You might also like

- Juris NotesDocument41 pagesJuris NotesSaha80% (5)

- Mano Marz Ul MautDocument12 pagesMano Marz Ul Mautdynamo vjNo ratings yet

- Jurisprudence Notes Ronald Dworkin'S InterpretivismDocument40 pagesJurisprudence Notes Ronald Dworkin'S Interpretivismdynamo vjNo ratings yet

- General Defences Under Law of TortsDocument14 pagesGeneral Defences Under Law of Tortsdynamo vjNo ratings yet

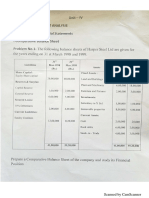

- Cost and Management Accounting Question Ban1Document3 pagesCost and Management Accounting Question Ban1dynamo vjNo ratings yet

- Police Administration DelhiDocument1 pagePolice Administration Delhidynamo vjNo ratings yet

- Questions CA Unit 4-5Document17 pagesQuestions CA Unit 4-5dynamo vjNo ratings yet

- Accounts For Banking BusinessDocument2 pagesAccounts For Banking BusinessgowthamNo ratings yet

- Family LawDocument140 pagesFamily Lawdynamo vjNo ratings yet

- Unit - III Labour CostDocument38 pagesUnit - III Labour CosttheriyathuNo ratings yet

- Internship Diary ManoDocument13 pagesInternship Diary Manodynamo vj100% (4)

- Family Law - Ii Notes Indian Succession Act, 1925Document80 pagesFamily Law - Ii Notes Indian Succession Act, 1925dynamo vj100% (2)

- Ios BibloDocument2 pagesIos Biblodynamo vjNo ratings yet

- Admissability of Forensic Evidences in Rape CasesDocument3 pagesAdmissability of Forensic Evidences in Rape Casesdynamo vjNo ratings yet

- Consortium of National Law Universities: Permanent Secretariat Nlsiu, Nagarbhavi, Bangalore - 560 072Document1 pageConsortium of National Law Universities: Permanent Secretariat Nlsiu, Nagarbhavi, Bangalore - 560 072dynamo vjNo ratings yet

- Ios BibloDocument2 pagesIos Biblodynamo vjNo ratings yet

- Green (R) Evolution Global Program Exam Guide: Online Mode (Recommended) : FreeDocument1 pageGreen (R) Evolution Global Program Exam Guide: Online Mode (Recommended) : FreeGaurvi AroraNo ratings yet

- Ios BibloDocument2 pagesIos Biblodynamo vjNo ratings yet

- UG TamilNaduNationalLawUniversityTNNLUTiruchirappalliDocument7 pagesUG TamilNaduNationalLawUniversityTNNLUTiruchirappallidynamo vjNo ratings yet

- SCHEDULE (17th March)Document2 pagesSCHEDULE (17th March)dynamo vjNo ratings yet

- Consortium of National Law Universities: Provisional 2nd List - CLAT 2019 - PGDocument2 pagesConsortium of National Law Universities: Provisional 2nd List - CLAT 2019 - PGdynamo vjNo ratings yet

- SCHEDULE (17th March)Document2 pagesSCHEDULE (17th March)dynamo vjNo ratings yet

- Indian Income Tax Act 2008Document1,065 pagesIndian Income Tax Act 2008ananthca100% (2)

- SecondCutoffMarks5YrHons2019 20Document1 pageSecondCutoffMarks5YrHons2019 20dynamo vjNo ratings yet

- Personal Data Protection Bill, 2018Document67 pagesPersonal Data Protection Bill, 2018Latest Laws TeamNo ratings yet

- Harshit Saxena - Lifting The Corporate VeilDocument24 pagesHarshit Saxena - Lifting The Corporate VeilHimanshu MishraNo ratings yet

- Estimated 2-Day Event Budget Rs. 40,000Document1 pageEstimated 2-Day Event Budget Rs. 40,000dynamo vjNo ratings yet

- Majority opinion declares instant triple talaq unconstitutionalDocument1 pageMajority opinion declares instant triple talaq unconstitutionaldynamo vjNo ratings yet

- Compeition RulesDocument1 pageCompeition Rulesdynamo vjNo ratings yet

- 11 TaxDocument37 pages11 TaxArpita KapoorNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Biography Nelson MandelaDocument4 pagesBiography Nelson MandelaBunga ChanNo ratings yet

- R V Jordan NotesDocument3 pagesR V Jordan NotesVenus WangNo ratings yet

- Atilano II vs. AsaaliDocument7 pagesAtilano II vs. AsaaliRamil GarciaNo ratings yet

