You might also like

- Paper & Paper Product Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandPaper & Paper Product Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- CPRT Us Equity - Model - ZCK - Mar 15 2023Document23 pagesCPRT Us Equity - Model - ZCK - Mar 15 2023Ekambaram Thirupalli TNo ratings yet

- Outboard Engines World Summary: Market Sector Values & Financials by CountryFrom EverandOutboard Engines World Summary: Market Sector Values & Financials by CountryNo ratings yet

- YES Bank Presentation Q42018Document32 pagesYES Bank Presentation Q42018sanjeev7777No ratings yet

- Apparel, Piece Goods & Notions Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandApparel, Piece Goods & Notions Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- CLEducateLimited PDFDocument30 pagesCLEducateLimited PDFhamsNo ratings yet

- Shalby Limited BSE 540797 FinancialsDocument51 pagesShalby Limited BSE 540797 Financialsakumar4uNo ratings yet

- Stmicro - Q4-Fy2018 PR - FinalDocument12 pagesStmicro - Q4-Fy2018 PR - Finalakshay kumarNo ratings yet

- Creative Enterprise Holdings Limited SEHK 3992 FinancialsDocument32 pagesCreative Enterprise Holdings Limited SEHK 3992 FinancialsxunstandupNo ratings yet

- Earnings Release (FY22 Q3) FINALDocument12 pagesEarnings Release (FY22 Q3) FINALIra BanksNo ratings yet

- Pepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsDocument28 pagesPepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsJulio CesarNo ratings yet

- Shalby Limited BSE 540797 FinancialsDocument39 pagesShalby Limited BSE 540797 Financialsakumar4uNo ratings yet

- Task 1 BigTech TemplateDocument5 pagesTask 1 BigTech Templatedaniyalansari.8425No ratings yet

- BOLT DCF ValuationDocument1 pageBOLT DCF ValuationOld School ValueNo ratings yet

- $ in Millions, Except Per Share DataDocument59 pages$ in Millions, Except Per Share DataTom HoughNo ratings yet

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocument10 pagesInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook SittiwatNo ratings yet

- Apollo Hospitals Enterprise Limited NSEI APOLLOHOSP FinancialsDocument40 pagesApollo Hospitals Enterprise Limited NSEI APOLLOHOSP Financialsakumar4uNo ratings yet

- Q1 2020-21 Fact Sheet PDFDocument27 pagesQ1 2020-21 Fact Sheet PDFJose CANo ratings yet

- Quarterly Results 2010-11: HCL TechnologiesDocument31 pagesQuarterly Results 2010-11: HCL Technologies13lackhatNo ratings yet

- Analisis FinancieroDocument124 pagesAnalisis FinancieroJesús VelázquezNo ratings yet

- 10 Ways To Use A Cascade Chart: David Goldstein February 2020Document14 pages10 Ways To Use A Cascade Chart: David Goldstein February 2020JohnNo ratings yet

- FIN439 - CokeTemplate - TOWSON UNIVERSITYDocument35 pagesFIN439 - CokeTemplate - TOWSON UNIVERSITYJose RuizNo ratings yet

- BofA Q1 2019Document29 pagesBofA Q1 2019ZerohedgeNo ratings yet

- 2021-01-21_Intel_Reports_Fourth_Quarter_and_Full_Year_2020_1439Document17 pages2021-01-21_Intel_Reports_Fourth_Quarter_and_Full_Year_2020_1439samuel.p.collingsNo ratings yet

- Class Exercise Fashion Company Three Statements Model - CompletedDocument16 pagesClass Exercise Fashion Company Three Statements Model - CompletedbobNo ratings yet

- 4Q23 Mastercard Earnings ReleaseDocument15 pages4Q23 Mastercard Earnings ReleaseFashina RashidatNo ratings yet

- QUESTIONSDocument19 pagesQUESTIONSrahidarzooNo ratings yet

- Johnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueDocument12 pagesJohnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueOld School Value100% (2)

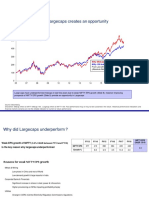

- Equity Markets Review Underperformance of Largecaps Creates An OpportunityDocument8 pagesEquity Markets Review Underperformance of Largecaps Creates An OpportunitysumeetNo ratings yet

- Rosetta Stone FinancialsDocument2 pagesRosetta Stone FinancialsAvaSeaveNo ratings yet

- LBO Completed ModelDocument210 pagesLBO Completed ModelBrian DongNo ratings yet

