You might also like

- Insurers Challenge of MobilityDocument8 pagesInsurers Challenge of MobilityEvaDrahosNo ratings yet

- Outsourcing Trends in Insurance IndustryDocument15 pagesOutsourcing Trends in Insurance IndustryRaviNo ratings yet

- Tomorrows Telematics For The Insurance IndustryDocument14 pagesTomorrows Telematics For The Insurance IndustryAdriana TirisNo ratings yet

- 7 Trends Transforming The Insurance Industry 062513 - v2b PDFDocument17 pages7 Trends Transforming The Insurance Industry 062513 - v2b PDFarnab.for.ever9439No ratings yet

- Digital Transformation in The Insurance IndustryDocument16 pagesDigital Transformation in The Insurance IndustryChafî Red100% (1)

- Accenture Cloud Computing Changes The GameDocument20 pagesAccenture Cloud Computing Changes The GamejonathananchenNo ratings yet

- Insurance Research ForecastDocument8 pagesInsurance Research ForecastShaarveen Raj KogularajaNo ratings yet

- Assignment 1A Final Draft Research ProposalDocument11 pagesAssignment 1A Final Draft Research ProposalAnil KumarNo ratings yet

- Financial Services Digital StrategiesDocument9 pagesFinancial Services Digital StrategiesAbdallah HaidarNo ratings yet

- Hostingcom Cloud Trends ReportDocument20 pagesHostingcom Cloud Trends ReportPrashant VashishtNo ratings yet

- Assignment: Case Studies For Telecom Business FinanceDocument11 pagesAssignment: Case Studies For Telecom Business FinancesinghrachanabaghelNo ratings yet

- The Future of Mobile Data Billing: Sponsored byDocument8 pagesThe Future of Mobile Data Billing: Sponsored byapi-192935904No ratings yet

- Machine Learning AML Report SummaryDocument10 pagesMachine Learning AML Report SummaryfhrjhaqobNo ratings yet

- The Rise of The Exponential Underwriter 1615942321Document24 pagesThe Rise of The Exponential Underwriter 1615942321Pankaj BazaariNo ratings yet

- The Journey To Understanding Your Insurance CustomersDocument17 pagesThe Journey To Understanding Your Insurance CustomersInam Ullah BukhariNo ratings yet

- Machine Learning in Uk Financial ServicesDocument41 pagesMachine Learning in Uk Financial ServicesAnno NymousNo ratings yet

- World Quality Report Consumer Products Retail and Distribution Sector Pull OutDocument4 pagesWorld Quality Report Consumer Products Retail and Distribution Sector Pull OutAnoop KumarNo ratings yet

- Fakhira Fiyanti Putri - Customer Switching Behavior Analysis in The Telecommunication IndustryDocument14 pagesFakhira Fiyanti Putri - Customer Switching Behavior Analysis in The Telecommunication IndustryFakhira Fiyanti PutriNo ratings yet

- Innovation at Progressive: Pay As You Go InsuranceDocument3 pagesInnovation at Progressive: Pay As You Go InsurancePatricia De La MotaNo ratings yet

- Sigma6 2015 enDocument43 pagesSigma6 2015 enHarry CerqueiraNo ratings yet

- Ey Cyber Strategy For InsurersDocument20 pagesEy Cyber Strategy For InsurersOrlandoNo ratings yet

- Final WorkBookDocument46 pagesFinal WorkBookajamilNo ratings yet

- Claims Classification of Insurance PoliciesDocument3 pagesClaims Classification of Insurance PoliciesHema Latha Krishna NairNo ratings yet

- From Buzz To Bucks Automotive Players On The Highway To Car Data MonetizationDocument48 pagesFrom Buzz To Bucks Automotive Players On The Highway To Car Data MonetizationAjay KathuriaNo ratings yet

- Risk ManagementDocument16 pagesRisk ManagementRahaf AlaNo ratings yet

- Accenture 2018 Compliance Risk StudyDocument12 pagesAccenture 2018 Compliance Risk StudyJOSEPHINE CUMMITINGNo ratings yet

- TELCOs Leverage Data Analytics to Stay CompetitiveDocument2 pagesTELCOs Leverage Data Analytics to Stay Competitiveanil kumarNo ratings yet

