You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Jones Electrical DistributionDocument6 pagesJones Electrical DistributionLoleeta H. Khaleel67% (9)

- PNB v Sta Maria liability siblingsDocument2 pagesPNB v Sta Maria liability siblingsHariette Kim TiongsonNo ratings yet

- Financial ServicesDocument10 pagesFinancial ServicesDinesh Sugumaran100% (4)

- Philippine Housing SituationDocument1 pagePhilippine Housing SituationAaron EspirituNo ratings yet

- Introduction To Corporate Finance: Mcgraw-Hill/IrwinDocument17 pagesIntroduction To Corporate Finance: Mcgraw-Hill/IrwinchrisNo ratings yet

- PAL ActDocument8 pagesPAL ActsudumalliNo ratings yet

- Napoli PizzaDocument8 pagesNapoli PizzaPriyanka DwivediNo ratings yet

- Ioi Corporation Berhad 2015 - ArDocument280 pagesIoi Corporation Berhad 2015 - ArmohdkhidirNo ratings yet

- Kerala State Entrepreneur Development Mission (Ksedm) General Instructions Eligibility CriteriaDocument2 pagesKerala State Entrepreneur Development Mission (Ksedm) General Instructions Eligibility CriteriabinilzalkarNo ratings yet

- FM-cash FlowDocument28 pagesFM-cash FlowParamjit Sharma100% (5)

- Goldman Sachs QuestionsDocument1 pageGoldman Sachs Questionspatrick-searle-3544No ratings yet

- Contracts IIDocument8 pagesContracts IISushmaSuresh100% (1)

- Cordon vs Balicanta: Lawyer Suspended 5 Yrs for MisconductDocument5 pagesCordon vs Balicanta: Lawyer Suspended 5 Yrs for MisconductJohn Ramil RabeNo ratings yet

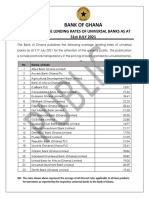

- Average Lending Rates As at July 2021Document1 pageAverage Lending Rates As at July 2021Fuaad DodooNo ratings yet

- ACI Dealing Certificate: SyllabusDocument12 pagesACI Dealing Certificate: SyllabusKhaldon AbusairNo ratings yet

- Contracts EssentialsDocument12 pagesContracts EssentialsRizza Angela MangallenoNo ratings yet

- Gullas V PNB DigestDocument2 pagesGullas V PNB DigestKareen Baucan100% (1)

- Prudence and MatchingDocument25 pagesPrudence and MatchingAbdul_Ghaffar_agkNo ratings yet

- Bank Guarantees and Trade FinanceDocument14 pagesBank Guarantees and Trade Finance1221No ratings yet

- Affordable Housing PPT 1Document66 pagesAffordable Housing PPT 1Sanjeev BumbNo ratings yet

- Essar OilsDocument1 pageEssar OilsvijaybhaskarreddymeeNo ratings yet

- Wealth DynamicsDocument32 pagesWealth Dynamicsmauve08No ratings yet

- BPI vs. Sps. SantiagoDocument3 pagesBPI vs. Sps. SantiagoAlecsandra ChuNo ratings yet

- Supreme Court Rules Ramos Must Pay Balance Despite DemandsDocument6 pagesSupreme Court Rules Ramos Must Pay Balance Despite DemandsfebwinNo ratings yet

- CFLA's Opposition To The CFPB Preliminary InjunctionDocument30 pagesCFLA's Opposition To The CFPB Preliminary InjunctionAndrew Lehman100% (1)

- BCom PDFDocument67 pagesBCom PDFSwathi Nandhagopal100% (1)

- Ancxc India Pestle AnalysisDocument15 pagesAncxc India Pestle Analysisbkaaljdaelv50% (2)

- Bernardo V MejiaDocument2 pagesBernardo V MejiaPaul VillarosaNo ratings yet

- Annuity Due and Perpetuity Sample ProblemsDocument5 pagesAnnuity Due and Perpetuity Sample ProblemsErvin Russel RoñaNo ratings yet

- AcctgDocument1 pageAcctgCherry Rago - AlajidNo ratings yet