/4Burka MartynNo ratings yet

- Usability of A Smartphone Application To Support TDocument13 pagesUsability of A Smartphone Application To Support TSha NapolesNo ratings yet

- Moments and Measures of Skewness and KurtosisDocument2 pagesMoments and Measures of Skewness and Kurtosislakhan kharwar0% (1)

- Determination of The Best Fit Probability Distribution For Monthly Rainfall Data in BangladeshDocument5 pagesDetermination of The Best Fit Probability Distribution For Monthly Rainfall Data in BangladeshOscar Romeo BravoNo ratings yet

- QTB Project ReportDocument15 pagesQTB Project ReportjeffNo ratings yet

- Mumbai University - FYBSc - Syllabus - 4.60 Statistics PDFDocument7 pagesMumbai University - FYBSc - Syllabus - 4.60 Statistics PDFreshmarautNo ratings yet

- Clinical SAS TermsDocument12 pagesClinical SAS TermsRachapudi SumanNo ratings yet

- N1a117124 - Ana Sandra PidahDocument145 pagesN1a117124 - Ana Sandra PidahAna sandra pidahNo ratings yet

- Sumedha July-Sept Full TextDocument18 pagesSumedha July-Sept Full TextsreelakshmipagoluNo ratings yet