You might also like

- 9 168493-2013-Philippine Airlines Inc. v. Commissioner ofDocument14 pages9 168493-2013-Philippine Airlines Inc. v. Commissioner ofCamille CruzNo ratings yet

- PAL Vs CIR Proper Party To File Refund 1Document12 pagesPAL Vs CIR Proper Party To File Refund 1Evan NervezaNo ratings yet

- Philippine Airline Vs CIR GR No. 198759Document26 pagesPhilippine Airline Vs CIR GR No. 198759Janin GallanaNo ratings yet

- Phil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Document8 pagesPhil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Lou Ann AncaoNo ratings yet

- PAL vs. CIRDocument16 pagesPAL vs. CIRVictoria aytonaNo ratings yet

- PAL v. CIRDocument2 pagesPAL v. CIRSanNo ratings yet

- Philippine Airlines Vs CIR DigestDocument2 pagesPhilippine Airlines Vs CIR DigestlumengggNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryUnicorns Are RealNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryL-Shy KïmNo ratings yet

- Philippine Airlines vs. CirDocument2 pagesPhilippine Airlines vs. CirTheodore0176100% (1)

- Philippine Airlines V CIRDocument5 pagesPhilippine Airlines V CIRBettina Rayos del SolNo ratings yet

- Pal vs. CirDocument2 pagesPal vs. CirKarla BeeNo ratings yet

- Definition, Concept and Purpose of Taxation: Taxation 1 Case Digest Atty. Marvin CaneroDocument13 pagesDefinition, Concept and Purpose of Taxation: Taxation 1 Case Digest Atty. Marvin CaneroStela PantaleonNo ratings yet

- Philippine Airlines V CIRDocument1 pagePhilippine Airlines V CIRZ FNo ratings yet

- Silkair Vs CIRDocument16 pagesSilkair Vs CIRJay TabuzoNo ratings yet

- Philippine Airlines, INC., Petitioner, Commissioner of Internal Revenue, RespondentDocument26 pagesPhilippine Airlines, INC., Petitioner, Commissioner of Internal Revenue, RespondentRA De JoyaNo ratings yet

- Tax 2Document96 pagesTax 2Luis de leonNo ratings yet

- Silkair (Singapore) Pte, Ltd. vs. Commissioner of Internal Revenue 544 SCRA 100Document18 pagesSilkair (Singapore) Pte, Ltd. vs. Commissioner of Internal Revenue 544 SCRA 100BernsNo ratings yet

- PAL v. CIR (GR 198759)Document2 pagesPAL v. CIR (GR 198759)Erica Gana100% (1)

- 4 Silkair Vs CIRDocument4 pages4 Silkair Vs CIRRobert EspinaNo ratings yet

- PAL Vs CIR DigestDocument2 pagesPAL Vs CIR DigestAnonymous bOncqbp8yiNo ratings yet

- Tax Digests On RemediesDocument22 pagesTax Digests On Remediesmadotan100% (2)

- Personal Notes - CaseDigest - Tax1-AttyCaneroDocument5 pagesPersonal Notes - CaseDigest - Tax1-AttyCaneroStela PantaleonNo ratings yet

- L/epublic of Tbe (!court: IffilanilaDocument16 pagesL/epublic of Tbe (!court: IffilanilaDanica GodornesNo ratings yet

- PAL vs. CIRDocument26 pagesPAL vs. CIRLiezl Oreilly VillanuevaNo ratings yet

- G.R. No. 188497Document15 pagesG.R. No. 188497ericson dela cruzNo ratings yet

- Exxonmobil Petroleum and Chemical HoldingsDocument1 pageExxonmobil Petroleum and Chemical HoldingsDino BacomoNo ratings yet

- Silkair VS Cir, GR No 173594, Feb 6, 2008Document12 pagesSilkair VS Cir, GR No 173594, Feb 6, 2008KidMonkey2299No ratings yet

- 5 Phil Ass SmeltingDocument4 pages5 Phil Ass SmeltingWayne ViernesNo ratings yet

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument39 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentEva TrinidadNo ratings yet

