You might also like

- Chapter 9 Test Risk ManagementDocument18 pagesChapter 9 Test Risk ManagementEymard Siojo0% (1)

- Chapter 10 Test Risk ManagementDocument15 pagesChapter 10 Test Risk ManagementNicole Labbao100% (2)

- Principles of Risk Management and Insurance Fundamental Legal ConceptsDocument18 pagesPrinciples of Risk Management and Insurance Fundamental Legal ConceptsNicole LabbaoNo ratings yet

- Analysis of Insurance ContractsDocument6 pagesAnalysis of Insurance ContractsAhmad Sabah100% (1)

- Principles of Risk Management and Insurance, 13E, Global Edition (Rejda/Mcnamara)Document11 pagesPrinciples of Risk Management and Insurance, 13E, Global Edition (Rejda/Mcnamara)Ra'fat Jallad100% (1)

- Excercise Questions - Part 1 - With AnswerDocument8 pagesExcercise Questions - Part 1 - With AnswerFelicia VpNo ratings yet

- Agent Question BankDocument47 pagesAgent Question BankshinukrajanNo ratings yet

- Principles of Insurance (Chapter - Unit 2) Solved MCQs (Set-1)Document5 pagesPrinciples of Insurance (Chapter - Unit 2) Solved MCQs (Set-1)ANURAGNo ratings yet

- Ch. 2 Test Bank - InsuranceDocument8 pagesCh. 2 Test Bank - InsuranceAhmed NaserNo ratings yet

- HTTP DR - FarkasszilveszterDocument40 pagesHTTP DR - FarkasszilveszterGud Man75% (4)

- Edition-by-Dorfman: Complete Downloadable File atDocument13 pagesEdition-by-Dorfman: Complete Downloadable File ataafnanNo ratings yet

- Test Bank For Introduction To Risk Management and Insurance 10th Edition by Dorfman Download 190327020242Document24 pagesTest Bank For Introduction To Risk Management and Insurance 10th Edition by Dorfman Download 190327020242Hasan Bin HusainNo ratings yet

- Principles of Risk Management and Insurance Chapter 1 Key ConceptsDocument11 pagesPrinciples of Risk Management and Insurance Chapter 1 Key ConceptsAhmed NaserNo ratings yet

- Introduction To Risk Management: Question Status: Previous EditionDocument7 pagesIntroduction To Risk Management: Question Status: Previous EditionSylvia Al-a'maNo ratings yet

- Risk Management and Insurance Solved MCQs Set 3Document7 pagesRisk Management and Insurance Solved MCQs Set 3Gauresh NaikNo ratings yet

- Chapter 3 ChooseDocument15 pagesChapter 3 ChooseHamadaAttiaNo ratings yet

- MCQ Re-InsuranceDocument1 pageMCQ Re-InsuranceAMIT BHATIA100% (2)

- Multiple Choice Questions: Answer: B. Wealth MaximisationDocument20 pagesMultiple Choice Questions: Answer: B. Wealth MaximisationArchana Neppolian100% (1)

- MCQ Financial Accounting II PDFDocument23 pagesMCQ Financial Accounting II PDFSurya ShekharNo ratings yet

- Department of Business Administration 16 UBM 515 - Insurance Principles and Practices Multiple Choice Questions Unit-IDocument18 pagesDepartment of Business Administration 16 UBM 515 - Insurance Principles and Practices Multiple Choice Questions Unit-IAman SharmaNo ratings yet

- ch4TB PDFDocument8 pagesch4TB PDFChan Man Hin0% (2)

- All HWsDocument109 pagesAll HWsGhala Alk100% (1)

- Chapter 21Document13 pagesChapter 21kennyNo ratings yet

- MCQ Bcom II Principles of Insurance 1 PDFDocument16 pagesMCQ Bcom II Principles of Insurance 1 PDFNaïlêñ Trïpūrå Jr.100% (1)

- Financial Management MCQDocument31 pagesFinancial Management MCQR.ARULNo ratings yet

- Multiple Choice Questions: Marginal CostingDocument6 pagesMultiple Choice Questions: Marginal CostingSatyam JainNo ratings yet

