You might also like

- How To Evaluate Private Real Estate InvestmentsDocument22 pagesHow To Evaluate Private Real Estate InvestmentsVeronica Nanco100% (4)

- Price AtionDocument247 pagesPrice Ationarvind_rathi06576989% (27)

- Stock Screener PDFDocument9 pagesStock Screener PDFClaude Bernard100% (2)

- Simple Balance Sheet For Sole Proprietorship or PartnershipDocument2 pagesSimple Balance Sheet For Sole Proprietorship or PartnershipMary86% (7)

- AccountStatement 2023 03 31Document6 pagesAccountStatement 2023 03 31STEPHEN NICHOLSONNo ratings yet

- Duddella - Stock Market PatternsDocument60 pagesDuddella - Stock Market PatternsVimal RavalNo ratings yet

- VL EXAM Set ADocument6 pagesVL EXAM Set ADavid GodiaNo ratings yet

- Review Questions - Doc - EthicsDocument35 pagesReview Questions - Doc - EthicsExam Dost100% (1)

- Assessment 1 - Accounting For Decision Makers - UWL ID 21432210Document48 pagesAssessment 1 - Accounting For Decision Makers - UWL ID 21432210Natasha de Silva100% (1)

- CUTE Exam Paper Set 1Document21 pagesCUTE Exam Paper Set 1born2pray50% (8)

- STO A Financial AnalysisDocument14 pagesSTO A Financial Analysisسنا عبداللهNo ratings yet

- Tutorial FA TOOLS WITH ANSWERDocument4 pagesTutorial FA TOOLS WITH ANSWERANIS SYAHMINo ratings yet

- Report On Profitability Ratios: Gross Profit MarginDocument8 pagesReport On Profitability Ratios: Gross Profit MarginakhilNo ratings yet

- Final Report ACC 406Document14 pagesFinal Report ACC 406Mahmud TuhinNo ratings yet

- Ultratech Cement 1. Overview of Ultratech Cement: Chart TitleDocument5 pagesUltratech Cement 1. Overview of Ultratech Cement: Chart TitleashuuuNo ratings yet

- Economic Analysis: Year 2011-2012 - 2013 - 2014 - 2015 - Compound Annual 2012 2013 2014 2015 2016 Growth Rate (CAGR) %Document4 pagesEconomic Analysis: Year 2011-2012 - 2013 - 2014 - 2015 - Compound Annual 2012 2013 2014 2015 2016 Growth Rate (CAGR) %ISHIKA MISHRA 20212622No ratings yet

- FinalReport On Financial Health of Company With Suggested Measures For Improvement NithishaDocument15 pagesFinalReport On Financial Health of Company With Suggested Measures For Improvement NithishaShiva Sai VikasNo ratings yet

- Capitaland CoDocument11 pagesCapitaland CoLucas ThuitaNo ratings yet

- Asset Management and Profitability RatioDocument3 pagesAsset Management and Profitability RatioJaneNo ratings yet

- Asset Management and Profitability RatioDocument3 pagesAsset Management and Profitability RatioJaneNo ratings yet

- Accounts PPT 12Document16 pagesAccounts PPT 12Sudhanshu PurandareNo ratings yet

- Financial RatiosDocument8 pagesFinancial Ratios21AD01 - ABISHEK JNo ratings yet

- MS7SL800 - Assignment - 1 - UniliverDocument23 pagesMS7SL800 - Assignment - 1 - UniliverDaniel AjanthanNo ratings yet

- Vadilal Industries LTD.: ContentDocument10 pagesVadilal Industries LTD.: ContentSachin NaikNo ratings yet

- Group 1 FM Cia 3Document14 pagesGroup 1 FM Cia 3ANUSHKA MAITY 2010479No ratings yet

- Analyses and Comment About The Profitability of Top GloveDocument3 pagesAnalyses and Comment About The Profitability of Top GloveAishvini ShanNo ratings yet

- FPT Fundamental of Financial Management ReportDocument29 pagesFPT Fundamental of Financial Management ReportTrần Phương Quỳnh TrangNo ratings yet

- Profitability Analysis of A Non Banking Financial Institution of BangladeshDocument27 pagesProfitability Analysis of A Non Banking Financial Institution of Bangladeshnusrat islamNo ratings yet