- Robotic Process Automation RPA in Insurance UiPathDocument9 pagesRobotic Process Automation RPA in Insurance UiPathsridhar_eeNo ratings yet

- PWC Study Fit For Growth Ecosystems in InsuranceDocument16 pagesPWC Study Fit For Growth Ecosystems in InsuranceFARA100% (1)

- Revenue Assurance - WikipediaDocument12 pagesRevenue Assurance - WikipediaSaurabh NolakhaNo ratings yet

- Telematics: The Game Changer: Reinventing Auto InsuranceDocument12 pagesTelematics: The Game Changer: Reinventing Auto InsuranceAdriana TirisNo ratings yet

- Chapter 4 TelkomDocument15 pagesChapter 4 TelkomZaheer HendricksNo ratings yet

- Churn Prediction in Mobile Telecom Using Data Mining TechniquesDocument5 pagesChurn Prediction in Mobile Telecom Using Data Mining TechniquesMahmoud Al-EwiwiNo ratings yet

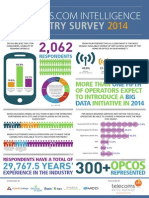

- Industry Survey: More Than of Operators Expect To Introduce A Initiative inDocument40 pagesIndustry Survey: More Than of Operators Expect To Introduce A Initiative intanveerameenNo ratings yet

- 174-White Paper Insurance Aggregator 13022014 WEBDocument15 pages174-White Paper Insurance Aggregator 13022014 WEBarnab.for.ever9439No ratings yet

- IRDA Dec 2010 Online Edition RDocument100 pagesIRDA Dec 2010 Online Edition RSatyen ShrivastavaNo ratings yet

- Project in Insurance SectorDocument51 pagesProject in Insurance Sectoryaminipawar509100% (1)

- Deloitte Uk Insurance Trends 2019 PDFDocument16 pagesDeloitte Uk Insurance Trends 2019 PDFRaghav RawatNo ratings yet

- Ebook 5 Pillars For A Connected Insurance and Modern Customer Experience FinalDocument15 pagesEbook 5 Pillars For A Connected Insurance and Modern Customer Experience FinalmetineeklaNo ratings yet

- IMAP Telematics Sector Report PDFDocument30 pagesIMAP Telematics Sector Report PDFRamon Ramirez TijerinaNo ratings yet

- EHS Safety Tech 2023 Ebook.644991ec53e19Document9 pagesEHS Safety Tech 2023 Ebook.644991ec53e19Diego MatillaNo ratings yet

- The Top Challenges of Monitoring Regulatory Risk in 2022Document21 pagesThe Top Challenges of Monitoring Regulatory Risk in 2022Businss emailNo ratings yet

- Ey Digital Transformation in InsuranceDocument18 pagesEy Digital Transformation in InsuranceSandeepPattathil100% (6)

- Stackiq Insuranceind WPP FDocument18 pagesStackiq Insuranceind WPP Fsmitanair143No ratings yet

- Journal08 - pg32-35Document4 pagesJournal08 - pg32-35hrsrinivasNo ratings yet

- Magic Quadrant For User Authentication - December 2014Document54 pagesMagic Quadrant For User Authentication - December 2014Karthik JagannathanNo ratings yet

- How Insurtech Can Close The Protection Gap in Emerging MarketsDocument8 pagesHow Insurtech Can Close The Protection Gap in Emerging MarketseugeneNo ratings yet

- A New Distribution Model: Finance On-Request InsuranceDocument8 pagesA New Distribution Model: Finance On-Request Insurancenagarajbu031No ratings yet

- Revenue Assurance For Third Party ServicesDocument8 pagesRevenue Assurance For Third Party Servicesmail2liyakhatNo ratings yet

- Gartner Market Share Analysis - Security Consulting, Worldwide, 2012Document9 pagesGartner Market Share Analysis - Security Consulting, Worldwide, 2012Othon CabreraNo ratings yet

- Using Mobile Solutions To Improve Insurance Sector PerformanceDocument16 pagesUsing Mobile Solutions To Improve Insurance Sector Performancealka_ranjan3176No ratings yet

- Dla Piper Digital Transformation in Financial ServicesDocument48 pagesDla Piper Digital Transformation in Financial Servicesapi-239489234No ratings yet

- The Shippers Guide To Transportation Management System ROI: White PaperDocument15 pagesThe Shippers Guide To Transportation Management System ROI: White PaperJoshua LimNo ratings yet

