You might also like

- Impact of COVID-19 in Oil Industry: Dr. CA. Nabeel AhmedDocument21 pagesImpact of COVID-19 in Oil Industry: Dr. CA. Nabeel AhmedDr VerdasNo ratings yet

- February 2020 OMRDocument73 pagesFebruary 2020 OMRfahminzNo ratings yet

- Uae 2020Document8 pagesUae 2020qasimali 898No ratings yet

- Tackling The Gasoline, Middle DistillateDocument8 pagesTackling The Gasoline, Middle DistillateMón Quà Vô GiáNo ratings yet

- "Base Oil, Base Oil Everywhere, Nor Any Drop To Buy" : The Curious Case of How Coronavirus Created A Lubrication CrisisDocument9 pages"Base Oil, Base Oil Everywhere, Nor Any Drop To Buy" : The Curious Case of How Coronavirus Created A Lubrication CrisisRafael Nakazato RecioNo ratings yet

- EOR-chapter 1 (Ver 1) (5051307)Document181 pagesEOR-chapter 1 (Ver 1) (5051307)KoushikNo ratings yet

- 2020 Oil, Gas, and Chemical Industry OutlookDocument16 pages2020 Oil, Gas, and Chemical Industry OutlookmapstonegardensNo ratings yet

- 2021.Q2 Goehring & Rozencwajg Market CommentaryDocument26 pages2021.Q2 Goehring & Rozencwajg Market CommentaryAitor LongarteNo ratings yet

- Fujairah Special Report Series 2016Document41 pagesFujairah Special Report Series 2016Nicholas KoutsNo ratings yet

- The Impact of COVID On The Gulf Oil IndustryDocument4 pagesThe Impact of COVID On The Gulf Oil IndustryjosephNo ratings yet

- Using Technology To Increase Middle Distillate Production-EnglishDocument6 pagesUsing Technology To Increase Middle Distillate Production-Englishsaleh4060No ratings yet

- Oil & Gas Sector ReportDocument19 pagesOil & Gas Sector ReportSarthak ChincholikarNo ratings yet

- Tackling The Gasoline-Middle Distillate Imbalance-EnglishDocument7 pagesTackling The Gasoline-Middle Distillate Imbalance-Englishsaleh4060No ratings yet

- Oil Sector PDFDocument15 pagesOil Sector PDFRochak AgarwalNo ratings yet

- OALP Oil and Gas Wrap Up Report 2021 FinalDocument20 pagesOALP Oil and Gas Wrap Up Report 2021 FinalnganugoNo ratings yet

- Mena Gas & Petrochemicals Investment Outlook 2020-2024: October 2020Document36 pagesMena Gas & Petrochemicals Investment Outlook 2020-2024: October 2020SreekanthMylavarapu100% (2)

- Emerging From The Downturn: A New Business Environment For Refining?Document16 pagesEmerging From The Downturn: A New Business Environment For Refining?Lindsey BondNo ratings yet

- 2023.Q1 Goehring and Rozencwajg Market CommentaryDocument38 pages2023.Q1 Goehring and Rozencwajg Market CommentaryDoug MartensNo ratings yet

- Oil From A Critical Raw Material Perspective - Geological Survey of Finland (GTK) (12/22/19)Document510 pagesOil From A Critical Raw Material Perspective - Geological Survey of Finland (GTK) (12/22/19)CliffhangerNo ratings yet

- Price Forecast: Oil, Gas & ChemicalsDocument36 pagesPrice Forecast: Oil, Gas & ChemicalsDavid AlfaroNo ratings yet

- Peak Oil May Be Imminent (Reynolds 2015)Document4 pagesPeak Oil May Be Imminent (Reynolds 2015)Cliffhanger100% (1)

- WEMO Oil and Gas Insighst InfographicDocument1 pageWEMO Oil and Gas Insighst Infographicshyam swaroopNo ratings yet

- Full Potential Oil Refining in A Challenging EnvironmentDocument12 pagesFull Potential Oil Refining in A Challenging Environmentahanx9No ratings yet

- Energy: A Global Scan From Bangladesh Perspective: Mohammad TamimDocument59 pagesEnergy: A Global Scan From Bangladesh Perspective: Mohammad TamimRashidul Islam MasumNo ratings yet

- Energy Outlook 2014Document6 pagesEnergy Outlook 2014Esdras DemoroNo ratings yet

- Oil Information Overview 2020 EditionDocument33 pagesOil Information Overview 2020 EditionS. Deep DasNo ratings yet

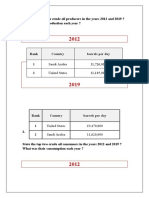

- State The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?Document6 pagesState The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?laoy aolNo ratings yet

- Upstream Services Market Overview 2008 2012Document33 pagesUpstream Services Market Overview 2008 2012Rudy Azwa ShafryNo ratings yet