- Silkair V Cir DigestDocument6 pagesSilkair V Cir Digestbdjn bdjnNo ratings yet

- Commissioner of Internal Revenue v. Pilipinas Shell, G.R. 188497, April 25, 2012.Document10 pagesCommissioner of Internal Revenue v. Pilipinas Shell, G.R. 188497, April 25, 2012.Christopher ArellanoNo ratings yet

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument5 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, Respondentavalavenia2abadNo ratings yet

- Spouses Pacquiao vs. CTA and CIRDocument3 pagesSpouses Pacquiao vs. CTA and CIRRhea CagueteNo ratings yet

- Silkair (Singapore) Vs CIRDocument7 pagesSilkair (Singapore) Vs CIRDana CalicaNo ratings yet

- 102 CIR v. Phil. Associated Smelting & Refining Corp., 737 SCRA 328Document3 pages102 CIR v. Phil. Associated Smelting & Refining Corp., 737 SCRA 328Raymond MedinaNo ratings yet

- RANAY Taxrev Case1Document12 pagesRANAY Taxrev Case1Erneylou RanayNo ratings yet

- CIR V CADocument6 pagesCIR V CAChrissyNo ratings yet

- Motion For Reconsideration Filed by Petitioner Chevron Philippines, Inc. (Chevron) 1Document4 pagesMotion For Reconsideration Filed by Petitioner Chevron Philippines, Inc. (Chevron) 1Oliveros DMNo ratings yet

- Customs DoctrinesDocument3 pagesCustoms DoctrinesBernadetteNo ratings yet

- Judicial Procedures Compiled CasesDocument4 pagesJudicial Procedures Compiled CasesVikki AmorioNo ratings yet

- Tariffs & Customs Code - C.T.a.Document5 pagesTariffs & Customs Code - C.T.a.JoAnne Yaptinchay ClaudioNo ratings yet

- En Banc: Resolution ResolutionDocument35 pagesEn Banc: Resolution Resolutionaspiringlawyer1234No ratings yet

- CIR Vs ShellDocument2 pagesCIR Vs ShellSherry Mae Malabago100% (1)

- 4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)Document6 pages4 Commissioner - of - Internal - Revenue - v. - CTA (RESOLUTION)ervingabralagbonNo ratings yet

- Silkair Vs CIRDocument5 pagesSilkair Vs CIRMark DungoNo ratings yet

- Part H 2 - CIR vs. Philippine Associated Smelting and Refining CorpDocument2 pagesPart H 2 - CIR vs. Philippine Associated Smelting and Refining CorpCyruz TuppalNo ratings yet

- CIR Vs Court of Tax Appeals and Petron CorpDocument8 pagesCIR Vs Court of Tax Appeals and Petron CorpAnthony Tamayosa Del AyreNo ratings yet

- Revenue Code (NIRC) Exempt From Excise Tax Is Deemed Illegal or Erroneous, and Should Be Credited orDocument5 pagesRevenue Code (NIRC) Exempt From Excise Tax Is Deemed Illegal or Erroneous, and Should Be Credited orJan Veah CaabayNo ratings yet

- Philippine Airlines v. CIRDocument61 pagesPhilippine Airlines v. CIRBeltran KathNo ratings yet

- CaseDocument6 pagesCaseVanessa GaringoNo ratings yet

- Commissioner of Internal Revenue vs. Pilipinas Shell Petroleum CorporationDocument3 pagesCommissioner of Internal Revenue vs. Pilipinas Shell Petroleum CorporationmjpjoreNo ratings yet

- Rule 41 45 CaseDocument86 pagesRule 41 45 CaseLeizel ZafraNo ratings yet

- Chevron V BIRDocument6 pagesChevron V BIRMark Anthony AlvarioNo ratings yet

- Commissioner of Internal Revenue and Commissioner of Customs v. Philippines Airlines, Inc., G.R. Nos. 212536-37, August 27, 2014Document7 pagesCommissioner of Internal Revenue and Commissioner of Customs v. Philippines Airlines, Inc., G.R. Nos. 212536-37, August 27, 2014Christopher ArellanoNo ratings yet

- Chevron Vs CIRDocument12 pagesChevron Vs CIRMark Anthony AlvarioNo ratings yet

- Petitioner Vs Vs Respondents: Special First DivisionDocument6 pagesPetitioner Vs Vs Respondents: Special First DivisionMaria Rebecca Chua OzaragaNo ratings yet