- Financial Management (1) (8818)Document22 pagesFinancial Management (1) (8818)georgeNo ratings yet

- ProjectDocument12 pagesProjectAamer MansoorNo ratings yet

- Attock Petroleum Limited: By: Iteqa Hameed Sidra NadeemDocument27 pagesAttock Petroleum Limited: By: Iteqa Hameed Sidra NadeemIbtisam RaiNo ratings yet

- Financial Reporting ProjectDocument11 pagesFinancial Reporting Projecttech& GamingNo ratings yet

- Print FINMAN - PrintDocument61 pagesPrint FINMAN - PrintBryan VibarNo ratings yet

- BVT Assignment MBA2019-169 Venu VedantDocument4 pagesBVT Assignment MBA2019-169 Venu VedantVenu VedantNo ratings yet

- HinoDocument14 pagesHinoOmerSyedNo ratings yet

- Profitability Ratio: Net Profit MarginDocument3 pagesProfitability Ratio: Net Profit MarginThanh Nhạn Nguyễn ThịNo ratings yet

- Document Karthi Ratio - 5 - 16.5Document10 pagesDocument Karthi Ratio - 5 - 16.5raj kumarNo ratings yet

- Acc ReportDocument24 pagesAcc ReportchavindiNo ratings yet

- Return On Assets (ROA) : ROA Is An Indicator of How Profitable A Company Is Relative To ItsDocument4 pagesReturn On Assets (ROA) : ROA Is An Indicator of How Profitable A Company Is Relative To ItsTanya RahmanNo ratings yet

- Ibn Sina Project 22Document18 pagesIbn Sina Project 22Amr ElghazalyNo ratings yet

- Vietnam Plastic Corporation: Group Assignment Principles of Accounting CLASS SE1417Document9 pagesVietnam Plastic Corporation: Group Assignment Principles of Accounting CLASS SE1417Đông AnhNo ratings yet

- Financial Ratios Financial Ratios Are Comparisons of Important Financial Data Used To Evaluate BusinessDocument12 pagesFinancial Ratios Financial Ratios Are Comparisons of Important Financial Data Used To Evaluate BusinessAaxAm KhAnNo ratings yet

- Section 3 Group 14 IocDocument5 pagesSection 3 Group 14 IocRachit Jaiswal MBA21No ratings yet

- Horizontal AnalysisDocument3 pagesHorizontal AnalysisTeofel John Alvizo Pantaleon0% (1)

- Finance Secondary MarketDocument12 pagesFinance Secondary MarketTabrej AlamNo ratings yet

- Inventories With Lower Cost, Without Sacrificing Its QualityDocument4 pagesInventories With Lower Cost, Without Sacrificing Its QualityMark Lyndon YmataNo ratings yet

- Deepinfosys LTD Pages DeletedDocument27 pagesDeepinfosys LTD Pages Deletedraimanisingh1982No ratings yet

- Financial Statement Analyses of Tata Motors LimitedDocument12 pagesFinancial Statement Analyses of Tata Motors LimitedJADUNATH HEMBRAMNo ratings yet

- Assignment 1.1: Financial ReportDocument11 pagesAssignment 1.1: Financial ReportRahul GuptaNo ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisShamim IqbalNo ratings yet

- Infosys Ratio AnalysisDocument8 pagesInfosys Ratio AnalysisRajat ChaudharyNo ratings yet

- Finance Ratios of ToyotaDocument4 pagesFinance Ratios of ToyotaMaryam KhalidNo ratings yet

- The ACME Laboratories Ltd. (ACMELAB) : Financial Statement Analysis ofDocument15 pagesThe ACME Laboratories Ltd. (ACMELAB) : Financial Statement Analysis ofHole StudioNo ratings yet

- CF K C ChandanDocument10 pagesCF K C ChandanChandan K CNo ratings yet

- K ElectricDocument9 pagesK ElectricAyesha Bareen.No ratings yet

- Fsa PresDocument5 pagesFsa PresHayab SafdarNo ratings yet

- FINANCIAL MANAGEMENT AssignmentDocument9 pagesFINANCIAL MANAGEMENT AssignmentMayank BhavsarNo ratings yet

