You might also like

- Case Taxation Second BatchDocument3 pagesCase Taxation Second BatchChristopher Jan DotimasNo ratings yet

- G.R. No. 149110Document20 pagesG.R. No. 149110Klein CarloNo ratings yet

- National Power Corp. vs. City of Cabanatuan, 401 SCRA 409Document16 pagesNational Power Corp. vs. City of Cabanatuan, 401 SCRA 409Machida AbrahamNo ratings yet

- Facts:: Cherie Mae F. Aguinaldo National Power Corporation Vs City of CabanatuanDocument2 pagesFacts:: Cherie Mae F. Aguinaldo National Power Corporation Vs City of CabanatuanAnonymous SBT3XU6INo ratings yet

- National Power Corporation vs. City of Cabanatuan PDFDocument30 pagesNational Power Corporation vs. City of Cabanatuan PDFGiuliana FloresNo ratings yet

- NPC V Cabanatuan DigestsDocument2 pagesNPC V Cabanatuan Digestspinkblush717No ratings yet

- National Power Corporation vs. City of CabanatuanDocument21 pagesNational Power Corporation vs. City of CabanatuanMp CasNo ratings yet

- Tax Cases LawDocument48 pagesTax Cases LawferosiacNo ratings yet

- Local Taxation DigestsDocument33 pagesLocal Taxation DigestsmarieNo ratings yet

- NPC V Cabanatuan DigestsDocument2 pagesNPC V Cabanatuan Digestspinkblush717100% (1)

- Taxation Digests Pt. 1Document15 pagesTaxation Digests Pt. 1Laurice PocaisNo ratings yet

- National Power Corporation v. City of Cabanatuan, G.R. No. 149110, April 09, 2003Document19 pagesNational Power Corporation v. City of Cabanatuan, G.R. No. 149110, April 09, 2003Glargo GlargoNo ratings yet

- National Power Corp. v. City of CabanatuanDocument12 pagesNational Power Corp. v. City of CabanatuanJoseph Paolo SantosNo ratings yet

- Taxation 2 Case DigestDocument27 pagesTaxation 2 Case DigestThalia SalvadorNo ratings yet

- NPC v. CITY OF CABANATUANDocument12 pagesNPC v. CITY OF CABANATUANMuhammadIshahaqBinBenjaminNo ratings yet

- C. National Power Corporation Vs City of Cabanatuan, G.R. No. 149110, April 09, 2003Document26 pagesC. National Power Corporation Vs City of Cabanatuan, G.R. No. 149110, April 09, 2003MirafelNo ratings yet

- 001&013-NPC v. City of Cabanatuan G.R. No. 149110 April 9, 2003Document12 pages001&013-NPC v. City of Cabanatuan G.R. No. 149110 April 9, 2003ShaneBeriñaImperialNo ratings yet

- NPC v. City of Cabanatuan, GR No. 149110, April 9, 2003Document4 pagesNPC v. City of Cabanatuan, GR No. 149110, April 9, 2003Judy Anne RamirezNo ratings yet

- Digests Tax RevDocument34 pagesDigests Tax RevJanela LanaNo ratings yet

- Napocor v. Cabanatuan CityDocument6 pagesNapocor v. Cabanatuan Cityjustforscribd2No ratings yet

- C - Ccpetitioner, VS.C C!RespondentDocument23 pagesC - Ccpetitioner, VS.C C!RespondentEMANEMANANSDAJDFNo ratings yet

- C - Ccpetitioner, VS.C C!RespondentDocument28 pagesC - Ccpetitioner, VS.C C!RespondentEMANBVGJHVJHVJNo ratings yet

- National Power Corporation Vs Cabanatuan CityDocument2 pagesNational Power Corporation Vs Cabanatuan CityDario G. TorresNo ratings yet

- 05 National Power Corporation vs. City of CabanatuanDocument2 pages05 National Power Corporation vs. City of CabanatuanJamaica Cabildo ManaligodNo ratings yet

- Philippine Amusement and Gaming Corporation, 197 SCRA 52, Where It Was Held ThatDocument28 pagesPhilippine Amusement and Gaming Corporation, 197 SCRA 52, Where It Was Held ThatLj Brazas SortigosaNo ratings yet

- G.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Document14 pagesG.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Carlo Lopez CantadaNo ratings yet

- I.8 NPC Vs City of Cabanatuan GR No. 149110 04092003 PDFDocument10 pagesI.8 NPC Vs City of Cabanatuan GR No. 149110 04092003 PDFbabyclaire17No ratings yet

- Pepsi Cola Bottling vs. Municipality of Tanuan 69 SCRA 460Document42 pagesPepsi Cola Bottling vs. Municipality of Tanuan 69 SCRA 460Celine GarciaNo ratings yet