- Oil Price War: Recession or Sustainability: Submitted To: DR. HIRA MUJAHIDDocument15 pagesOil Price War: Recession or Sustainability: Submitted To: DR. HIRA MUJAHIDHafiz M. UzairNo ratings yet

- Russia Ukraine War and Implications For Global Oil Markets 1682951950Document30 pagesRussia Ukraine War and Implications For Global Oil Markets 1682951950higgsboson83No ratings yet

- Oil & Gas: Difficult Times..Document4 pagesOil & Gas: Difficult Times..Arvind MeenaNo ratings yet

- Impact of COVID-19Document12 pagesImpact of COVID-19Aman Kumar JhaNo ratings yet

- Oil Market Report (июнь 2023) IEADocument47 pagesOil Market Report (июнь 2023) IEAmaryli121212No ratings yet

- Pete Conch 1Document26 pagesPete Conch 1Anonymous Ys17x7No ratings yet

- IEA WEO 2012 Summary SlidesDocument13 pagesIEA WEO 2012 Summary SlidesNikolai OudalovNo ratings yet

- EssayDocument7 pagesEssayUmair KhanNo ratings yet

- Lecture # 11 - Oil Price FormationDocument39 pagesLecture # 11 - Oil Price FormationHafiz Muhammad AkhterNo ratings yet

- India-Opec Oil TradeDocument11 pagesIndia-Opec Oil TradeHari ChandanaNo ratings yet

- Middle East TrendsDocument5 pagesMiddle East TrendsShaara NeyNo ratings yet

- Top 5 Issues For Global Oil Markets in 2020: 1. China's Instant Demand Shock: How Will The Oil Market Adjust?Document2 pagesTop 5 Issues For Global Oil Markets in 2020: 1. China's Instant Demand Shock: How Will The Oil Market Adjust?Marco PoloNo ratings yet

- Global Oil Supply: Will Mature Field Declines Drive The Next Supply Crunch?Document54 pagesGlobal Oil Supply: Will Mature Field Declines Drive The Next Supply Crunch?Maurilio BotelhoNo ratings yet

- APICORP Annual MENA Energy Investment Outlook 2022 26Document62 pagesAPICORP Annual MENA Energy Investment Outlook 2022 26Fady AhmedNo ratings yet

- UOP-Maximizing-Diesel-in-Existing-Assets-Tech-Paper3 - NPRA 2009 Dieselization Paper FinalDocument24 pagesUOP-Maximizing-Diesel-in-Existing-Assets-Tech-Paper3 - NPRA 2009 Dieselization Paper FinalsantiagoNo ratings yet

- The Light Sweet Medium Sour Crude Imbalance and The Dynamics of Price DifferentialsDocument12 pagesThe Light Sweet Medium Sour Crude Imbalance and The Dynamics of Price Differentialsmbw000012378No ratings yet

- OIL GAS ANGOLA-2021-definitiefDocument20 pagesOIL GAS ANGOLA-2021-definitiefSecretario SigmaNo ratings yet

- IATA June Global OutlookDocument23 pagesIATA June Global OutlookTim MooreNo ratings yet

- Murban A Benchmark For The Middle EastDocument19 pagesMurban A Benchmark For The Middle EastzanterNo ratings yet

- LNG Trends & Outlook Post Covid-19: Thursday, 11th June 2020Document25 pagesLNG Trends & Outlook Post Covid-19: Thursday, 11th June 2020Andrew XuguomingNo ratings yet

- 15JUNE2022 OilMarketReportDocument89 pages15JUNE2022 OilMarketReportAbhishek ChaudhariNo ratings yet

- Redefining The FutureDocument6 pagesRedefining The FutureLuis GomezNo ratings yet

- Sector Comment Oil Gas Cross Region 27may20Document5 pagesSector Comment Oil Gas Cross Region 27may20Pedro MentadoNo ratings yet

- Saudi Arabias Energy Pricing Reform in A Changing Domestic and Global ContectDocument25 pagesSaudi Arabias Energy Pricing Reform in A Changing Domestic and Global Contectمحمد التهامىNo ratings yet

- Fundamental Analysis of Crude OilDocument15 pagesFundamental Analysis of Crude Oilmoxit shahNo ratings yet

- Lithium: Demand To Double Inside A DecadeDocument31 pagesLithium: Demand To Double Inside A DecadeResearchtimeNo ratings yet

- Asia Oil CONF PDF V2Document5 pagesAsia Oil CONF PDF V2Teck HuaiNo ratings yet

- 2022 Laharrere Et Al How Much Oil RemainsDocument19 pages2022 Laharrere Et Al How Much Oil RemainsBlasNo ratings yet

- 1.november 2020 Oil Market Report PDFDocument78 pages1.november 2020 Oil Market Report PDFJuan José M RiveraNo ratings yet

- Crude Oil CommentaryDocument5 pagesCrude Oil CommentaryMphatso ManyambaNo ratings yet

