You might also like

- FINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSDocument9 pagesFINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSPau Santos76% (29)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Accounting for Investment in AssociatesDocument10 pagesAccounting for Investment in AssociatesShaina SamonteNo ratings yet

- Investment in Associate-HandoutDocument9 pagesInvestment in Associate-HandoutPhoeza Espinosa VillanuevaNo ratings yet

- PAS 28 Investment in Associates and Joint VenturesDocument29 pagesPAS 28 Investment in Associates and Joint Venturesrena chavez100% (2)

- Exercise 2 - Hotel Project FinanceDocument30 pagesExercise 2 - Hotel Project FinanceAtish Satam100% (1)

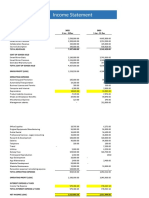

- Tibetan Grill Region 5 P&L ReportDocument23 pagesTibetan Grill Region 5 P&L ReportTTV TimeKpRNo ratings yet

- Investment in AssociateDocument60 pagesInvestment in Associateadarose romaresNo ratings yet

- ITAE Student Guide v1.0Document44 pagesITAE Student Guide v1.0evianneyh8010No ratings yet

- Investment in Associate PDFDocument3 pagesInvestment in Associate PDFVillaruz Shereen MaeNo ratings yet

- 2022 Level I Key Facts and Formulas SheetDocument13 pages2022 Level I Key Facts and Formulas Sheetayesha ansari100% (2)

- Gold and Blue Summary Notes - Investment in AssociateDocument6 pagesGold and Blue Summary Notes - Investment in AssociateBryzan Dela CruzNo ratings yet

- Impairment of Loans and Receivable FinancingDocument17 pagesImpairment of Loans and Receivable FinancingGelyn CruzNo ratings yet

- Investing in Associates: Accounting for Significant InfluenceDocument7 pagesInvesting in Associates: Accounting for Significant InfluenceCharice Anne VillamarinNo ratings yet

- Accounting for Investments in AssociatesDocument5 pagesAccounting for Investments in AssociatesRodelLaborNo ratings yet

- Chapter 17 - Investment in Associate PDFDocument14 pagesChapter 17 - Investment in Associate PDFTurks100% (1)

- IFRS9 Financial Instruments 2018 PDFDocument108 pagesIFRS9 Financial Instruments 2018 PDFYo ThuvanNo ratings yet

- Summary of Pas 28 Investments in Associates and Joint VenturesDocument8 pagesSummary of Pas 28 Investments in Associates and Joint VenturesFatima Guevarra100% (2)

- Audit of LiabilityDocument8 pagesAudit of LiabilityMark Lord Morales Bumagat50% (2)

- Audit of LiabilityDocument8 pagesAudit of LiabilityMark Lord Morales Bumagat50% (2)

- Full Download Advanced Accounting 12th Edition Beams Solutions ManualDocument36 pagesFull Download Advanced Accounting 12th Edition Beams Solutions Manualrojeroissy2232s100% (39)

- Chapter 12Document57 pagesChapter 12Crestu Jin0% (1)

- FAR MerchandisingDocument68 pagesFAR MerchandisingAira DavidNo ratings yet

- #15 Investment in AssociatesDocument3 pages#15 Investment in AssociatesZaaavnn VannnnnNo ratings yet

- 17 - Investment-In Associate (Basic Principles)Document44 pages17 - Investment-In Associate (Basic Principles)KhenNo ratings yet

- Cima F1 Chapter 4Document20 pagesCima F1 Chapter 4MichelaRosignoli100% (1)

- Chap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFDocument5 pagesChap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFSuper JhedNo ratings yet

- Problems Audit of Investments PDFDocument17 pagesProblems Audit of Investments PDFLove alexchelle ducut0% (1)

- FARAP 4406A Investment in Equity SecuritiesDocument8 pagesFARAP 4406A Investment in Equity SecuritiesLei PangilinanNo ratings yet

- Pas 28 Investment in Associate & Joint VentureDocument4 pagesPas 28 Investment in Associate & Joint VentureElaiza Jane CruzNo ratings yet

- Accounting for Investments in Associates and Joint VenturesDocument31 pagesAccounting for Investments in Associates and Joint VenturesAivan Kiel100% (1)

- Brown Monochrome Simple Minimalist Research Project Final Defense Presentation TemplateDocument24 pagesBrown Monochrome Simple Minimalist Research Project Final Defense Presentation TemplateFranze CincoNo ratings yet

- Ias 28 - Investments in AssociatesDocument14 pagesIas 28 - Investments in AssociatesJaaNo ratings yet

- Topic 1Document59 pagesTopic 1SarannyaRajendraNo ratings yet

- PAS 28 Equity Method AssociatesDocument5 pagesPAS 28 Equity Method AssociatesJustine VeralloNo ratings yet