- Starbucks Coffee Company: Oppenheimer Consumer, Gaming, Lodging and Leisure Conference June 30, 2010Document29 pagesStarbucks Coffee Company: Oppenheimer Consumer, Gaming, Lodging and Leisure Conference June 30, 2010jphillips267No ratings yet

- Varanium 11042019Document25 pagesVaranium 11042019Rahul JainNo ratings yet

- Straco Corporation Limited SGX S85 FinancialsDocument80 pagesStraco Corporation Limited SGX S85 FinancialsP.RaviNo ratings yet

- Illustrative LBO AnalysisDocument21 pagesIllustrative LBO AnalysisBrian DongNo ratings yet

- Enph EstimacionDocument38 pagesEnph EstimacionPablo Alejandro JaldinNo ratings yet

- LBO (Leveraged Buyout) Model For Private Equity FirmsDocument2 pagesLBO (Leveraged Buyout) Model For Private Equity FirmsDishant KhanejaNo ratings yet

- TCS Financial Results: Quarter III FY 2021-22Document25 pagesTCS Financial Results: Quarter III FY 2021-22Arindam MukhopadhyayNo ratings yet

- Economic Indicators of PakistanDocument4 pagesEconomic Indicators of PakistanhellosaadyNo ratings yet

- Varma Capitals - Modeling TestDocument6 pagesVarma Capitals - Modeling TestSuper FreakNo ratings yet

- DCF Textbook Model ExampleDocument6 pagesDCF Textbook Model ExamplePeterNo ratings yet

- Tax BudgetDocument31 pagesTax BudgetJim ParkerNo ratings yet

- Jollibee Foods Corporation PSE JFC FinancialsDocument38 pagesJollibee Foods Corporation PSE JFC FinancialsJasper Andrew AdjaraniNo ratings yet

- Q3 2022 Earnings Release SnowDocument14 pagesQ3 2022 Earnings Release SnowCode BeretNo ratings yet

- Prataap Snacks DCF Valuation Upside CaseDocument41 pagesPrataap Snacks DCF Valuation Upside CaseCharanjitNo ratings yet

- MONDE - 17C 9M23 Briefing Materials - 8 November 2023Document34 pagesMONDE - 17C 9M23 Briefing Materials - 8 November 2023judy jace thaddeus AlejoNo ratings yet

- Parsons 2019Document150 pagesParsons 2019Ayman FatimaNo ratings yet

- GD 4Q21 Earnings Highlights-and-Outlook-FinalDocument13 pagesGD 4Q21 Earnings Highlights-and-Outlook-Finals95qgd9rmjNo ratings yet

- Canara Bank (NSEI:CANBK) Financials Key StatsDocument34 pagesCanara Bank (NSEI:CANBK) Financials Key StatsLekhnarayan ThakurNo ratings yet

- FY 2017 PresentationDocument30 pagesFY 2017 PresentationtheredcornerNo ratings yet

- First Quarter 2021 Earnings Conference Call May 3, 2021Document20 pagesFirst Quarter 2021 Earnings Conference Call May 3, 2021LisaNo ratings yet

- Angiodynamics: Fourth Quarter 2018 Earnings Presentation July 11, 2018Document10 pagesAngiodynamics: Fourth Quarter 2018 Earnings Presentation July 11, 2018medtechyNo ratings yet

- India@2030 - Mohandas Pai (Final) PDFDocument52 pagesIndia@2030 - Mohandas Pai (Final) PDFSunil KumarNo ratings yet

- LG Electronics 4Q'19 Earnings ReleaseDocument19 pagesLG Electronics 4Q'19 Earnings ReleaseОverlord 4No ratings yet

- 9M16 Results Beat Forecast On Higher Than Expected Revenues: Share DataDocument3 pages9M16 Results Beat Forecast On Higher Than Expected Revenues: Share DataJajahinaNo ratings yet

- UPL Limited BSE 512070 Financials RatiosDocument5 pagesUPL Limited BSE 512070 Financials RatiosRehan TyagiNo ratings yet

- Adani Power Limited NSEI ADANIPOWER FinancialsDocument34 pagesAdani Power Limited NSEI ADANIPOWER FinancialsSHAMBHAVI GUPTANo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- Planilha de Gerenciamento de Risco e RentabilidadeDocument6 pagesPlanilha de Gerenciamento de Risco e RentabilidadeBEACH SCUBA DETECTINGNo ratings yet

- NVDA F3Q23 Investor Presentation FINALDocument62 pagesNVDA F3Q23 Investor Presentation FINALandre.torresNo ratings yet

- Nasdaq Testimony 12 6 2019 Fin Tech Task Force AI Hearing FinalDocument9 pagesNasdaq Testimony 12 6 2019 Fin Tech Task Force AI Hearing FinaltabbforumNo ratings yet

