You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Foreign Marketing SelectionDocument9 pagesForeign Marketing SelectionSammir MalhotraNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Impact of Inflation On PovertyDocument5 pagesImpact of Inflation On PovertyVincent QuitorianoNo ratings yet

- Jima Eco 8Document53 pagesJima Eco 8hunde garumaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

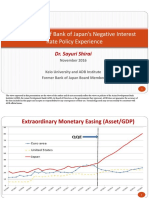

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Macroeconomics Class 12 Circular Flow of Income MCQ-CBSEDocument9 pagesMacroeconomics Class 12 Circular Flow of Income MCQ-CBSEPraveen TiwariNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Applied - Economics - Q1 - SHS AppliedDocument55 pagesApplied - Economics - Q1 - SHS Appliedjoshua seanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Economics Today The Micro 17th Edition Roger LeRoy Miller Test Bank DownloadDocument136 pagesEconomics Today The Micro 17th Edition Roger LeRoy Miller Test Bank DownloadGladys Carr100% (30)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Inflation NoteDocument3 pagesInflation NoteKeith FernándezNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Per Capita Income - Wikipedia - 1 PAgeDocument2 pagesPer Capita Income - Wikipedia - 1 PAgeVinod KaleNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Paul Tudor Jones The Great Liquidity RaceDocument2 pagesPaul Tudor Jones The Great Liquidity RacePeter BullockNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Stock Market Capitalization and Economic Growth in GhanaDocument13 pagesStock Market Capitalization and Economic Growth in GhanaAlexander DeckerNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Ordoliberalism Nov22Document226 pagesOrdoliberalism Nov22benichouNo ratings yet

- Eco415 Chapter 8 Measuring GDP and Ni AccountingDocument39 pagesEco415 Chapter 8 Measuring GDP and Ni AccountingAMIRA100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Report 1 - Lewis ModelDocument11 pagesReport 1 - Lewis ModelLalaine ReyesNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Fis-Balaji Mba College - KadapaDocument97 pagesFis-Balaji Mba College - KadapaBhuvana AnalapudiNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- IGNOU MMPC003 Balance of Payment SlidesDocument13 pagesIGNOU MMPC003 Balance of Payment SlidesAchal MeenaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Quiz - CourseraDocument3 pagesQuiz - CourseraAmay Singh29% (7)

- T6 Pretutorial 2019Document2 pagesT6 Pretutorial 2019karl hemmingNo ratings yet

- Answers To End of Chapter QuestionsDocument59 pagesAnswers To End of Chapter QuestionsBruce_scribed90% (10)

- Economic Growth of The PhilippinesDocument3 pagesEconomic Growth of The Philippinesana villaflorNo ratings yet

- Worksheet Money and Banking 2023Document6 pagesWorksheet Money and Banking 2023Reyaz Khan100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Extension Unit 6Document123 pagesExtension Unit 6Mann PandyaNo ratings yet

- International Finance and Polices: Dr. Bui Thanh LongDocument55 pagesInternational Finance and Polices: Dr. Bui Thanh LongThanh Long BuiNo ratings yet

- FIN350 - Solutions Slides 12Document3 pagesFIN350 - Solutions Slides 12David NguyenNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- ECO701 Economics and The Business EnvironmentDocument17 pagesECO701 Economics and The Business EnvironmentSrijita SahaNo ratings yet

- Nirmala Memorial Foundation College of Commerce and Science Q BDocument3 pagesNirmala Memorial Foundation College of Commerce and Science Q BEmmanuel Kwame OclooNo ratings yet

- 1.economist Name and Quoatation by Manish DuaDocument2 pages1.economist Name and Quoatation by Manish DuaHimanshu SoniNo ratings yet

- Money and InflationDocument1 pageMoney and InflationLucian NutaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Principles of Macroeconomics Sixth Canadian Edition Canadian 6th Edition Mankiw Solutions ManualDocument36 pagesPrinciples of Macroeconomics Sixth Canadian Edition Canadian 6th Edition Mankiw Solutions Manualdemivoltnotpatedf6u2ra100% (24)

- Reseach Paper (BOP) ITLDocument7 pagesReseach Paper (BOP) ITLNeha SachdevaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)