- Pas 28Document3 pagesPas 28Jay JavierNo ratings yet

- Significant Influence EvidenceDocument5 pagesSignificant Influence Evidenceelle friasNo ratings yet

- Yasir Riaz CFAP 1 Chap 6Document27 pagesYasir Riaz CFAP 1 Chap 6rameelamirNo ratings yet

- Ia - 1 - Chapter 17 Investment in Associate Basic PrinciplesDocument19 pagesIa - 1 - Chapter 17 Investment in Associate Basic PrinciplesKhezia Mae U. GarlandoNo ratings yet

- M3 Accele 4Document15 pagesM3 Accele 4Julie Marie Anne LUBINo ratings yet

- Notes For IaDocument3 pagesNotes For IaHassan AdamNo ratings yet

- Chapter 5 Investments in Equity SecuritiesDocument13 pagesChapter 5 Investments in Equity SecuritiesKrissa Mae Longos100% (2)

- Accounting for investment in associates (Part 3Document2 pagesAccounting for investment in associates (Part 3JonieNo ratings yet

- Nvestment in AssociatesDocument4 pagesNvestment in AssociatesJeric Lagyaban AstrologioNo ratings yet

- 161 15 PAS 28 Investment in AssociateDocument2 pages161 15 PAS 28 Investment in AssociateRegina Gregoria SalasNo ratings yet

- Investments in Associates and Joint VenturesDocument4 pagesInvestments in Associates and Joint VenturesBrigit MartinezNo ratings yet

- As 23Document6 pagesAs 23abhishekkapse654No ratings yet

- W10 Module 15 Investment in Associates Impairment of AssetDocument12 pagesW10 Module 15 Investment in Associates Impairment of Assethaven AvyyNo ratings yet

- ACC 226 Week 4 To 5 SIMDocument33 pagesACC 226 Week 4 To 5 SIMMireya YueNo ratings yet

- AA2 Chapter 12 SolutionDocument57 pagesAA2 Chapter 12 SolutionDaisy Mae HardingNo ratings yet

- Chap 002Document45 pagesChap 002poop gravy100% (1)

- ReSA CPA Review Batch 43 Investment in AssociatesDocument4 pagesReSA CPA Review Batch 43 Investment in AssociatesATHALIAH LUNA MERCADEJASNo ratings yet

- Acctg3-7 Associates and Joint VentureDocument2 pagesAcctg3-7 Associates and Joint Ventureflammy07No ratings yet

- Chap 002Document52 pagesChap 002Kiky Agustyan TanoewidjajaNo ratings yet

- Audit of Investments - Equity Method and ImpairmentDocument2 pagesAudit of Investments - Equity Method and Impairmentantonette seradNo ratings yet

- Intermediate 2nd Sem (Midterm)Document13 pagesIntermediate 2nd Sem (Midterm)Mariella louise RoblesNo ratings yet

- 06A Investment in Equity Securities (Financial Assets at FMV, Investment in Associates)Document6 pages06A Investment in Equity Securities (Financial Assets at FMV, Investment in Associates)randomlungs121223No ratings yet

- Chapter 10 PAS 28 INVESTMENT IN ASSOCIATESDocument2 pagesChapter 10 PAS 28 INVESTMENT IN ASSOCIATESgabriel ramosNo ratings yet

- 12 Investment in AssociateDocument3 pages12 Investment in AssociateLara Jane Dela CruzNo ratings yet

- Joint Arrangements and Accounting for AssociatesDocument22 pagesJoint Arrangements and Accounting for AssociatesBianca AcoymoNo ratings yet

- Accounting for associates and financial instrumentsDocument29 pagesAccounting for associates and financial instrumentsHiền MỹNo ratings yet

- Lesson 6Document12 pagesLesson 6shadowlord468No ratings yet

- Standards On ConsoDocument33 pagesStandards On ConsobiggykhairNo ratings yet

- Investment in AssociateDocument11 pagesInvestment in AssociateElla MontefalcoNo ratings yet

- Full Download Advanced Accounting 13th Edition Beams Solutions ManualDocument36 pagesFull Download Advanced Accounting 13th Edition Beams Solutions Manualjacksongubmor100% (34)

- AccountsDocument19 pagesAccountssampat97No ratings yet

- Material Part IDocument64 pagesMaterial Part IKrishna AdhikariNo ratings yet

- Dwnload Full Advanced Accounting 13th Edition Beams Solutions Manual PDFDocument36 pagesDwnload Full Advanced Accounting 13th Edition Beams Solutions Manual PDFunrudesquirtjghzl100% (15)

- Borrowing Cost - Investment in AssociatesDocument16 pagesBorrowing Cost - Investment in AssociatesJomerNo ratings yet

- CFAS PAS 28 Investment in AssociatesDocument1 pageCFAS PAS 28 Investment in AssociatesErica mae BodosoNo ratings yet

