You might also like

- Petrobowl QuestionsDocument59 pagesPetrobowl QuestionsMonica100% (1)

- Canaan Group Financial AnalysisDocument1 pageCanaan Group Financial AnalysisAparna GannavarapuNo ratings yet

- Cairn ReportDocument37 pagesCairn ReportRaghav AryaNo ratings yet

- Ogfj201601 DLDocument68 pagesOgfj201601 DLJasgeoNo ratings yet

- The Evolving Domestic & Global Crude Oil Pricing Landscape: An Inside Look at The Gulf Coast Infrastructure & Supply ChainDocument15 pagesThe Evolving Domestic & Global Crude Oil Pricing Landscape: An Inside Look at The Gulf Coast Infrastructure & Supply ChainColin GardetteNo ratings yet

- Oceanagold Corporation: Sepq Report - First LookDocument5 pagesOceanagold Corporation: Sepq Report - First Lookashok yadavNo ratings yet

- 2021 Int'l and Offshore OutlookDocument26 pages2021 Int'l and Offshore OutlookHung100% (1)

- Implementation of Wave Effects in The Unstructured Delft3D Suite FinalDocument24 pagesImplementation of Wave Effects in The Unstructured Delft3D Suite FinalSud HaldarNo ratings yet

- International Oil Gas Report 061608Document204 pagesInternational Oil Gas Report 061608hurdleNo ratings yet

- Pretium Resources - Broker Reports - Thomson One - 3 MonthsDocument39 pagesPretium Resources - Broker Reports - Thomson One - 3 MonthsJZNo ratings yet

- APC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightDocument10 pagesAPC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightAshokNo ratings yet

- Industry Note: Equity ResearchDocument10 pagesIndustry Note: Equity ResearchForexliveNo ratings yet

- AMR 3Q EPS Preview: Back On TrackDocument10 pagesAMR 3Q EPS Preview: Back On TrackAshokNo ratings yet

- All About Pakistan's Oil & Gas Exploration CompaniesDocument13 pagesAll About Pakistan's Oil & Gas Exploration CompaniesFahad HussainNo ratings yet

- Numis June 2018 Teach-In 28 JunDocument34 pagesNumis June 2018 Teach-In 28 JunAyo OgunkanmiNo ratings yet

- 2019-09-16-EOG.v-hannam Partners-Second Discovery De-Risks Development and Further ... - 86211411Document5 pages2019-09-16-EOG.v-hannam Partners-Second Discovery De-Risks Development and Further ... - 86211411Anonymous xAIKZFSomNo ratings yet

- Core Laboratories: Innovative Technology: Impacting Energy Industry ReturnsDocument21 pagesCore Laboratories: Innovative Technology: Impacting Energy Industry ReturnsAlekseiNo ratings yet

- Hecla Mining Sept 2009 PresentationDocument14 pagesHecla Mining Sept 2009 PresentationAla BasterNo ratings yet

- 2023 Global Private Equity OutlookDocument52 pages2023 Global Private Equity OutlookYing SunNo ratings yet

- OKE - ArgusDocument5 pagesOKE - ArgusJeff SturgeonNo ratings yet

- Crude PricingDocument1 pageCrude PricingSmitha MohanNo ratings yet

- Z Borowski 2018Document3 pagesZ Borowski 2018Google mailNo ratings yet

- Business Standard English MumbaiDocument27 pagesBusiness Standard English MumbaiRajan NandolaNo ratings yet

- Cameco Investor Presentation 2019 Q3Document28 pagesCameco Investor Presentation 2019 Q3jesusftNo ratings yet

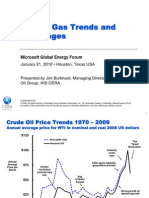

- Jim Burkhard Microsoft Jan 21 2010Document11 pagesJim Burkhard Microsoft Jan 21 2010Charan RajNo ratings yet

- ATP FLight School Career GuideDocument18 pagesATP FLight School Career GuideDevNo ratings yet