- Sample Exam QuestionsDocument6 pagesSample Exam QuestionsTôn Nữ Hương Giang100% (1)

- Life and Health Insurance ChapterDocument29 pagesLife and Health Insurance ChapterWonde BiruNo ratings yet

- WCM Finance MCQDocument28 pagesWCM Finance MCQMosam AliNo ratings yet

- Financial Management MCQs 35: Maximizing Firm ValueDocument6 pagesFinancial Management MCQs 35: Maximizing Firm Valuekhan50% (2)

- Financial Management MCQsDocument11 pagesFinancial Management MCQsmadihaadnan150% (2)

- Financial Statement Analysis MCQs With AnswerDocument5 pagesFinancial Statement Analysis MCQs With AnswerHamza Khan YousafzaiNo ratings yet

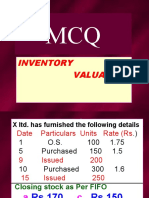

- MCQ Inventory Valuation LBSIMDocument49 pagesMCQ Inventory Valuation LBSIMSumit SharmaNo ratings yet

- (Risk Management and Insurance 1) Exam Questions Code 3Document3 pages(Risk Management and Insurance 1) Exam Questions Code 3trang100% (1)

- Chapter 9 Test Risk ManagementDocument6 pagesChapter 9 Test Risk Managementxdivanxd67% (3)

- Risk Management & Insurance QuizDocument2 pagesRisk Management & Insurance QuizApdy Aziiz Daahir100% (1)

- Objective Questions and Answers of Financial ManagementDocument22 pagesObjective Questions and Answers of Financial ManagementGhulam MustafaNo ratings yet

- Test Bank For Principles of Risk Management and Insurance 12th Edition by RejdaDocument10 pagesTest Bank For Principles of Risk Management and Insurance 12th Edition by Rejdajames90% (10)

- MCQ in Risk ManagementDocument7 pagesMCQ in Risk ManagementPrakriti ThapaNo ratings yet

- Banking and Finance Module 4 - Insurance QuestionsDocument5 pagesBanking and Finance Module 4 - Insurance Questionsdivya100% (1)

- LEASE ACC - MCQ - FY B Com-converted-F10022vo3rON9mO0DtNs-COU20200917082041uFV-1810Document8 pagesLEASE ACC - MCQ - FY B Com-converted-F10022vo3rON9mO0DtNs-COU20200917082041uFV-1810Vineet KrNo ratings yet

- 250 Question Insurance LawDocument43 pages250 Question Insurance LawShivansh MishraNo ratings yet

- CVP ActivityDocument7 pagesCVP ActivityANSLEY CATE C. GUEVARRANo ratings yet

- Cost Accounting McqsDocument11 pagesCost Accounting McqsJanani Priya0% (1)

- Chapter 3 Introduction To Risk Management NewDocument7 pagesChapter 3 Introduction To Risk Management NewDanielLam83% (6)

- Insurance Claim AccountDocument12 pagesInsurance Claim AccountKadam Kartikesh50% (2)

- REDEMPTION OF SHARES & DEBENTURES MCQsDocument7 pagesREDEMPTION OF SHARES & DEBENTURES MCQsChetan StoresNo ratings yet

- A) Strategic ManagementDocument67 pagesA) Strategic ManagementRajat JazziNo ratings yet

- Multiple Choice QuestionsDocument20 pagesMultiple Choice QuestionsHenryNo ratings yet

- Amalgamation, Absorption & External Reconstruction: Chapter-IDocument15 pagesAmalgamation, Absorption & External Reconstruction: Chapter-Ibharat wankhedeNo ratings yet

- B&a - MCQDocument11 pagesB&a - MCQAniket PuriNo ratings yet

- FM CH 3Document18 pagesFM CH 3samuel kebedeNo ratings yet

- Security Analysis & Portfolio Management (MCQ, S & Short Answers)Document54 pagesSecurity Analysis & Portfolio Management (MCQ, S & Short Answers)Hamid Ilyas80% (10)

- Cost Sem 5 ObjectiveDocument16 pagesCost Sem 5 Objectivesimran Keswani0% (1)

- Pages 55 Capital Market Operation FinalDocument38 pagesPages 55 Capital Market Operation FinalAakash SharmaNo ratings yet

