You might also like

- New Heritage DollDocument8 pagesNew Heritage DollJITESH GUPTANo ratings yet

- Final Solution - New Heritage Doll CompanyDocument6 pagesFinal Solution - New Heritage Doll CompanyRehan Tyagi100% (2)

- New Heritage Doll Company Capital Budgeting SolutionDocument10 pagesNew Heritage Doll Company Capital Budgeting SolutionBiswadeep royNo ratings yet

- New Heritage Doll CompanDocument9 pagesNew Heritage Doll CompanArima ChatterjeeNo ratings yet

- New Heritage Doll Company Case SolutionDocument31 pagesNew Heritage Doll Company Case SolutionSoundarya AbiramiNo ratings yet

- PGP Heritage Doll ExcelDocument5 pagesPGP Heritage Doll ExcelPGP37 392 Abhishek SinghNo ratings yet

- New Heritage Doll Capital Budgeting Case SolutionDocument5 pagesNew Heritage Doll Capital Budgeting Case Solutionalka murarka50% (14)

- New Heritage Doll Capital Budgeting Case SolutionDocument5 pagesNew Heritage Doll Capital Budgeting Case SolutiontroyanxNo ratings yet

- New Heritage Doll CompanyDocument11 pagesNew Heritage Doll CompanyLightning SalehNo ratings yet

- New Heritage Doll CompanyDocument5 pagesNew Heritage Doll CompanyAnonymous xJLJ4CKNo ratings yet

- New Heritage ExhibitsDocument4 pagesNew Heritage ExhibitsBRobbins12100% (16)

- New Heritage Doll CoDocument3 pagesNew Heritage Doll Copalmis2100% (5)

- New Heritage Doll - SolutionDocument4 pagesNew Heritage Doll - Solutionrath347775% (4)

- Case AnalysisDocument11 pagesCase AnalysisSagar Bansal50% (2)

- New Heritage Doll CompanyDocument5 pagesNew Heritage Doll CompanyRahul LalwaniNo ratings yet

- New Heritage Doll Company:: Capital BudgetingDocument27 pagesNew Heritage Doll Company:: Capital BudgetingInêsRosário100% (8)

- NHDC Solution EditedDocument5 pagesNHDC Solution EditedShreesh ChandraNo ratings yet

- New Heritage Doll Company Case SolutionDocument42 pagesNew Heritage Doll Company Case SolutionRupesh Sharma100% (6)

- Heritage CaseDocument3 pagesHeritage CaseGregory ChengNo ratings yet

- New DollDocument2 pagesNew DollJuyt HertNo ratings yet

- 4214-XLS-ENG New Herritage Doll Case SpreadsheetDocument4 pages4214-XLS-ENG New Herritage Doll Case SpreadsheetAlex HuesingNo ratings yet

- New Heritage Doll CompanyDocument12 pagesNew Heritage Doll CompanyRafael Bosch60% (5)

- New Heritage Doll (NHD) : Figure 1: The Current ProcessDocument2 pagesNew Heritage Doll (NHD) : Figure 1: The Current Processrath3477100% (4)

- NHDC SolutionDocument5 pagesNHDC SolutionShivam Goyal71% (24)

- New Heritage Doll Company Capital BudgetDocument27 pagesNew Heritage Doll Company Capital BudgetCarlos100% (1)

- Flash Memory CaseDocument6 pagesFlash Memory Casechitu199233% (3)

- New Heritage Doll Company Student SpreadsheetDocument4 pagesNew Heritage Doll Company Student SpreadsheetGourav Agarwal73% (11)

- NHDC-Solution-xls Analisis VPN TIR NHDCDocument4 pagesNHDC-Solution-xls Analisis VPN TIR NHDCDaniel Infante0% (1)

- New Heritage DoolDocument9 pagesNew Heritage DoolVidya Sagar KonaNo ratings yet

- RESUELTO New Heritage Doll Company Student SpreadsheetDocument13 pagesRESUELTO New Heritage Doll Company Student SpreadsheetDaniel InfanteNo ratings yet

- New Heritage DollDocument26 pagesNew Heritage DollJITESH GUPTANo ratings yet

- Flash Memory, IncDocument16 pagesFlash Memory, Inckiller drama67% (3)

- Heritage Doll CompanyDocument11 pagesHeritage Doll CompanyDeep Dey0% (1)

- New Heritage Doll Capital BudgetingDocument9 pagesNew Heritage Doll Capital Budgetingpalmis20% (1)

- Flash - Memory - Inc From Website 0515Document8 pagesFlash - Memory - Inc From Website 0515竹本口木子100% (1)

- Online AnswerDocument4 pagesOnline AnswerYiru Pan100% (2)