- Hibiscus Petroleum Berhad (5199.KL) Equity Analysis (5 Apr 2020)Document26 pagesHibiscus Petroleum Berhad (5199.KL) Equity Analysis (5 Apr 2020)soumyaNo ratings yet

- Blue Nile 050809Document12 pagesBlue Nile 050809Brian BolanNo ratings yet

- JPM Oil 2030 - Long Term Incentive Oil PriceDocument54 pagesJPM Oil 2030 - Long Term Incentive Oil PriceНикита МузафаровNo ratings yet

- UOB Company Update AKRA 12 Jul 2023Document5 pagesUOB Company Update AKRA 12 Jul 2023botoy26No ratings yet

- Inco 070606Document3 pagesInco 070606Cristiano DonzaghiNo ratings yet

- Upl PDFDocument44 pagesUpl PDFbharat005No ratings yet

- Faro Energy Remanso Norte 25052018Document27 pagesFaro Energy Remanso Norte 250520181 aguilarNo ratings yet

- Investor Information: Published May 1, 2019Document40 pagesInvestor Information: Published May 1, 2019Sohini ChatterjeeNo ratings yet

- AKD Detailed Sep 21 2022Document8 pagesAKD Detailed Sep 21 2022shahjahanabdulrehmanNo ratings yet

- Wallstreetjournal 20161201 The Wall Street JournalDocument38 pagesWallstreetjournal 20161201 The Wall Street JournaljohnNo ratings yet

- Tanker Monthly - July 2023Document9 pagesTanker Monthly - July 2023Mai PhamNo ratings yet

- Permian Basin & Eagle Ford Shale From A Global Perspective - Art Berman 2018Document16 pagesPermian Basin & Eagle Ford Shale From A Global Perspective - Art Berman 2018Cliffhanger100% (1)

- News Release: Newmont Updates 5-Year Business Plan - 2003 Gold Reserves in Ghana Expected To Reach 10 Million OuncesDocument12 pagesNews Release: Newmont Updates 5-Year Business Plan - 2003 Gold Reserves in Ghana Expected To Reach 10 Million OuncescobbymarkNo ratings yet

- Oil Sensitivities From ScotiaDocument20 pagesOil Sensitivities From ScotiaForexliveNo ratings yet

- Design 2 CH 2Document14 pagesDesign 2 CH 2thankikalpeshNo ratings yet

- Stock Report - Dangote Cement PLC Q1 20 - Facing COVID Tides With Additional CapDocument5 pagesStock Report - Dangote Cement PLC Q1 20 - Facing COVID Tides With Additional CapMichael AdesanyaNo ratings yet

- EFERT Dividend Galore...Document3 pagesEFERT Dividend Galore...bilal aliNo ratings yet

- Eloro Resources LTD.: High-Grade Breccias in Stable JurisdictionsDocument68 pagesEloro Resources LTD.: High-Grade Breccias in Stable JurisdictionsAniket BokeNo ratings yet

- JP Morgan KLBN4@BZ Pulp Open Parachute - Downgrading SUZB & KLBN To NeutraDocument26 pagesJP Morgan KLBN4@BZ Pulp Open Parachute - Downgrading SUZB & KLBN To NeutraVinicius AssisNo ratings yet

- UOB Company Update AKRA 19 May 2023 Maintain Buy Higher TP Rp1,750Document5 pagesUOB Company Update AKRA 19 May 2023 Maintain Buy Higher TP Rp1,750ekaNo ratings yet

- Cheyenne IDocument13 pagesCheyenne IYuri AlexanderNo ratings yet

- Orchard Projections (Imperial Units)Document11 pagesOrchard Projections (Imperial Units)Chandler OrchardsNo ratings yet

- WLL Eft 10.31.19Document91 pagesWLL Eft 10.31.19HECTOR FLORESNo ratings yet

- Insights Bullish Near Term OutlookDocument62 pagesInsights Bullish Near Term OutlookHandy HarisNo ratings yet

- Flex LNG Dec 2019 Presentation VFDocument24 pagesFlex LNG Dec 2019 Presentation VFClaudio Osvaldo Vargas FarfanNo ratings yet