- Technology & Real EstateDocument9 pagesTechnology & Real EstateWilliamNo ratings yet

- Insurance TechnologyDocument14 pagesInsurance TechnologyYadunath SadasivaNo ratings yet

- Imap Sector Report Telematics Augist 2017Document30 pagesImap Sector Report Telematics Augist 2017Rahul VamshidharNo ratings yet

- The INSURTECH Book: The Insurance Technology Handbook for Investors, Entrepreneurs and FinTech VisionariesFrom EverandThe INSURTECH Book: The Insurance Technology Handbook for Investors, Entrepreneurs and FinTech VisionariesNo ratings yet

- Future of Vehicle InsuranceDocument10 pagesFuture of Vehicle InsuranceAdriana TirisNo ratings yet

- Future of Vehicle InsuranceDocument10 pagesFuture of Vehicle InsuranceAdriana TirisNo ratings yet

- Tomorrows Telematics For The Insurance IndustryDocument16 pagesTomorrows Telematics For The Insurance IndustryAdriana TirisNo ratings yet

- Global Insurance Telematics Free AbstractDocument63 pagesGlobal Insurance Telematics Free AbstractAdriana TirisNo ratings yet

- The Impact of Telematics on the Motor Insurance Landscape in ItalyDocument53 pagesThe Impact of Telematics on the Motor Insurance Landscape in ItalyAdriana TirisNo ratings yet

- Telematics: The Game Changer: Reinventing Auto InsuranceDocument12 pagesTelematics: The Game Changer: Reinventing Auto InsuranceAdriana TirisNo ratings yet

- Transforming The Auto Insurance Industry With Telematics WhitepaperDocument4 pagesTransforming The Auto Insurance Industry With Telematics WhitepaperAdriana TirisNo ratings yet

- Future of Vehicle InsuranceDocument10 pagesFuture of Vehicle InsuranceAdriana TirisNo ratings yet

- 737 HERE Swiss Re White Paper FinalDocument11 pages737 HERE Swiss Re White Paper Finaladriana tirisNo ratings yet

- Husnjak Perakovic Forenbacher Mumdziev20-20Procedia20Engineering202015Document8 pagesHusnjak Perakovic Forenbacher Mumdziev20-20Procedia20Engineering202015Adriana TirisNo ratings yet

- Cerere Finantare Pensiune CristinaDocument1 pageCerere Finantare Pensiune CristinaAdriana TirisNo ratings yet

- GlobalDocument38 pagesGlobalkathyboothNo ratings yet

- Improving Automobile Insurance Ratemaking Using Telematics: Incorporating Mileage and Driver Behaviour DataDocument23 pagesImproving Automobile Insurance Ratemaking Using Telematics: Incorporating Mileage and Driver Behaviour DataAdriana TirisNo ratings yet

- ND Core Competencies Early Educ Care Practitioners Revy3!17!10Document38 pagesND Core Competencies Early Educ Care Practitioners Revy3!17!10Adriana TirisNo ratings yet

- 737-HERE Swiss-Re White-Paper Final PDFDocument15 pages737-HERE Swiss-Re White-Paper Final PDFadriana tirisNo ratings yet

- Smedefinitionguide enDocument60 pagesSmedefinitionguide enJLCNo ratings yet

- ND Core Competencies Early Educ Care Practitioners Revy3!17!10Document38 pagesND Core Competencies Early Educ Care Practitioners Revy3!17!10Adriana TirisNo ratings yet

- GHIDUL SOLICITANTULUI Pentru SubMasura 7.2 Septembrie 2015Document1 pageGHIDUL SOLICITANTULUI Pentru SubMasura 7.2 Septembrie 2015Adriana TirisNo ratings yet

- Call Fiche Ict PSP Call6Document1 pageCall Fiche Ict PSP Call6Viorel RoNo ratings yet

- Support malaria control in GabonDocument67 pagesSupport malaria control in GabonAdriana TirisNo ratings yet

- Notes Marriage 2 InsyirahDocument13 pagesNotes Marriage 2 InsyirahInsyirah Mohamad NohNo ratings yet

- Comments The Best Thing About OrphanagesDocument31 pagesComments The Best Thing About OrphanagesafamailNo ratings yet