- Flash Memory IncDocument7 pagesFlash Memory IncAbhinandan SinghNo ratings yet

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisTheicon420No ratings yet

- Finance - WK 4 Assignment TemplateDocument31 pagesFinance - WK 4 Assignment TemplateIsfandyar Junaid50% (2)

- Heritage Doll Company Project EvaluationDocument13 pagesHeritage Doll Company Project EvaluationSabyasachi Sahu100% (1)

- Flash Memory IncDocument9 pagesFlash Memory Incxcmalsk100% (1)

- Flash Memory Case SolutionDocument10 pagesFlash Memory Case SolutionsahilkuNo ratings yet

- FlashMemory SolnDocument8 pagesFlashMemory Solnchopra98harsh3311100% (4)

- Flash Memory IncDocument3 pagesFlash Memory IncAhsan IqbalNo ratings yet

- Mercury Athletic SlidesDocument28 pagesMercury Athletic SlidesTaimoor Shahzad100% (3)

- Friendly CS SolutionDocument8 pagesFriendly CS SolutionEfendiNo ratings yet

- Case - Flash Memory, Inc. - SolutionDocument11 pagesCase - Flash Memory, Inc. - SolutionBryan Meza71% (38)

- New Heritage DollDocument4 pagesNew Heritage Dolls_gonzalez75No ratings yet

- New Heritage Doll Company Capital BudgetDocument10 pagesNew Heritage Doll Company Capital BudgetIris Belen Medina OrozcoNo ratings yet

- Tarea Heritage Doll CompanyDocument6 pagesTarea Heritage Doll CompanyFelipe HidalgoNo ratings yet

- Heritage Dolls CaseDocument8 pagesHeritage Dolls Casearun jacobNo ratings yet

- Calculation My DollDocument2 pagesCalculation My Dollfitri0% (1)

- BHEL Valuation of CompanyDocument23 pagesBHEL Valuation of CompanyVishalNo ratings yet

- Mirr MMDC (3,020) (5,706) 11% 8.40 940 DYOD (5,331) (9,557) 10% 8.12 940 Initial Capex Add Capex Base Payback Base CaseDocument3 pagesMirr MMDC (3,020) (5,706) 11% 8.40 940 DYOD (5,331) (9,557) 10% 8.12 940 Initial Capex Add Capex Base Payback Base Casesd717No ratings yet

- Performance AGlanceDocument1 pagePerformance AGlanceHarshal SawaleNo ratings yet

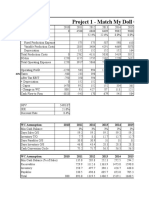

- Project 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015Document4 pagesProject 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015rohitNo ratings yet

- Revenue Production Costs: Initial ExpendituresDocument16 pagesRevenue Production Costs: Initial Expendituresajeetkumarverma 2k21dmba20No ratings yet

- Gildan Model BearDocument57 pagesGildan Model BearNaman PriyadarshiNo ratings yet

- Dersnot 1372 1684245035Document6 pagesDersnot 1372 1684245035Murat SiyahkayaNo ratings yet

- TCS RATIO Calulations-1Document4 pagesTCS RATIO Calulations-1reddynagendrapalle123No ratings yet

- Currently Factor Correlation Matrix Is Not Showing Up in Our CaseDocument1 pageCurrently Factor Correlation Matrix Is Not Showing Up in Our Casesanket vermaNo ratings yet

- Section B - Group 1 - CSR - Coca ColaDocument1 pageSection B - Group 1 - CSR - Coca Colasanket vermaNo ratings yet

- MIS ProjectDocument1 pageMIS Projectsanket vermaNo ratings yet

- Strategic Management - I: Porter'S 5 Forces ModelDocument4 pagesStrategic Management - I: Porter'S 5 Forces Modelsanket vermaNo ratings yet

- Group 1 - Section B - Corporate Finance ProjectDocument14 pagesGroup 1 - Section B - Corporate Finance Projectsanket vermaNo ratings yet

- Group4 SectionB iDreamReport PDFDocument15 pagesGroup4 SectionB iDreamReport PDFsanket vermaNo ratings yet

- Idream Education: Empowering With Data: Management Information Systems at Management Development Institute, GurgaonDocument8 pagesIdream Education: Empowering With Data: Management Information Systems at Management Development Institute, Gurgaonsanket vermaNo ratings yet

- MIS Project IdreamDocument11 pagesMIS Project Idreamsanket vermaNo ratings yet

- Idream Education: Empowering With Data: Management Information Systems at Management Development Institute, GurgaonDocument8 pagesIdream Education: Empowering With Data: Management Information Systems at Management Development Institute, Gurgaonsanket vermaNo ratings yet