- Local TaxationDocument63 pagesLocal TaxationRolando Mauring ReubalNo ratings yet

- G.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Document15 pagesG.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Aerith AlejandreNo ratings yet

- National Power Corporation Vs City of Cabanatuan: Diciembre 5, 2013Document2 pagesNational Power Corporation Vs City of Cabanatuan: Diciembre 5, 2013alexNo ratings yet

- Tax Cases B NatureDocument13 pagesTax Cases B NatureammeNo ratings yet

- G.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Document12 pagesG.R. No. 149110 April 9, 2003 National Power Corporation, Petitioner, CITY OF CABANATUAN, Respondent. PUNO, J.Samuel John CahimatNo ratings yet

- Napocor V City of CabanatuanDocument2 pagesNapocor V City of CabanatuanRyan Vic Abadayan100% (1)

- National Power Corporation Vs City of Cabanatuan, GRDocument4 pagesNational Power Corporation Vs City of Cabanatuan, GRDon Michael ManiegoNo ratings yet

- National Power Corporation vs. City of Cabanatuan FactsDocument6 pagesNational Power Corporation vs. City of Cabanatuan FactsSuzyNo ratings yet

- Napocor Vs City CabanatuanDocument2 pagesNapocor Vs City Cabanatuanhime mejNo ratings yet

- National Power Corporation v. City of CabanatuanDocument21 pagesNational Power Corporation v. City of CabanatuanXyril Ü LlanesNo ratings yet

- Meralco vs. Province of Laguna DigestDocument3 pagesMeralco vs. Province of Laguna DigestMa Gabriellen Quijada-Tabuñag100% (2)

- NPC v. City of Cabanatuan-DigestDocument2 pagesNPC v. City of Cabanatuan-DigestMartel John Milo100% (1)

- NPC V City of Cabanatuan GR No 149110 9 April 2003Document10 pagesNPC V City of Cabanatuan GR No 149110 9 April 2003Mannor ModaNo ratings yet

- National Power Corporation, Petitioner CITY OF CABANATUAN, Respondent FactsDocument5 pagesNational Power Corporation, Petitioner CITY OF CABANATUAN, Respondent FactsEmNo ratings yet

- Manila Electric Co Inc Vs Province of Laguna TAX 1Document3 pagesManila Electric Co Inc Vs Province of Laguna TAX 1Libay Villamor IsmaelNo ratings yet

- Tax Case DigestDocument12 pagesTax Case DigestDanyNo ratings yet

- G.R. No. 149110 - National Power Corporation v. City of CabanatuanDocument24 pagesG.R. No. 149110 - National Power Corporation v. City of CabanatuanCamille CruzNo ratings yet

- Admin Digest CasesDocument94 pagesAdmin Digest CasesKarl Laurenz MagnoNo ratings yet

- NPC v. City of CabanatuanDocument2 pagesNPC v. City of CabanatuanRo CheNo ratings yet

- Petitioner Respondent The Solicitor General Edgardo G. Villarin Trese D. WenceslaoDocument22 pagesPetitioner Respondent The Solicitor General Edgardo G. Villarin Trese D. WenceslaoAggy AlbotraNo ratings yet

- PubCorp Case Set 5Document65 pagesPubCorp Case Set 5Benjie PangosfianNo ratings yet

- Supreme Court: Charges by Government and Governmental Instrumentalities.-The Corporation Shall Be Non-Profit and ShallDocument10 pagesSupreme Court: Charges by Government and Governmental Instrumentalities.-The Corporation Shall Be Non-Profit and ShallRYWELLE BRAVONo ratings yet

- Admin CasesDocument95 pagesAdmin CasesKarl Laurenz MagnoNo ratings yet

- Commission On Internal Revenue vs. AlgueDocument3 pagesCommission On Internal Revenue vs. AlgueVikki AmorioNo ratings yet

- NPC vs. City of Cabanatuan DigestDocument3 pagesNPC vs. City of Cabanatuan DigestMa Gabriellen Quijada-Tabuñag100% (1)

- Napocor VS City of CabanatuanDocument3 pagesNapocor VS City of CabanatuanbelleferiesebelsaNo ratings yet

- Meralco Vs Province of Laguna 1999Document7 pagesMeralco Vs Province of Laguna 1999Jaycil GaaNo ratings yet

- MERALCO v. Laguna (Non - Impairment Clause Does Not Apply To Franchise)Document5 pagesMERALCO v. Laguna (Non - Impairment Clause Does Not Apply To Franchise)Sarah Jane-Shae O. SemblanteNo ratings yet