- Chevron v. CIR (2015)Document47 pagesChevron v. CIR (2015)Avocado DreamsNo ratings yet

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintFrom EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintRating: 4 out of 5 stars4/5 (1)

- Kapatiran NG Mga Naglilingkod Sa Pamahalaan VsDocument5 pagesKapatiran NG Mga Naglilingkod Sa Pamahalaan VsammeNo ratings yet

- Continuos Trial AmendedDocument46 pagesContinuos Trial AmendedammeNo ratings yet

- Ivler Vs San PedroDocument13 pagesIvler Vs San PedroJonathan BacusNo ratings yet

- Malayan vs. PapDocument5 pagesMalayan vs. PapammeNo ratings yet

- Cir Vs Wander Phil, TaxDocument3 pagesCir Vs Wander Phil, TaxClyde MagallanesNo ratings yet

- Adv Consti Disini V Sec of JusticeDocument29 pagesAdv Consti Disini V Sec of JusticeammeNo ratings yet

- Ing Bank vs. CirDocument15 pagesIng Bank vs. CirammeNo ratings yet

- FC-Afisco Insurance Vs CA (1999)Document10 pagesFC-Afisco Insurance Vs CA (1999)Abbot ReyesNo ratings yet

- Delphers Trade V IacDocument5 pagesDelphers Trade V IacLoren SanapoNo ratings yet

- Missioner vs. Javier 199 SCRA 824Document4 pagesMissioner vs. Javier 199 SCRA 824Lord AumarNo ratings yet

- FC-Afisco Insurance Vs CA (1999)Document10 pagesFC-Afisco Insurance Vs CA (1999)Abbot ReyesNo ratings yet

- TAX CASES K Limitations F BasisDocument52 pagesTAX CASES K Limitations F BasisammeNo ratings yet

- Missioner vs. Javier 199 SCRA 824Document4 pagesMissioner vs. Javier 199 SCRA 824Lord AumarNo ratings yet

- COMMISSIONER OF INTERNAL REVENUE vs. Estate of TodaDocument9 pagesCOMMISSIONER OF INTERNAL REVENUE vs. Estate of TodaammeNo ratings yet

- Philippine Acetylene Co. Inc vs. CirDocument6 pagesPhilippine Acetylene Co. Inc vs. CirammeNo ratings yet

- Delphers Trade V IacDocument5 pagesDelphers Trade V IacLoren SanapoNo ratings yet

- Ing Bank vs. CirDocument15 pagesIng Bank vs. CirammeNo ratings yet

- CIR V Central LuzonDocument14 pagesCIR V Central Luzonxeileen08No ratings yet

- Conflict of Laws CasesDocument31 pagesConflict of Laws CasesammeNo ratings yet

- David vs. ArroyoDocument90 pagesDavid vs. ArroyoammeNo ratings yet

- TAX CASES F Extent Scope of TaxDocument14 pagesTAX CASES F Extent Scope of TaxammeNo ratings yet

- Tax Cases B NatureDocument62 pagesTax Cases B NatureammeNo ratings yet

- Silkair Singapore vs. CirDocument15 pagesSilkair Singapore vs. CirammeNo ratings yet

- CIR V Central LuzonDocument14 pagesCIR V Central Luzonxeileen08No ratings yet

- TAX CASES E Purposes and Objectives of TaxDocument25 pagesTAX CASES E Purposes and Objectives of TaxammeNo ratings yet

- Tax Cases D Basis of TaxDocument56 pagesTax Cases D Basis of TaxammeNo ratings yet

- TAX CASES K Limitations F BasisDocument52 pagesTAX CASES K Limitations F BasisammeNo ratings yet

- Cir vs. de La SalleDocument20 pagesCir vs. de La SalleammeNo ratings yet

- TAX CASES E Purposes and Objectives of TaxDocument25 pagesTAX CASES E Purposes and Objectives of TaxammeNo ratings yet

- Natures Wedding PackageDocument2 pagesNatures Wedding PackageJulie Pearl EspisoNo ratings yet

- Licence Fee RevisionDocument2 pagesLicence Fee RevisionAshish KumarNo ratings yet