- Mr. Mcclintock Can Analyse The Following Factors To Decide Whether or Not To Adopt Level Production PlanDocument10 pagesMr. Mcclintock Can Analyse The Following Factors To Decide Whether or Not To Adopt Level Production Plansanket vermaNo ratings yet

- Community Service Learning IdeasDocument4 pagesCommunity Service Learning IdeasMuneeb ZafarNo ratings yet

- Spice Processing UnitDocument3 pagesSpice Processing UnitKSHETRIMAYUM MONIKA DEVINo ratings yet

- Karnataka BankDocument6 pagesKarnataka BankS Vivek BhatNo ratings yet

- Economics and Agricultural EconomicsDocument28 pagesEconomics and Agricultural EconomicsM Hossain AliNo ratings yet

- The Future of Psychology Practice and Science PDFDocument15 pagesThe Future of Psychology Practice and Science PDFPaulo César MesaNo ratings yet

- Dumont's Theory of Caste.Document4 pagesDumont's Theory of Caste.Vikram Viner50% (2)

- Lindenberg-Anlagen GMBH: Stromerzeugungs-Und Pumpenanlagen SchaltanlagenDocument10 pagesLindenberg-Anlagen GMBH: Stromerzeugungs-Und Pumpenanlagen SchaltanlagenБогдан Кендзер100% (1)

- Astm D1895 17Document4 pagesAstm D1895 17Sonia Goncalves100% (1)

- Pasahol-Bsa1-Rizal AssignmentDocument4 pagesPasahol-Bsa1-Rizal AssignmentAngel PasaholNo ratings yet

- AMUL'S Every Function Involves Huge Human ResourcesDocument3 pagesAMUL'S Every Function Involves Huge Human ResourcesRitu RajNo ratings yet

- The Nature of Mathematics: "Nature's Great Books Is Written in Mathematics" Galileo GalileiDocument9 pagesThe Nature of Mathematics: "Nature's Great Books Is Written in Mathematics" Galileo GalileiLei-Angelika TungpalanNo ratings yet

- Full Download Test Bank For Health Psychology Well Being in A Diverse World 4th by Gurung PDF Full ChapterDocument36 pagesFull Download Test Bank For Health Psychology Well Being in A Diverse World 4th by Gurung PDF Full Chapterbiscuitunwist20bsg4100% (18)

- 1-Gaikindo Category Data Jandec2020Document2 pages1-Gaikindo Category Data Jandec2020Tanjung YanugrohoNo ratings yet

- OptiX OSN 8800 6800 3800 Configuration Guide (V100R007)Document924 pagesOptiX OSN 8800 6800 3800 Configuration Guide (V100R007)vladNo ratings yet

- Financial Performance Report General Tyres and Rubber Company-FinalDocument29 pagesFinancial Performance Report General Tyres and Rubber Company-FinalKabeer QureshiNo ratings yet

- 2's Complement Division C++ ProgramDocument11 pages2's Complement Division C++ ProgramAjitabh Gupta100% (2)

- Brahm Dutt v. UoiDocument3 pagesBrahm Dutt v. Uoiswati mohapatraNo ratings yet

- Curriculum Vitae: Personal InformationDocument2 pagesCurriculum Vitae: Personal InformationtyasNo ratings yet

- TNEA Participating College - Cut Out 2017Document18 pagesTNEA Participating College - Cut Out 2017Ajith KumarNo ratings yet

- Food NutritionDocument21 pagesFood NutritionLaine AcainNo ratings yet

- HDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Document40 pagesHDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Sumit MalikNo ratings yet

- End of Semester Student SurveyDocument2 pagesEnd of Semester Student SurveyJoaquinNo ratings yet

- Quiz 07Document15 pagesQuiz 07Ije Love100% (1)

- Phylogenetic Tree: GlossaryDocument7 pagesPhylogenetic Tree: GlossarySab ka bada FanNo ratings yet

- Introduction To Emerging TechnologiesDocument145 pagesIntroduction To Emerging TechnologiesKirubel KefyalewNo ratings yet

- Result 1st Entry Test Held On 22-08-2021Document476 pagesResult 1st Entry Test Held On 22-08-2021AsifRiazNo ratings yet

- Aqualab ClinicDocument12 pagesAqualab ClinichonyarnamiqNo ratings yet

- Best Interior Architects in Kolkata PDF DownloadDocument1 pageBest Interior Architects in Kolkata PDF DownloadArsh KrishNo ratings yet

- Duterte Vs SandiganbayanDocument17 pagesDuterte Vs SandiganbayanAnonymous KvztB3No ratings yet

- Final Test General English TM 2021Document2 pagesFinal Test General English TM 2021Nenden FernandesNo ratings yet