- Issue of Survival of KannadaDocument6 pagesIssue of Survival of KannadaPrashanth VaidyarajNo ratings yet

- Ra 9523Document5 pagesRa 9523diheydsNo ratings yet

- ADOPTION RULINGSDocument8 pagesADOPTION RULINGSHarold Q. GardonNo ratings yet

- Republic Act 8043 establishes Inter-Country adoption rulesDocument3 pagesRepublic Act 8043 establishes Inter-Country adoption rulesRodel Camposo100% (2)

- What Is "Forced Adoption"? (Forced Adoption Edit)Document3 pagesWhat Is "Forced Adoption"? (Forced Adoption Edit)paul robertsNo ratings yet

- Research Work 3Document4 pagesResearch Work 3Marc CosepNo ratings yet

- (Digest) Bobanovic v. MontesDocument3 pages(Digest) Bobanovic v. MontesKarla BeeNo ratings yet

- RA 8552 - Domestic Adoption ActDocument12 pagesRA 8552 - Domestic Adoption ActGerry Payno100% (1)

- Enpam Ungal ChoiceDocument15 pagesEnpam Ungal Choicekavanpt32% (22)

- MY REVIEWER IN REMEDIAL LAW - AdoptionDocument45 pagesMY REVIEWER IN REMEDIAL LAW - AdoptionGuiller MagsumbolNo ratings yet

- Equivalent citations adoption appeal judgmentDocument5 pagesEquivalent citations adoption appeal judgmentSkk IrisNo ratings yet

- Card - Against Marriage and MotherhoodDocument24 pagesCard - Against Marriage and MotherhoodJe AmaechiNo ratings yet

- Republic Act No. 10165Document7 pagesRepublic Act No. 10165sofiaqueenNo ratings yet

- Preparing YouthDocument14 pagesPreparing Youthfrancisco CarocaNo ratings yet

- Consumers ' Usage and Adoption of E-Pharmacy in India: Mallika SrivastavaDocument16 pagesConsumers ' Usage and Adoption of E-Pharmacy in India: Mallika SrivastavaSundaravel ElangovanNo ratings yet

- Eng Top On Law IIDocument84 pagesEng Top On Law IITomas BeržeckisNo ratings yet

- Meaning and Concept of AdoptionDocument13 pagesMeaning and Concept of AdoptionMAINAMPATI SATHVIK REDDYNo ratings yet

- Law On AdoptionDocument21 pagesLaw On AdoptionThu ThuNo ratings yet

- AFAADocument41 pagesAFAAVidya Prakash Cheekhorry0% (1)

- Republic Act No. 9523 - Amending RA 8552, RA 8043 and PD 603 Re - Requiring DSWD Certification As Prerequisite For AdoptionDocument5 pagesRepublic Act No. 9523 - Amending RA 8552, RA 8043 and PD 603 Re - Requiring DSWD Certification As Prerequisite For Adoptionrenzo zapantaNo ratings yet

- Barriers To Adoption of Some Agricultural Innovations in A Village in The New Valley GovernorateDocument6 pagesBarriers To Adoption of Some Agricultural Innovations in A Village in The New Valley GovernorateZaini RisaNo ratings yet

- Right to adopt not a fundamental rightDocument4 pagesRight to adopt not a fundamental rightHarsha AmmineniNo ratings yet

- Sociology Exploring The Architecture of Everyday Life Readings 10th Edition Newman Test BankDocument11 pagesSociology Exploring The Architecture of Everyday Life Readings 10th Edition Newman Test Bankdoctorsantalumu9coab100% (20)

- Midnight - Honor and ShadowDocument65 pagesMidnight - Honor and ShadowAnonymous 5Z3EMCc100% (6)

- Argumentative EssayDocument2 pagesArgumentative Essayapi-292470526No ratings yet

- A Conceptual Model For Electronic Document and Records Management System Adoption in Malaysian Public SectorDocument8 pagesA Conceptual Model For Electronic Document and Records Management System Adoption in Malaysian Public SectorAronza LeeNo ratings yet

- Robert Oscar Lopez Amicus BriefDocument42 pagesRobert Oscar Lopez Amicus BriefEquality Case Files100% (1)

- International Adoption Guide & Homestudy InfoDocument25 pagesInternational Adoption Guide & Homestudy InfosujiguruNo ratings yet