- Petitioner Respondent The Solicitor General Edgardo G. Villarin Trese D. WenceslaoDocument23 pagesPetitioner Respondent The Solicitor General Edgardo G. Villarin Trese D. WenceslaoArste GimoNo ratings yet

- NPC Vs City of CabanatuanDocument2 pagesNPC Vs City of Cabanatuan8111 aaa 1118100% (1)

- MERALCO VS PROVINCE OF LAGUNA DigestedDocument3 pagesMERALCO VS PROVINCE OF LAGUNA DigestedSuzyNo ratings yet

- 10 LBP Vs LajomDocument2 pages10 LBP Vs LajomJanno Sangalang100% (2)

- 82 LBP Vs DalautaDocument2 pages82 LBP Vs DalautaJanno SangalangNo ratings yet

- Galope Vs BugarinDocument2 pagesGalope Vs BugarinJanno SangalangNo ratings yet

- Leoveraz Vs ValdezDocument2 pagesLeoveraz Vs ValdezJanno Sangalang100% (1)

- 37 Caluzor Vs LlanilloDocument2 pages37 Caluzor Vs LlanilloJanno SangalangNo ratings yet

- 25 Republic Vs RoxasDocument4 pages25 Republic Vs RoxasJanno Sangalang0% (1)

- 40 Borromeo Vs DescallarDocument3 pages40 Borromeo Vs DescallarJanno SangalangNo ratings yet

- 10 Sps. Evangelista v. Mercator Finance Corp.Document2 pages10 Sps. Evangelista v. Mercator Finance Corp.Janno Sangalang100% (1)

- 35 Republic Vs AquinoDocument2 pages35 Republic Vs AquinoJanno SangalangNo ratings yet

- 290 PentCapital Investment Corporation Vs MahinayDocument2 pages290 PentCapital Investment Corporation Vs MahinayJanno SangalangNo ratings yet

- 125 Consolidated Plywood Industries Vs BrevaDocument2 pages125 Consolidated Plywood Industries Vs BrevaJanno SangalangNo ratings yet

- 92 Montenegro Vs MontenegroDocument2 pages92 Montenegro Vs MontenegroJanno Sangalang67% (3)

- 59 Motor Services Vs Yellow Taxicab Co.Document2 pages59 Motor Services Vs Yellow Taxicab Co.Janno SangalangNo ratings yet

- Miles Vs LaoDocument2 pagesMiles Vs LaoJanno SangalangNo ratings yet

- 51 Rojas Vs MaglanaDocument3 pages51 Rojas Vs MaglanaJanno SangalangNo ratings yet

- 09 Republic Planters Bank v. CADocument3 pages09 Republic Planters Bank v. CAJanno SangalangNo ratings yet

- Sadaya v. SevillaDocument2 pagesSadaya v. SevillaJanno SangalangNo ratings yet

- 32 Republic vs. EbradaDocument2 pages32 Republic vs. EbradaJanno SangalangNo ratings yet

- 15 Anillo Vs COSLAPDocument2 pages15 Anillo Vs COSLAPJanno SangalangNo ratings yet

- 39 Metrobank vs. CabilzoDocument3 pages39 Metrobank vs. CabilzoJanno SangalangNo ratings yet

- 03 Sumulong Vs COMELECDocument2 pages03 Sumulong Vs COMELECJanno Sangalang100% (1)

- 71 Bank of Commerce Vs NiteDocument2 pages71 Bank of Commerce Vs NiteJanno SangalangNo ratings yet

- 11 Respect of Dignity, Personality, EtcDocument1 page11 Respect of Dignity, Personality, EtcJanno SangalangNo ratings yet

- 125 Vargas and Co. Vs Chan Hang ChiuDocument2 pages125 Vargas and Co. Vs Chan Hang ChiuJanno SangalangNo ratings yet

- 25 Siga-An Vs VillanuevaDocument2 pages25 Siga-An Vs VillanuevaJanno Sangalang100% (1)

- 26 People Vs LadjaalamDocument2 pages26 People Vs LadjaalamJanno Sangalang100% (1)

- 59 People Vs AgulayDocument2 pages59 People Vs AgulayJanno SangalangNo ratings yet

- 04 Loong Vs ComelecDocument2 pages04 Loong Vs ComelecJanno SangalangNo ratings yet

- 95 Triesta Vs SandiganbayanDocument1 page95 Triesta Vs SandiganbayanJanno SangalangNo ratings yet

- Lily Sy V Hon Secretary of JusticeDocument2 pagesLily Sy V Hon Secretary of JusticeJanno SangalangNo ratings yet