- Operating Margin RatioDocument9 pagesOperating Margin RatiorideralfiNo ratings yet

- Corporate Finance: Topic: Company Analysis "Infosys"Document6 pagesCorporate Finance: Topic: Company Analysis "Infosys"Anuradha SinghNo ratings yet

- Ratio Analysis of Asia Pacific General Insurance Company Limited.Document18 pagesRatio Analysis of Asia Pacific General Insurance Company Limited.Harunur RashidNo ratings yet

- Financial Statement AnalysisDocument13 pagesFinancial Statement AnalysisFaiza ShaikhNo ratings yet

- Inventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andDocument23 pagesInventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andrajendranSelviNo ratings yet

- Research Project: Course: Fundamentals of FinanceDocument12 pagesResearch Project: Course: Fundamentals of FinanceAhmad SafiNo ratings yet

- Ratio AnalysisDocument5 pagesRatio AnalysisAli haiderNo ratings yet

- Ratio Analysis: Gross Profit MarginDocument9 pagesRatio Analysis: Gross Profit MarginmuhammadTzNo ratings yet

- Assignment On Financial Statement Analysis: Topic: Ratio Analysis and Interpretation ofDocument14 pagesAssignment On Financial Statement Analysis: Topic: Ratio Analysis and Interpretation ofRajashree MuktiarNo ratings yet

- Ratio AnalysisDocument4 pagesRatio AnalysisNave2n adventurism & art works.No ratings yet

- Apex Tannery Ltd. Ratio AnalysisDocument5 pagesApex Tannery Ltd. Ratio AnalysisMohammad TanveerNo ratings yet

- Step 5: Compute Net Income or Net LossDocument29 pagesStep 5: Compute Net Income or Net LossTanvir Islam100% (1)

- 1a (Macro)Document32 pages1a (Macro)Tanvir IslamNo ratings yet

- GNP and GDPDocument42 pagesGNP and GDPTanvir IslamNo ratings yet

- Macro MeasurementsDocument16 pagesMacro MeasurementsTanvir IslamNo ratings yet

- Tabular SummaryDocument16 pagesTabular SummaryTanvir IslamNo ratings yet

- 3-1 Illustration 3.25Document7 pages3-1 Illustration 3.25Tanvir IslamNo ratings yet

- Money and Banking Chapter-11Document30 pagesMoney and Banking Chapter-11Tanvir IslamNo ratings yet

- Introduction To Macroeconomics: Chapter OutlineDocument26 pagesIntroduction To Macroeconomics: Chapter OutlineTanvir IslamNo ratings yet

- Valuation of Bonds and SharesDocument42 pagesValuation of Bonds and SharesTanvir IslamNo ratings yet

- Business Law Assignment Topic: Case 1 - Tahsin Hasan Vs Bangladesh University of ProfessionalsDocument3 pagesBusiness Law Assignment Topic: Case 1 - Tahsin Hasan Vs Bangladesh University of ProfessionalsTanvir IslamNo ratings yet

- Measuring The Cost of LivingDocument41 pagesMeasuring The Cost of LivingbaoNo ratings yet

- Case Round 1 Corporiddlerz 2017 PDFDocument7 pagesCase Round 1 Corporiddlerz 2017 PDFTanvir IslamNo ratings yet

- AD and ASDocument33 pagesAD and ASTanvir IslamNo ratings yet

- Case Round 1 Corporiddlerz 2017 PDFDocument7 pagesCase Round 1 Corporiddlerz 2017 PDFTanvir IslamNo ratings yet

- CH 2Document20 pagesCH 2Tanvir IslamNo ratings yet

- (Van Horne) : The Business, Tax, and Financial EnvironmentDocument8 pages(Van Horne) : The Business, Tax, and Financial EnvironmentTanvir IslamNo ratings yet

- Business Law Assignment Topic: Case 1 - Tahsin Hasan Vs Bangladesh University of ProfessionalsDocument3 pagesBusiness Law Assignment Topic: Case 1 - Tahsin Hasan Vs Bangladesh University of ProfessionalsTanvir IslamNo ratings yet

