You might also like

- Bunk SheetDocument1 pageBunk Sheetamitesh7224No ratings yet

- Balance Sheet As at 31st March 2015Document1 pageBalance Sheet As at 31st March 2015Mrigul UppalNo ratings yet

- Communication Evaluation SheetDocument1 pageCommunication Evaluation Sheetamitesh7224No ratings yet

- Accenture FY19 Case Workbook One Accenture ConsultingDocument24 pagesAccenture FY19 Case Workbook One Accenture Consultingamitesh7224No ratings yet

- AnnualReport2013 14Document140 pagesAnnualReport2013 14HannahNgoNo ratings yet

- Strategic Marketing Management Cialis Case Study Christopher CashenDocument45 pagesStrategic Marketing Management Cialis Case Study Christopher CashenChristopher Cashen92% (13)

- Mccombs Template Usage NotesDocument25 pagesMccombs Template Usage Notesamitesh7224No ratings yet

- Revocation SDocument17 pagesRevocation Samitesh7224No ratings yet

- Mccombs Template Usage NotesDocument25 pagesMccombs Template Usage Notesamitesh7224No ratings yet

- Appt Town HouseDocument2 pagesAppt Town Houseamitesh7224No ratings yet

- CH 01Document12 pagesCH 01amitesh7224No ratings yet

- AnnualReport2012 13Document148 pagesAnnualReport2012 13Mohit KapoorNo ratings yet

- CLT - SimulateDocument799 pagesCLT - Simulateamitesh7224No ratings yet

- Cialis Marketing PlanDocument5 pagesCialis Marketing PlanAsaad BayanNo ratings yet

- Cialis Marketing PlanDocument5 pagesCialis Marketing PlanAsaad BayanNo ratings yet

- Balance Sheet As at 31st March 2015Document1 pageBalance Sheet As at 31st March 2015Mrigul UppalNo ratings yet

- Resource Allocation and Decision Analysis (ECON 8010) - Spring 2014 "Linear Programming"Document26 pagesResource Allocation and Decision Analysis (ECON 8010) - Spring 2014 "Linear Programming"Kartik KaushikNo ratings yet

- Metron SolutionDocument11 pagesMetron Solutionamitesh7224No ratings yet

- Merton TrucksDocument19 pagesMerton Trucksamitesh7224No ratings yet

- FIRO-B Personality Test Scoring SheetDocument1 pageFIRO-B Personality Test Scoring Sheetamitesh7224No ratings yet

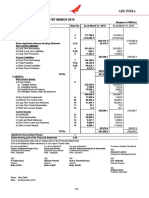

- Balance Sheet As at 31 March 2013: Air IndiaDocument1 pageBalance Sheet As at 31 March 2013: Air Indiaamitesh7224No ratings yet

- SolverTable HelpDocument12 pagesSolverTable HelpJorgitoNo ratings yet

- 80 Rules To Solve Sentence CorrectionDocument20 pages80 Rules To Solve Sentence CorrectionlionlionsherNo ratings yet

- Sap Fico TutorialDocument191 pagesSap Fico TutorialVicky Memon100% (1)

- 900 FOL 36 000000000004 EXT 38 000000000051Document3 pages900 FOL 36 000000000004 EXT 38 000000000051amitesh7224No ratings yet

- SOFMDocument3 pagesSOFMamitesh7224No ratings yet

- Panynj Terminal Planning GuidelinesDocument120 pagesPanynj Terminal Planning Guidelinesamitesh7224No ratings yet

- SrgbtbrelDocument1 pageSrgbtbrelamitesh7224No ratings yet

- 24.airport Terminal PDFDocument17 pages24.airport Terminal PDFAman Jot SinghNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Merger ReportDocument9 pagesMerger ReportArisha KhanNo ratings yet

- ESW Capital OverviewDocument7 pagesESW Capital OverviewindyanexpressNo ratings yet

- Case Interview FrameworksDocument9 pagesCase Interview FrameworksMohit Tuteja67% (3)

- CaterpillarDocument21 pagesCaterpillarZerohedge100% (1)