- ACC1AIS - Homework Exercises - Week 10: Excel Exercise 1 - Prepare Vertical AnalysisDocument3 pagesACC1AIS - Homework Exercises - Week 10: Excel Exercise 1 - Prepare Vertical AnalysisSuptoNo ratings yet

- Cashflow Template For Construction IndustryDocument1 pageCashflow Template For Construction IndustryCrestNo ratings yet

- Reviewer in FabmDocument5 pagesReviewer in FabmJhoanna Elaine CuizonNo ratings yet

- Tax-1 SyllabusDocument16 pagesTax-1 SyllabusJennica Gyrl DelfinNo ratings yet

- Tugas Ch.20Document9 pagesTugas Ch.20Chupa HesNo ratings yet

- Liab Test BankDocument72 pagesLiab Test BankMyles Ninon LazoNo ratings yet

- Visual FoxProDocument1 pageVisual FoxProAjit RautNo ratings yet

- Fine Art - Direct and Indirect Taxation Aspects: A Masterwork of ComplexityDocument12 pagesFine Art - Direct and Indirect Taxation Aspects: A Masterwork of ComplexityMark KubanNo ratings yet

- On June 1 of This Year J Larkin Optometrist Established The Larkin Eye Clinic The ClinicsDocument3 pagesOn June 1 of This Year J Larkin Optometrist Established The Larkin Eye Clinic The ClinicsCharlotteNo ratings yet

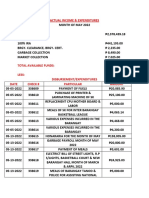

- Actual Income & ExpendituresDocument5 pagesActual Income & Expendituressan nicolas 2nd betis guagua pampangaNo ratings yet

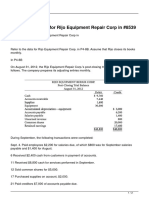

- Refer To The Data For Rijo Equipment Repair Corp inDocument2 pagesRefer To The Data For Rijo Equipment Repair Corp inMiroslav Gegoski0% (1)

- Chapter 13 - Return Filing - NotesDocument6 pagesChapter 13 - Return Filing - NotesAkshay PooniaNo ratings yet

- CIA3010 Week 10 DiscussionsDocument4 pagesCIA3010 Week 10 DiscussionsWong Yong Sheng WongNo ratings yet

- Group 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument18 pagesGroup 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeRhad Lester C. MaestradoNo ratings yet

- Assume XYZ Company Is A Merchandising Business and Registered For VAT WhichDocument6 pagesAssume XYZ Company Is A Merchandising Business and Registered For VAT WhichKen LatiNo ratings yet

- Problem 23-16Document9 pagesProblem 23-16anneliban499No ratings yet

- T2 Corporation Income Tax Return (2019 and Later Tax Years) : IdentificationDocument9 pagesT2 Corporation Income Tax Return (2019 and Later Tax Years) : IdentificationBryan WilleyNo ratings yet

- Solved The Outstanding Stock in Red Blue and Green Corporations EachDocument1 pageSolved The Outstanding Stock in Red Blue and Green Corporations EachAnbu jaromiaNo ratings yet

- CHP 3Document23 pagesCHP 3Laiba SadafNo ratings yet

- Financial Accounting and ReportingDocument1 pageFinancial Accounting and ReportingPaula BautistaNo ratings yet

- SyllabusDocument5 pagesSyllabusGLYDEL ESIONGNo ratings yet

- Your GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Document2 pagesYour GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Karaoui LaidNo ratings yet

- You Are A Manager at Northern Fibre Which Is ConsideringDocument1 pageYou Are A Manager at Northern Fibre Which Is ConsideringAmit PandeyNo ratings yet

- RMC 17 2011 Notes To FS Taxes PDFDocument3 pagesRMC 17 2011 Notes To FS Taxes PDFMarie Vea RamosNo ratings yet

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatusAndyTomas100% (1)

- Lesson 5: Taxation of CorporationsDocument14 pagesLesson 5: Taxation of CorporationsGio yowyowNo ratings yet

- XXXX2681 2020 1099 02-04-2021Document14 pagesXXXX2681 2020 1099 02-04-2021Nicholas FusaroNo ratings yet

- Indian Income Tax Return: (Refer Instructions For Eligibility)Document6 pagesIndian Income Tax Return: (Refer Instructions For Eligibility)shivam raiNo ratings yet

- Solved MR Alm Earned A 61 850 Salary and Recognized A 5 600Document1 pageSolved MR Alm Earned A 61 850 Salary and Recognized A 5 600Anbu jaromiaNo ratings yet

- Accrual and Cash BasisDocument4 pagesAccrual and Cash BasisShe Enna Ortaleza Ulap100% (1)