- AP Cut Through The Hype Nov 2018Document10 pagesAP Cut Through The Hype Nov 2018tabbforum100% (1)

- Elm 02 20 2020Document6 pagesElm 02 20 2020tabbforumNo ratings yet

- ESMA and Market Data FeesDocument6 pagesESMA and Market Data FeestabbforumNo ratings yet

- V16-045 The Tool Beyond The ToolDocument21 pagesV16-045 The Tool Beyond The TooltabbforumNo ratings yet

- Original 2018-11 Equities LiquidityMatrix November 2018 v2Document21 pagesOriginal 2018-11 Equities LiquidityMatrix November 2018 v2tabbforumNo ratings yet

- V17-045 Institutionalizing CryptoDocument23 pagesV17-045 Institutionalizing CryptotabbforumNo ratings yet

- V17-061 Structured Solutions Using Options On FuturesDocument3 pagesV17-061 Structured Solutions Using Options On FuturestabbforumNo ratings yet

- V17-059 Bond Market AutomationDocument12 pagesV17-059 Bond Market AutomationtabbforumNo ratings yet

- V17-006 The Multi-Asset Buy Side Overkill or Table Stakes FinalDocument4 pagesV17-006 The Multi-Asset Buy Side Overkill or Table Stakes Finaltabbforum100% (1)

- Volcker 2.0 CadwaladerDocument12 pagesVolcker 2.0 CadwaladertabbforumNo ratings yet

- Numerix White Paper: The 5 Top-of-Mind Issues Dominating The LIBOR TransitionDocument5 pagesNumerix White Paper: The 5 Top-of-Mind Issues Dominating The LIBOR TransitiontabbforumNo ratings yet

- BMLL Technologies - LSE - Outage - MTF-LiquidityDocument8 pagesBMLL Technologies - LSE - Outage - MTF-LiquiditytabbforumNo ratings yet

- Larry Tabb Cboe LPP Comment Letter July 2019Document6 pagesLarry Tabb Cboe LPP Comment Letter July 2019tabbforumNo ratings yet

- Street Contxt Benchmark Report Q4 2018Document15 pagesStreet Contxt Benchmark Report Q4 2018tabbforumNo ratings yet

- Street Contxt Benchmark Report Q3-2018Document16 pagesStreet Contxt Benchmark Report Q3-2018tabbforumNo ratings yet

- 2018 RegTech Report FINRADocument13 pages2018 RegTech Report FINRAtabbforumNo ratings yet

- Cryptocompare Cryptoasset Taxonomy Report 2018Document79 pagesCryptocompare Cryptoasset Taxonomy Report 2018tabbforumNo ratings yet

- V16-043 Know Your Options - Options On Futures As Strategic Investment Vehicles v2Document17 pagesV16-043 Know Your Options - Options On Futures As Strategic Investment Vehicles v2tabbforumNo ratings yet

- Cross-Border Swaps Regulation - CFTC.10.1.18Document110 pagesCross-Border Swaps Regulation - CFTC.10.1.18tabbforumNo ratings yet

- Making The Connection: The Electronic Shift in Legacy Bond Market WorkflowDocument13 pagesMaking The Connection: The Electronic Shift in Legacy Bond Market WorkflowtabbforumNo ratings yet

- V16-044 Panacea or PipedreamDocument17 pagesV16-044 Panacea or PipedreamtabbforumNo ratings yet

- Greenwich Associates Bond Etf Study 2018Document8 pagesGreenwich Associates Bond Etf Study 2018tabbforumNo ratings yet

- MMI - FTT Study.9.18Document11 pagesMMI - FTT Study.9.18tabbforumNo ratings yet

- TABB - Future of Investment Banking.10.2008Document34 pagesTABB - Future of Investment Banking.10.2008tabbforumNo ratings yet

- NumerixWhitePaper Adapting To Change in The Electronic Fixed Income and OTC Markets Sept18 FinalDocument6 pagesNumerixWhitePaper Adapting To Change in The Electronic Fixed Income and OTC Markets Sept18 FinaltabbforumNo ratings yet

- 2018-08-13 AxiomSL - Return On Data InvestmentDocument13 pages2018-08-13 AxiomSL - Return On Data Investmenttabbforum0% (1)

- Fee Pilot Comment - PragmaDocument4 pagesFee Pilot Comment - PragmatabbforumNo ratings yet

- Tick Size Pilot: Year in ReviewDocument13 pagesTick Size Pilot: Year in ReviewtabbforumNo ratings yet