- Investments in Associates and Investments in Jointly Controlled EntitiesDocument47 pagesInvestments in Associates and Investments in Jointly Controlled EntitiesPhilip Dan Jayson LarozaNo ratings yet

- Serial Bonds and TDRDocument2 pagesSerial Bonds and TDRLove alexchelle ducutNo ratings yet

- Choice of Remedies PDFDocument8 pagesChoice of Remedies PDFLove alexchelle ducutNo ratings yet

- Accounting Summay Serial BondsDocument75 pagesAccounting Summay Serial BondsLove alexchelle ducutNo ratings yet

- Accounting Exam 16 September 2018 Questions PDFDocument5 pagesAccounting Exam 16 September 2018 Questions PDFLove alexchelle ducutNo ratings yet

- F2 Fin Acc IAS 37 Conor FoleyDocument9 pagesF2 Fin Acc IAS 37 Conor FoleyLove alexchelle ducutNo ratings yet

- Summary 217 229Document5 pagesSummary 217 229Love alexchelle ducutNo ratings yet

- Accounting Summay Serial BondsDocument75 pagesAccounting Summay Serial BondsLove alexchelle ducutNo ratings yet

- Accounting Exam 16 September 2018 Questions PDFDocument5 pagesAccounting Exam 16 September 2018 Questions PDFLove alexchelle ducutNo ratings yet

- Far450 Fac450Document9 pagesFar450 Fac450aielNo ratings yet

- Fra - New Format 01Document4 pagesFra - New Format 01paras pantNo ratings yet

- V & H AnalysisDocument19 pagesV & H AnalysisAslam SoniNo ratings yet

- Bank Liquidity AnalysisDocument43 pagesBank Liquidity AnalysisBaburam LamaNo ratings yet

- Comparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018Document5 pagesComparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018JonellNo ratings yet

- Financial Statements Cheat SheetDocument1 pageFinancial Statements Cheat SheetjmbaezfNo ratings yet

- Income Statement GuideDocument14 pagesIncome Statement GuideReymark TalaveraNo ratings yet

- Cash and Fund Flow Analysis and Ratio Analysis of DKSSKNDocument103 pagesCash and Fund Flow Analysis and Ratio Analysis of DKSSKNAMIT K SINGHNo ratings yet

- Study Session 8 - Long Lived Assets - 2022 - 1ADocument63 pagesStudy Session 8 - Long Lived Assets - 2022 - 1AIhuomacumehNo ratings yet

- The Effects of Financial Accounting Reporting On Managerial Decision MakingDocument95 pagesThe Effects of Financial Accounting Reporting On Managerial Decision MakingAP GREEN ENERGY CORPORATION LIMITEDNo ratings yet

- Tutorial Questions: Topic 1: Introduction To AccountingDocument28 pagesTutorial Questions: Topic 1: Introduction To AccountingBernard OwusuNo ratings yet

- Partnership and Corporation Solman 2011 Chapter 1Document7 pagesPartnership and Corporation Solman 2011 Chapter 1Reymilyn Sanchez0% (1)

- CVP Analysis and Profit Planning Problems - 0Document28 pagesCVP Analysis and Profit Planning Problems - 0lilienesieraNo ratings yet

- Income Statement Analysis 2022-2023Document4 pagesIncome Statement Analysis 2022-2023sally ngNo ratings yet

- ASSIGNMENT BBAW2103 - Financial AccountingDocument13 pagesASSIGNMENT BBAW2103 - Financial AccountingMUHAMMAD NAJIB BIN HAMBALI STUDENTNo ratings yet

- Vertical Analysis Tabung HajiDocument6 pagesVertical Analysis Tabung HajiRyuzanna JubaidiNo ratings yet

- Effective Use of Resources To Improve Business PerformanceDocument15 pagesEffective Use of Resources To Improve Business PerformancekamalhossenNo ratings yet

- Ratio analysis and budgeting for retail businessesDocument4 pagesRatio analysis and budgeting for retail businessesAsif IqbalNo ratings yet

- Profit and Loss AccountDocument2 pagesProfit and Loss AccountameliarosminiNo ratings yet

- Bcom I Fa 103 MCQSDocument11 pagesBcom I Fa 103 MCQSTushar GuptaNo ratings yet

- Problem 4-1 Multiple Choice (PAS 37)Document3 pagesProblem 4-1 Multiple Choice (PAS 37)jayNo ratings yet

- Elem Canteen-Report 22-23 Aug-NovDocument4 pagesElem Canteen-Report 22-23 Aug-NovMark Jay BongolanNo ratings yet

- Filomena Merchandising 2019 Income StatementDocument42 pagesFilomena Merchandising 2019 Income StatementABM-AKRISTINE DELA CRUZNo ratings yet

- Case StudiesDocument36 pagesCase StudiesValeria Lanata0% (1)