- People vs Cagoco - Murder conviction upheld for fatal blow to victim's headDocument72 pagesPeople vs Cagoco - Murder conviction upheld for fatal blow to victim's headGerard Anthony Teves RosalesNo ratings yet

- Calendar - 2016 08 12Document2 pagesCalendar - 2016 08 12Elden Cunanan BonillaNo ratings yet

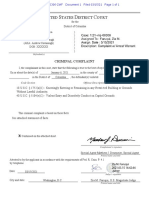

- USA Vs Andrew CavanaughDocument1 pageUSA Vs Andrew CavanaughNBC MontanaNo ratings yet

- Nariman Submission 4Document66 pagesNariman Submission 4Live LawNo ratings yet

- IEI Is Statutory-Court JudgmentDocument8 pagesIEI Is Statutory-Court JudgmentErRajivAmieNo ratings yet

- Certificate of Candidacy SGODocument2 pagesCertificate of Candidacy SGObernardNo ratings yet

- People Vs CA and Maquiling (Re GAD)Document13 pagesPeople Vs CA and Maquiling (Re GAD)Vern CastilloNo ratings yet

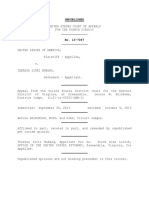

- United States v. Theresa Mubang, 4th Cir. (2013)Document3 pagesUnited States v. Theresa Mubang, 4th Cir. (2013)Scribd Government DocsNo ratings yet

- Not PrecedentialDocument9 pagesNot PrecedentialScribd Government DocsNo ratings yet

- Rajesh V Choudhary Vs Kshitij Rajiv Torka and OrsMH201519091519125799COM279936Document23 pagesRajesh V Choudhary Vs Kshitij Rajiv Torka and OrsMH201519091519125799COM279936Shubhangi SinghNo ratings yet

- Ministry of Civil Aviation Security RulesDocument13 pagesMinistry of Civil Aviation Security RulesshombisNo ratings yet

- CASE #91 Republic of The Philippines vs. Alvin Dimarucot and Nailyn Tañedo-Dimarucot G.R. No. 202069, March 7, 2018 FactsDocument2 pagesCASE #91 Republic of The Philippines vs. Alvin Dimarucot and Nailyn Tañedo-Dimarucot G.R. No. 202069, March 7, 2018 FactsHarleneNo ratings yet

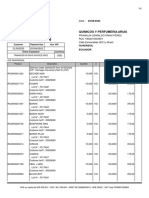

- Factura ComercialDocument6 pagesFactura ComercialKaren MezaNo ratings yet

- Roman Catholic v. CA (1991)Document2 pagesRoman Catholic v. CA (1991)Nap GonzalesNo ratings yet

- People Vs Degamo April 30 2003Document2 pagesPeople Vs Degamo April 30 2003Vance CeballosNo ratings yet

- Bangladesh's Environment Court System Needs ReformDocument22 pagesBangladesh's Environment Court System Needs ReformNazmoon NaharNo ratings yet

- GST ChallanDocument1 pageGST ChallanAshish VishnoiNo ratings yet

- Maloles Vs Phillips, CADocument14 pagesMaloles Vs Phillips, CAMariz D.R.No ratings yet

- Francisco Vs TRBDocument3 pagesFrancisco Vs TRBFranz KafkaNo ratings yet

- Strict LiabilityDocument11 pagesStrict LiabilityMWAKISIKI MWAKISIKI EDWARDSNo ratings yet

- Vakalatnama Supreme CourtDocument2 pagesVakalatnama Supreme CourtSiddharth Chitturi80% (5)

- KP Law BROCHUREDocument7 pagesKP Law BROCHUREIvan_jaydee100% (1)

- Customs Seizure of Ships UpheldDocument2 pagesCustoms Seizure of Ships UpheldFgmtNo ratings yet

- Red Tape Report: Behind The Scenes of The Section 8 Housing ProgramDocument7 pagesRed Tape Report: Behind The Scenes of The Section 8 Housing ProgramBill de BlasioNo ratings yet

- RFP - Visa OutsourcingDocument12 pagesRFP - Visa OutsourcingromsbhojakNo ratings yet

- Petitioners Respondent Atty. Noe Q. Laguindam Atty. Elpidio I. DigaumDocument11 pagesPetitioners Respondent Atty. Noe Q. Laguindam Atty. Elpidio I. DigaumRomy IanNo ratings yet

- Appeal To High Court Under Code of Civil ProcedureDocument2 pagesAppeal To High Court Under Code of Civil ProcedureShelly SachdevNo ratings yet