- MAC: Ready For Takeoff: Notable MoversDocument4 pagesMAC: Ready For Takeoff: Notable MoversJNo ratings yet

- Nippon Indosari Corpindo: No Room For ErrorDocument10 pagesNippon Indosari Corpindo: No Room For Errorainia putriNo ratings yet

- BP Report NewDocument22 pagesBP Report NewKatie WilliamsNo ratings yet

- 2018 01 22 - Presentation - Transforming TT Natural Gas - Energy Conference 2018 - Pres Mark LoquanDocument20 pages2018 01 22 - Presentation - Transforming TT Natural Gas - Energy Conference 2018 - Pres Mark LoquanrubenpeNo ratings yet

- CPNO Copano Energy Jan 2010 PresentationDocument59 pagesCPNO Copano Energy Jan 2010 PresentationAla BasterNo ratings yet

- Inventory Lecture 2 PDFDocument13 pagesInventory Lecture 2 PDFWaqas KhanNo ratings yet

- Control de Lectura 1 - 2do ParcialDocument5 pagesControl de Lectura 1 - 2do ParcialPaulaNo ratings yet

- Fact Sheet Q3 - 2016: OverviewDocument3 pagesFact Sheet Q3 - 2016: OverviewkaiselkNo ratings yet

- Man Industries LTD.: CMP Rs.58 (2.0X Fy22E P/E) Not RatedDocument5 pagesMan Industries LTD.: CMP Rs.58 (2.0X Fy22E P/E) Not RatedshahavNo ratings yet

- Staff ReportDocument7 pagesStaff Reportlbaker2009No ratings yet

- Vidler - VisionDocument2 pagesVidler - Visionlbaker2009No ratings yet

- 2016 Baird Conference Deck FINALDocument10 pages2016 Baird Conference Deck FINALlbaker2009No ratings yet

- Wiwellwater101 Ver2Document63 pagesWiwellwater101 Ver2lbaker2009No ratings yet

- Layne Water Midstream PresentationDocument10 pagesLayne Water Midstream Presentationlbaker2009No ratings yet

- 2 - Treasury Infrastructure White Paper 042215Document29 pages2 - Treasury Infrastructure White Paper 042215lbaker2009No ratings yet

- Mi - Data Brochure 2016Document4 pagesMi - Data Brochure 2016lbaker2009No ratings yet

- AviTrader Aviation Marketplace 2015-03-23Document4 pagesAviTrader Aviation Marketplace 2015-03-23lbaker2009No ratings yet

- 974 I. Jurisdictional Fact 978Document48 pages974 I. Jurisdictional Fact 978lbaker2009No ratings yet

- Water Springs PDFDocument10 pagesWater Springs PDFlbaker2009No ratings yet

- PEA Comp Study - Estate Planning For Private Equity Fund Managers (ITaback, JWaxenberg 10 - 10)Document13 pagesPEA Comp Study - Estate Planning For Private Equity Fund Managers (ITaback, JWaxenberg 10 - 10)lbaker2009No ratings yet

- Usg PDFDocument14 pagesUsg PDFlbaker2009No ratings yet

- DB Presentation On Longevity Risk PDFDocument25 pagesDB Presentation On Longevity Risk PDFlbaker2009No ratings yet

- Industry Trends To Watch For: Airframer Momentum & StrategyDocument1 pageIndustry Trends To Watch For: Airframer Momentum & Strategylbaker2009No ratings yet

- Trusts Arent Just For Taxes and They Never Were - NJLJ - EW&MV - 02.08.10Document2 pagesTrusts Arent Just For Taxes and They Never Were - NJLJ - EW&MV - 02.08.10lbaker2009No ratings yet

- CIT PageDocument1 pageCIT Pagelbaker2009No ratings yet

- Shale Gas & Oil ShaleDocument17 pagesShale Gas & Oil ShaleNorfolkingNo ratings yet

- Hughes - Exec Sum - Shale Reality Check 2021Document10 pagesHughes - Exec Sum - Shale Reality Check 2021Budi KhoironiNo ratings yet