- Pylon Public Company Limited 2008 Annual ReportDocument152 pagesPylon Public Company Limited 2008 Annual Reportu5010476No ratings yet

- Standalone Financial Results For March 31, 2016 (Result)Document3 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- 489592katina Stefanova Is CIO and CEO of Marto Capital, A Systematic Multi Strategy Asset Manager. That The Genius of International InvestmentsDocument2 pages489592katina Stefanova Is CIO and CEO of Marto Capital, A Systematic Multi Strategy Asset Manager. That The Genius of International Investmentssamanthawrightkgn6No ratings yet

- Capital Structure of Ranbaxy PharmaDocument40 pagesCapital Structure of Ranbaxy PharmaNooral Alfa100% (1)

- BSC Question of Day(GA/IT): 38 General Knowledge QuestionsDocument59 pagesBSC Question of Day(GA/IT): 38 General Knowledge Questionscbzsports1098No ratings yet

- Investment Vs FinancingDocument6 pagesInvestment Vs FinancingSolomon, Heren Mae M.No ratings yet

- Company Profile SharekhanDocument7 pagesCompany Profile Sharekhangarima_rathi0% (2)

- OtorajaParts PRICE LIST Oct 2022 PDFDocument14 pagesOtorajaParts PRICE LIST Oct 2022 PDFDedi wahyudiNo ratings yet

- BTG EnevaDocument24 pagesBTG EnevaBeto ParanaNo ratings yet

- ANZ Commodity Daily 718 041012Document5 pagesANZ Commodity Daily 718 041012anon_370534332No ratings yet

- CMPMDocument8 pagesCMPMLarry DixonNo ratings yet

- Tax Planning & JV AbroadDocument16 pagesTax Planning & JV AbroadAmit KapoorNo ratings yet

- MidTerm Exam, Partnership Formation, Operation and DissolutionDocument3 pagesMidTerm Exam, Partnership Formation, Operation and DissolutionIñego Begdorf100% (5)

- Remic Guide As Explained To Investors - Easy To UnderstandDocument7 pagesRemic Guide As Explained To Investors - Easy To Understand83jjmackNo ratings yet

- India Cements' Hostile Takeover of Raasi Cements - Case Study on Synergies and Market ConsolidationDocument5 pagesIndia Cements' Hostile Takeover of Raasi Cements - Case Study on Synergies and Market ConsolidationDeepshikha BandebuccheNo ratings yet

- BCOM (Hons) - 2019-II-IV-VI Sem (CBCS)Document2 pagesBCOM (Hons) - 2019-II-IV-VI Sem (CBCS)rajesh khannaNo ratings yet

- Oil and GasDocument4 pagesOil and GasmanasthaNo ratings yet

- Financial Statement AnalysisDocument10 pagesFinancial Statement AnalysisBeth Diaz LaurenteNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument13 pages© The Institute of Chartered Accountants of Indiajanardhan CA,CSNo ratings yet

- Fixed Income Portfolio Management: Achieving Target YieldsDocument2 pagesFixed Income Portfolio Management: Achieving Target YieldsJoel Christian MascariñaNo ratings yet

- Cash Flow of Southwest AirlinesDocument4 pagesCash Flow of Southwest AirlinessumitNo ratings yet

- Karnataka State Co-Operative Apex Bank Limited: Balance Sheet As On 31st March, 2008Document6 pagesKarnataka State Co-Operative Apex Bank Limited: Balance Sheet As On 31st March, 2008ಲೋಕೇಶ್ ಎಂ ಗೌಡNo ratings yet

- Valez Setup 2Document210 pagesValez Setup 2Rodrigo Reis100% (6)

- CH 7 - TAK Soal PDFDocument9 pagesCH 7 - TAK Soal PDFDiny SulisNo ratings yet

- Prospectus AssignmentDocument3 pagesProspectus AssignmentAmy Doll100% (2)

- Case Assignment: Corporate Practice Submitted By: Francis Ray A. FilipinasDocument5 pagesCase Assignment: Corporate Practice Submitted By: Francis Ray A. FilipinasFrancis Ray Arbon FilipinasNo ratings yet

- The Family AdvantageDocument94 pagesThe Family AdvantageBusiness Families FoundationNo ratings yet

- Chapter 2 Basic Concepts in AccountingDocument4 pagesChapter 2 Basic Concepts in AccountinghidayahNo ratings yet

- SAP VAT For GCC CountryDocument16 pagesSAP VAT For GCC CountryEdith Yit50% (2)

- 02 CapStr Basic NiuDocument28 pages02 CapStr Basic NiuLombeNo ratings yet