- QUESTION One (Multiple Choice) : Insurance Company OperationsDocument14 pagesQUESTION One (Multiple Choice) : Insurance Company Operationsmamush fikaduNo ratings yet

- Principles of Risk Management and Insurance 11th Edition Rejda Test BankDocument10 pagesPrinciples of Risk Management and Insurance 11th Edition Rejda Test Bankhelenglendacduf100% (22)

- Principles of Risk Management and Insurance 12th Edition Rejda Test BankDocument13 pagesPrinciples of Risk Management and Insurance 12th Edition Rejda Test Bankcleopatrabanhft1vh7100% (27)

- Principles of Risk Management and Insurance 12Th Edition Rejda Test Bank Full Chapter PDFDocument34 pagesPrinciples of Risk Management and Insurance 12Th Edition Rejda Test Bank Full Chapter PDFJasonMoralesykcx100% (7)

- Cum in MeDocument11 pagesCum in MeJohn DoeNo ratings yet

- 6.5 Measures of Relative PositionDocument2 pages6.5 Measures of Relative PositionAmeer ElatmaNo ratings yet

- History of InsuranceDocument36 pagesHistory of InsuranceMurali DharanNo ratings yet

- 10 - Chapter 1 PDFDocument65 pages10 - Chapter 1 PDFAyushi MahadikNo ratings yet

- History of InsuranceDocument36 pagesHistory of InsuranceMurali DharanNo ratings yet

- Intro To Insurance Overheads043004Document22 pagesIntro To Insurance Overheads043004Rajesh JatavNo ratings yet

- ExamRevision2012 With Answers 2Document30 pagesExamRevision2012 With Answers 2Ameer ElatmaNo ratings yet

- 6.5 Measures of Relative PositionDocument2 pages6.5 Measures of Relative PositionAmeer ElatmaNo ratings yet

- Insurance Verification and Fee Transparency for PatientsDocument23 pagesInsurance Verification and Fee Transparency for PatientsAmeer ElatmaNo ratings yet

- Insurance Verification and Fee Transparency for PatientsDocument23 pagesInsurance Verification and Fee Transparency for PatientsAmeer ElatmaNo ratings yet

- 5.4 Line Integrals: Quantity Intensity Per Unit LengthDocument4 pages5.4 Line Integrals: Quantity Intensity Per Unit LengthAmeer ElatmaNo ratings yet

- CH 17Document24 pagesCH 17Ameer ElatmaNo ratings yet

- Chemistry Exam (Chapters 1,2,3&7), The Exam Will Be Allowed Friday 1222020 (6PM 9PM), Edit by Eng. Sayed YousefDocument1 pageChemistry Exam (Chapters 1,2,3&7), The Exam Will Be Allowed Friday 1222020 (6PM 9PM), Edit by Eng. Sayed YousefAmeer ElatmaNo ratings yet

- History of InsuranceDocument36 pagesHistory of InsuranceMurali DharanNo ratings yet

- Integration by InspectionDocument10 pagesIntegration by InspectionAmeer ElatmaNo ratings yet

- Statistical Techniques in Business & Q Economics: Professor: Mamdouh Hamza AhmedDocument16 pagesStatistical Techniques in Business & Q Economics: Professor: Mamdouh Hamza AhmedAmeer ElatmaNo ratings yet

- BA 302 Stats SyllabusDocument6 pagesBA 302 Stats SyllabusAmeer ElatmaNo ratings yet

- Chapter 6 17Document6 pagesChapter 6 17Ameer ElatmaNo ratings yet

- Fundamental Legal Principles of Insurance Contract: QUESTION One (Multiple Choice)Document13 pagesFundamental Legal Principles of Insurance Contract: QUESTION One (Multiple Choice)Ameer Elatma100% (1)

- Design The CurriculumDocument14 pagesDesign The CurriculumYusran AzizNo ratings yet

- 11.work Ethics & Loyalty - PPSX PDFDocument24 pages11.work Ethics & Loyalty - PPSX PDFAngrez SinghNo ratings yet

- Introduction To Literature and Literary Devices: Lesson ProperDocument7 pagesIntroduction To Literature and Literary Devices: Lesson ProperAngel NacenoNo ratings yet