- CH-5 VariablesDocument14 pagesCH-5 VariablesTanvir IslamNo ratings yet

- 72 - 3rd quiz-IFMDocument9 pages72 - 3rd quiz-IFMTanvir IslamNo ratings yet

- (Van Horne) : The Business, Tax, and Financial EnvironmentDocument8 pages(Van Horne) : The Business, Tax, and Financial EnvironmentTanvir IslamNo ratings yet

- Ch-4 QuestionnaireDocument18 pagesCh-4 QuestionnaireTanvir IslamNo ratings yet

- Research Methodology (2 Edition) : by Ranjit KumarDocument26 pagesResearch Methodology (2 Edition) : by Ranjit KumarTanvir Islam100% (1)

- CH 3Document15 pagesCH 3Tanvir IslamNo ratings yet

- Making Capital Investment Decision (Jordan 10) PDFDocument5 pagesMaking Capital Investment Decision (Jordan 10) PDFTanvir IslamNo ratings yet

- HameemDocument9 pagesHameemTanvir IslamNo ratings yet

- How Camping Has Changed Over The YearsDocument2 pagesHow Camping Has Changed Over The YearsTanvir IslamNo ratings yet

- Quiz 4 SolutionDocument10 pagesQuiz 4 SolutionTanvir IslamNo ratings yet

- 12 - IFM Quiz 3Document3 pages12 - IFM Quiz 3Tanvir IslamNo ratings yet

- Insurance Term Paper - 12Document1 pageInsurance Term Paper - 12Tanvir IslamNo ratings yet

- ISB Essays Pre-FinalDocument4 pagesISB Essays Pre-FinalRishabh JhunjhunwalaNo ratings yet

- Mba Syllabus, DocDocument3 pagesMba Syllabus, Docsachinkumar3009No ratings yet

- Meaning and Concept of Capital MarketDocument3 pagesMeaning and Concept of Capital Marketkhrn_himanshuNo ratings yet

- Chapter (8) : Financial Ratios Analysis: February 2019Document31 pagesChapter (8) : Financial Ratios Analysis: February 2019ALAQMARRAJNo ratings yet

- Minority InterestDocument1 pageMinority Interestankur4042007No ratings yet

- 102 QP 1003Document6 pages102 QP 1003api-3701114No ratings yet

- Ec 1745 Fall 2008 Problem Set 1Document2 pagesEc 1745 Fall 2008 Problem Set 1tarun singhNo ratings yet

- MCX Factsheet 2016Document4 pagesMCX Factsheet 2016Profit CircleNo ratings yet

- Wa0009.Document9 pagesWa0009.harkiratsinghbedi770No ratings yet

- Bhit 2022 - 06Document139 pagesBhit 2022 - 06adrian.8800No ratings yet

- ULOs Week 4 To 5Document32 pagesULOs Week 4 To 5Re MarNo ratings yet

- FinmgtDocument92 pagesFinmgtMary Elisha PinedaNo ratings yet

- Practice Questions For Final ExamDocument8 pagesPractice Questions For Final ExamChivajeetNo ratings yet

- Harbour Club ReportDocument29 pagesHarbour Club ReportEnthusiastic NoobNo ratings yet

- Project Report On Mutual FundDocument60 pagesProject Report On Mutual FundBaldeep KaurNo ratings yet

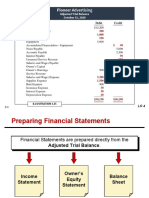

- Preparing Financial StatementsDocument15 pagesPreparing Financial StatementsAUDITOR97No ratings yet

- Study On Intrinsic Value of PseDocument84 pagesStudy On Intrinsic Value of PseApoorv MudgilNo ratings yet

- CMT Level I Sample Exam AnswersDocument14 pagesCMT Level I Sample Exam AnswersZahamish MalikNo ratings yet

- Ema Garp Fund - q2 2011 ReportDocument9 pagesEma Garp Fund - q2 2011 ReportllepardNo ratings yet

- Financial Management Paper 2.4march 2023Document17 pagesFinancial Management Paper 2.4march 2023johny SahaNo ratings yet

- Lot 38, Jalan Bunga Raya KG Lancung Jaya Shah Alam 40400: Nurul Ellisa Binti Mohd RamliDocument8 pagesLot 38, Jalan Bunga Raya KG Lancung Jaya Shah Alam 40400: Nurul Ellisa Binti Mohd Ramliellisa ramliNo ratings yet