- The Valuation Effects of Bank MergersDocument26 pagesThe Valuation Effects of Bank MergersVictor CebotariNo ratings yet

- New Balance Athletic Shoe, Inc.Document8 pagesNew Balance Athletic Shoe, Inc.Chanakya Kambhampati0% (1)

- Legal Service For M&A Case in Vietnam: 1. Scope of WorksDocument4 pagesLegal Service For M&A Case in Vietnam: 1. Scope of WorksHà AnhNo ratings yet

- Corporate Innovations Drive M&AsDocument2 pagesCorporate Innovations Drive M&AsMarat SafarliNo ratings yet

- 2018 Salary Guide US Accounting and FinanceDocument33 pages2018 Salary Guide US Accounting and FinanceLuke FinnemoreNo ratings yet

- AR 711-7 Supply Chain ManagementDocument26 pagesAR 711-7 Supply Chain ManagementTom JonesNo ratings yet

- Case Study - Stock Pitch GuideDocument7 pagesCase Study - Stock Pitch GuideMuyuchen Shi100% (1)

- MPI Valuation Opinions & Transaction Advisory Industry Update Q4 2013 Asset ManagementDocument12 pagesMPI Valuation Opinions & Transaction Advisory Industry Update Q4 2013 Asset Managementst96dgx8No ratings yet

- F2 Revision SummariesDocument97 pagesF2 Revision Summarieswakomoli100% (2)

- Diploma in Corporate Finance SyllabusDocument18 pagesDiploma in Corporate Finance Syllabuscima2k15No ratings yet

- Tax Law Project On: Capital Gain and Capital AssetsDocument15 pagesTax Law Project On: Capital Gain and Capital AssetsAazamNo ratings yet

- Wiley Financial Management Association InternationalDocument19 pagesWiley Financial Management Association InternationalKhaeraniMahdinurAwliaNo ratings yet

- Kellton Tech Solutions R 28092018Document7 pagesKellton Tech Solutions R 28092018Suresh Kumar RaiNo ratings yet

- L&T Mindtree Project PresentationDocument8 pagesL&T Mindtree Project PresentationPuneet Agarwal100% (2)

- Agrawal v. MuskDocument39 pagesAgrawal v. MuskTHRNo ratings yet

- Chapter 6 Powerpoint NotesDocument47 pagesChapter 6 Powerpoint NotesJeftaNo ratings yet

- Fmbo Sebi LDDocument10 pagesFmbo Sebi LDPournima KoliNo ratings yet

- Real Estate Merger Motives PDFDocument13 pagesReal Estate Merger Motives PDFadonisghlNo ratings yet

- The Long Case For LKQ CorporationDocument38 pagesThe Long Case For LKQ CorporationAnonymous Ht0MIJNo ratings yet

- Plugin Taxguide 511 Iht BPR Groups Dec 2011Document17 pagesPlugin Taxguide 511 Iht BPR Groups Dec 2011Rashad ShamimNo ratings yet

- Book Review: Sarangi Uthaman 1627654 Mbai2 TrimesterDocument3 pagesBook Review: Sarangi Uthaman 1627654 Mbai2 TrimesterSarangi UthamanNo ratings yet

- Chapter One: The Nature of Strategic ManagementDocument70 pagesChapter One: The Nature of Strategic ManagementNong LegacionNo ratings yet

- Book Solution Economics of Strategy Answer To Questions From The Book Also Relevant For Later Editions of The BookDocument229 pagesBook Solution Economics of Strategy Answer To Questions From The Book Also Relevant For Later Editions of The Bookvgfalcao84100% (2)

- PUX-10659-01042015.) (Repaired)Document45 pagesPUX-10659-01042015.) (Repaired)Afsheen Danish NaqviNo ratings yet

- End Term ACF 2021 Set 2Document2 pagesEnd Term ACF 2021 Set 2pranita mundraNo ratings yet

- Competition Policy COVID-19Document8 pagesCompetition Policy COVID-19Kharla MendivilNo ratings yet