- Cabbage Hybrid Seed ProductionDocument55 pagesCabbage Hybrid Seed ProductionDivya Dharshini VNo ratings yet

- Greaves Cotton Non-Automotive Engines for Agriculture, Construction, Marine and Industrial ApplicationsDocument6 pagesGreaves Cotton Non-Automotive Engines for Agriculture, Construction, Marine and Industrial ApplicationsRicardo TurlaNo ratings yet

- The Effectiveness of EMP and EFP: An IS-LM-BP AnalysisDocument10 pagesThe Effectiveness of EMP and EFP: An IS-LM-BP AnalysisNurul FatihahNo ratings yet

- Pangasinan State UniversityDocument25 pagesPangasinan State UniversityAnna Marie Ventayen MirandaNo ratings yet

- Maharaja Soaps industries profileDocument41 pagesMaharaja Soaps industries profileVenki GajaNo ratings yet

- Activity Proposal For Nutrition Month Celebration 2018Document4 pagesActivity Proposal For Nutrition Month Celebration 2018Cherly Pangadlin Deroca-Gaballo100% (2)

- Elkay ManufacturingDocument5 pagesElkay ManufacturingAbhishek Kumar SinghNo ratings yet

- Inhibition in Speaking Ability of Fifth Semester Students in Class 2 of English Department at Tidar UniversityDocument5 pagesInhibition in Speaking Ability of Fifth Semester Students in Class 2 of English Department at Tidar UniversityAzizi AziziNo ratings yet

- CPWD RatesDocument197 pagesCPWD RatespnkjinamdarNo ratings yet

- Delhi Public School Ghatkesar Friday: Daily Time TableDocument1 pageDelhi Public School Ghatkesar Friday: Daily Time TableranjithophirNo ratings yet

- Royal Rangers Gold Merit RequirementsDocument27 pagesRoyal Rangers Gold Merit Requirementsccm2361No ratings yet

- Bus Org NotesDocument37 pagesBus Org NotesHonorio Bartholomew ChanNo ratings yet

- Chapter 3.12 - Winding UpDocument21 pagesChapter 3.12 - Winding UpDashania GregoryNo ratings yet

- IT Governance MCQDocument3 pagesIT Governance MCQHazraphine Linso63% (8)

- Romance Short S-WPS OfficeDocument4 pagesRomance Short S-WPS OfficeNidya putriNo ratings yet

- Key Trends Affecting Pharmacy AdministrationDocument5 pagesKey Trends Affecting Pharmacy AdministrationPeter NdiraguNo ratings yet

- MV SSI BRILLIANT Daily Report 04 - 12.11.2023Document16 pagesMV SSI BRILLIANT Daily Report 04 - 12.11.2023DanielNo ratings yet

- Ertyuikjrewdefthyjhertyujkreytyjthm VCDocument2 pagesErtyuikjrewdefthyjhertyujkreytyjthm VCCedrick Jasper SanglapNo ratings yet

- Deped Community MappingDocument1 pageDeped Community MappingDorothy Jean100% (2)

- CBT TestDocument18 pagesCBT TestJulieBarrieNo ratings yet

- 2014 Lancaster-Lebanon League High School Football PreviewDocument48 pages2014 Lancaster-Lebanon League High School Football PreviewLNP MEDIA GROUP, Inc.No ratings yet

- Dere Ham Booklet LoresDocument33 pagesDere Ham Booklet Loresbookworm2830No ratings yet

- UEE NotesDocument40 pagesUEE NotesSmarty KalyanNo ratings yet

- UE Muscles OINADocument3 pagesUE Muscles OINAUshuaia Chely FilomenoNo ratings yet

- Veritas Command Line SyntaxDocument6 pagesVeritas Command Line SyntaxSalma KhatoonNo ratings yet

- Guide To Securing Microsoft Windows XP (NSA)Document141 pagesGuide To Securing Microsoft Windows XP (NSA)prof_ktNo ratings yet

- C-Data Epon Olt Fd1108s Cli User Manual v1.3Document89 pagesC-Data Epon Olt Fd1108s Cli User Manual v1.3sarasa100% (2)