- Fee Schedule For Law Courses - NIMT 2018Document2 pagesFee Schedule For Law Courses - NIMT 2018Pranjal BajpaiNo ratings yet

- Foxtons Fees and Terms LondonDocument1 pageFoxtons Fees and Terms LondonAlejandroNo ratings yet

- Ko2014augm07 1756842019 9230034684Document2 pagesKo2014augm07 1756842019 9230034684Shoubhik DasNo ratings yet

- AUSTRALIA STUDENT VISA PROCESSING A To ZDocument63 pagesAUSTRALIA STUDENT VISA PROCESSING A To ZEmon AhamedNo ratings yet

- Simplifying BusinessDocument182 pagesSimplifying BusinessniqdelrosarioNo ratings yet

- Opinion No. 17, 2020 - 2Document7 pagesOpinion No. 17, 2020 - 2April Joy AsbocNo ratings yet

- Uttaranchal University Dehradun Fee Structure B.tech (Lateral Entry) 2021-22Document1 pageUttaranchal University Dehradun Fee Structure B.tech (Lateral Entry) 2021-22محمد إحسنNo ratings yet

- Fit Out HandbookDocument70 pagesFit Out HandbookchriisngoNo ratings yet

- Manual of Administrative Policies and Procedures: UniversityDocument5 pagesManual of Administrative Policies and Procedures: UniversityMladen HrvatinNo ratings yet

- ILPA Private Equity PrinciplesDocument16 pagesILPA Private Equity PrinciplesDan PrimackNo ratings yet

- Royal Sarovar Portico: Hotel Confirmation VoucherDocument2 pagesRoyal Sarovar Portico: Hotel Confirmation VoucherArup DattaNo ratings yet

- Birth-Usvr1031962 James Arnold Edownload Us Vitals RecordsDocument3 pagesBirth-Usvr1031962 James Arnold Edownload Us Vitals RecordsJames ArnoldNo ratings yet

- Daftar Akun For MYOBDocument4 pagesDaftar Akun For MYOBsukainaIlhamNo ratings yet

- Tax Invoice: Scorptec ComputersDocument1 pageTax Invoice: Scorptec ComputersRyan Cara0% (1)

- Iesco Online BillDocument2 pagesIesco Online BillHORAIRA ABBASINo ratings yet

- Novy ChargesDocument41 pagesNovy ChargesGavin RozziNo ratings yet

- Enrollment Assessment Form: Class ScheduleDocument1 pageEnrollment Assessment Form: Class SchedulemigsbricksNo ratings yet

- Namibia Consumer Credit Policy-29 May 2020Document27 pagesNamibia Consumer Credit Policy-29 May 2020Milton LouwNo ratings yet

- Css Profile Student GuideDocument1 pageCss Profile Student GuidesofiaNo ratings yet

- Business Plan E&E (CAFE)Document29 pagesBusiness Plan E&E (CAFE)Navdeep Kaur100% (1)

- Baroda UP Gramin Bank 181212Document9 pagesBaroda UP Gramin Bank 181212Sreeram KambhampatiNo ratings yet

- WTS Chalan FormDocument1 pageWTS Chalan FormAteeq SarganaNo ratings yet

- CTU Online InfoDocument4 pagesCTU Online Infojamjayjames3208100% (2)

- MakeMyTrip E Voucher NH210441845617Document2 pagesMakeMyTrip E Voucher NH210441845617Mohandass ArichandranNo ratings yet

- Tax ChecklistDocument1 pageTax ChecklistBily ManNo ratings yet

- Original Proposal of Georgia Bank and Trust To Columbia County For Banking ServicesDocument20 pagesOriginal Proposal of Georgia Bank and Trust To Columbia County For Banking ServicesAllie M GrayNo ratings yet

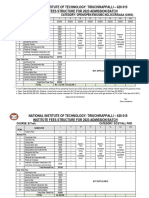

- B.Tech Institute Fee Structure For 2023 24 Admission v2Document4 pagesB.Tech Institute Fee Structure For 2023 24 Admission v2vaikai.kaveriNo ratings yet

- Stretch Wrap RecyclingDocument27 pagesStretch Wrap RecyclingJohn VerneNo ratings yet