- Global Oil Supply and Demand Outlook To 2040 Online SummaryDocument9 pagesGlobal Oil Supply and Demand Outlook To 2040 Online SummarysaidNo ratings yet

- The Modern Day Cult: by Antonio Panebianco, Jason Devine, Will RichardsDocument11 pagesThe Modern Day Cult: by Antonio Panebianco, Jason Devine, Will RichardsAntonio PanebiancoNo ratings yet

- Lesson 2 Arts of East AsiaDocument21 pagesLesson 2 Arts of East Asiarenaldo ocampoNo ratings yet

- Power SupplyDocument79 pagesPower SupplySharad KumbharanaNo ratings yet

- Rajiv Gandhi University of Health Sciences Exam Result: PrintDocument1 pageRajiv Gandhi University of Health Sciences Exam Result: PrintAbhi NavNo ratings yet

- EclipseDocument6 pagesEclipsetoncipNo ratings yet

- Research Argumentative EssayDocument6 pagesResearch Argumentative EssayHoney LabajoNo ratings yet

- Band Structure Engineering in Gallium Sulfde NanostructuresDocument9 pagesBand Structure Engineering in Gallium Sulfde NanostructuresucimolfettaNo ratings yet

- Agricultural Extension and CommunicationDocument173 pagesAgricultural Extension and CommunicationAlfredo Conde100% (1)

- Saberon StratMan2Document3 pagesSaberon StratMan2paredesladyheart18No ratings yet

- Beauty Therapy Thesis SampleDocument8 pagesBeauty Therapy Thesis Samplerachelvalenzuelaglendale100% (2)

- Philips Family Lamp UV CDocument4 pagesPhilips Family Lamp UV CmaterpcNo ratings yet

- Tabla QuimicaDocument12 pagesTabla QuimicaPablo PasqualiniNo ratings yet

- Lexus JTJBT20X740057503 AllSystemDTC 20230702045631Document2 pagesLexus JTJBT20X740057503 AllSystemDTC 20230702045631Venerable DezzyNo ratings yet

- R OR K C S V: EG Epair Its For Ylinder and Ervice AlvesDocument5 pagesR OR K C S V: EG Epair Its For Ylinder and Ervice AlvesLeonardoFabioCorredorNo ratings yet

- Reason: God Had Made The Mistake of Sending Only 70 PesosDocument2 pagesReason: God Had Made The Mistake of Sending Only 70 PesosS Vaibhav81% (21)

- Sarason ComplexFunctionTheory PDFDocument177 pagesSarason ComplexFunctionTheory PDFYanfan ChenNo ratings yet

- NHouse SelfBuilder Brochure v2 Jan19 LowresDocument56 pagesNHouse SelfBuilder Brochure v2 Jan19 LowresAndrew Richard ThompsonNo ratings yet

- Chapter 3 Deflection of Beams - Conjugate Beam MethodDocument6 pagesChapter 3 Deflection of Beams - Conjugate Beam MethodMbali MagagulaNo ratings yet

- Fermat Contest: Canadian Mathematics CompetitionDocument4 pagesFermat Contest: Canadian Mathematics Competitionสฮาบูดีน สาและNo ratings yet

- AP Human Geography Review Unit 2Document18 pagesAP Human Geography Review Unit 2BaselOsman50% (2)

- MicrosoftDynamicsNAVAdd OnsDocument620 pagesMicrosoftDynamicsNAVAdd OnsSadiq QudduseNo ratings yet

- Module IiDocument5 pagesModule IiFahmi PrayogiNo ratings yet

- UNDP NP Dhangadhi SWM TOR FinalDocument4 pagesUNDP NP Dhangadhi SWM TOR FinalNirmal K.c.No ratings yet

- Alzheimer's Disease Inhalational Alzheimer's Disease An UnrecognizedDocument10 pagesAlzheimer's Disease Inhalational Alzheimer's Disease An UnrecognizednikoknezNo ratings yet

- Genesis of KupferschieferDocument15 pagesGenesis of KupferschieferMaricela GarciaNo ratings yet

- Bio-Rad D-10 Dual ProgramDocument15 pagesBio-Rad D-10 Dual ProgramMeesam AliNo ratings yet

- Rolling Bearings VRMDocument2 pagesRolling Bearings VRMRollerJonnyNo ratings yet

- Podar International School (Icse) Practice Sheet STD: IX Chapter 28: Distance FormulaDocument2 pagesPodar International School (Icse) Practice Sheet STD: IX Chapter 28: Distance FormulaVanshika MehrotraNo ratings yet

- Zhou 2019 IOP Conf. Ser. Earth Environ. Sci. 252 032144Document11 pagesZhou 2019 IOP Conf. Ser. Earth Environ. Sci. 252 032144Dante FilhoNo ratings yet

- DattadasDocument4 pagesDattadasJéssica NatáliaNo ratings yet