- Prospects & PropertiesDocument24 pagesProspects & Propertiesreceuerdeme100% (2)

- How Oil Drilling Works: Craig C. Freudenrich, PH.DDocument18 pagesHow Oil Drilling Works: Craig C. Freudenrich, PH.DmohammedNo ratings yet

- Goehring & Rozencwajg Oil Market CommentaryDocument27 pagesGoehring & Rozencwajg Oil Market CommentaryYog MehtaNo ratings yet

- 2018-08-01 - Compressor - Tech2 'I'Document76 pages2018-08-01 - Compressor - Tech2 'I'ferick23No ratings yet

- 2013 IAE ShaleOilandGas Resources PDFDocument730 pages2013 IAE ShaleOilandGas Resources PDFBruno PortillaNo ratings yet

- Amalga Trader Magazine 201401Document77 pagesAmalga Trader Magazine 201401lowtarhk0% (1)

- Oil and Gas Dec 2010Document32 pagesOil and Gas Dec 2010sakoboyNo ratings yet

- Spe 199993 MSDocument28 pagesSpe 199993 MSHussam AgabNo ratings yet

- TAG Oil Reports 100% Increase in Production Revenue & Strong Year-End Financial ResultsDocument6 pagesTAG Oil Reports 100% Increase in Production Revenue & Strong Year-End Financial ResultsmpgervetNo ratings yet

- Frac SandsDocument36 pagesFrac SandsDavid A. CuéllarNo ratings yet

- BSM - BARCLAYS - Initiation Report - 05 26 2015Document21 pagesBSM - BARCLAYS - Initiation Report - 05 26 2015Shivam GuptaNo ratings yet

- December 2014Document64 pagesDecember 2014Gas, Oil & Mining Contractor MagazineNo ratings yet

- Hydraulic Fracture Design Optimization in Unconventional Reservoirs - A Case History PDFDocument14 pagesHydraulic Fracture Design Optimization in Unconventional Reservoirs - A Case History PDFblackoil1981No ratings yet

- Epm 2013 05Document149 pagesEpm 2013 05jpsi6No ratings yet

- Assessment of Crude by Rail (CBR) Safety Issues in Commonwealth of PennsylvaniaDocument84 pagesAssessment of Crude by Rail (CBR) Safety Issues in Commonwealth of PennsylvaniaGovernor Tom Wolf100% (1)

- Squeezing Profits From ShaleDocument189 pagesSqueezing Profits From Shaleatilio martinezNo ratings yet

- CMGWebinar Unconventional Reservoir Modelling 18feb15Document49 pagesCMGWebinar Unconventional Reservoir Modelling 18feb15mvinassa4828100% (2)

- IOR & EOR in Tight Reservoirs - BakkenDocument47 pagesIOR & EOR in Tight Reservoirs - Bakkennitin lahkarNo ratings yet

- GALWE - Ligue Marc Marcel DjoDocument26 pagesGALWE - Ligue Marc Marcel DjozazamanNo ratings yet

- Nov 2016Document104 pagesNov 2016chuchin28No ratings yet

- Torcuk Mines 0052N 10192 PDFDocument69 pagesTorcuk Mines 0052N 10192 PDFKenny WidjayaNo ratings yet

- GEO ExPro V7i2 Full PDFDocument44 pagesGEO ExPro V7i2 Full PDFAjay PundirNo ratings yet

- SLB Shale Oil Case Study InternalDocument2 pagesSLB Shale Oil Case Study Internalapi-205999899No ratings yet

- Oil & Gas Financial JournalDocument68 pagesOil & Gas Financial Journalabsolutvacio82No ratings yet

- Bison Courier, July 25, 2013Document20 pagesBison Courier, July 25, 2013surfnewmediaNo ratings yet

- SPE 135319-Bakken Completion PNP Vs OH Packers With Frac ValvesDocument17 pagesSPE 135319-Bakken Completion PNP Vs OH Packers With Frac ValvesJose Gregorio FariñasNo ratings yet