You might also like

- OceanLink Partners Q1 2019 LetterDocument14 pagesOceanLink Partners Q1 2019 LetterKan ZhouNo ratings yet

- Maintenance Manual: Models 8300, 8400, and 8500 Pallet Trucks and Model 8600 Tow TractorDocument291 pagesMaintenance Manual: Models 8300, 8400, and 8500 Pallet Trucks and Model 8600 Tow TractorJosé Luis Ang Soto92% (13)

- 3-4 Cutting RoomDocument17 pages3-4 Cutting Roomtotol99100% (1)

- Pareto's Principle: Expand your business with the 80/20 ruleFrom EverandPareto's Principle: Expand your business with the 80/20 ruleRating: 5 out of 5 stars5/5 (1)

- TM1600 ManualDocument28 pagesTM1600 ManualedgarcooNo ratings yet

- Group-1 PPT Royal EnfieldDocument8 pagesGroup-1 PPT Royal EnfieldPuneet AgarwalNo ratings yet

- Airbus A300-600/A310 Landing Gear SystemsDocument190 pagesAirbus A300-600/A310 Landing Gear SystemsRaph 1123No ratings yet

- Aligning HR Interventions With Business StrategiesDocument14 pagesAligning HR Interventions With Business StrategiesSunielNo ratings yet

- Buisiness Marketing Project On: Avery DennisonDocument21 pagesBuisiness Marketing Project On: Avery DennisonGaurav Kumar100% (1)

- Amy RollinsonDocument51 pagesAmy RollinsonfrankyNo ratings yet

- Service Reboot: The New Science of Selling, Marketing, and Managing ServicesFrom EverandService Reboot: The New Science of Selling, Marketing, and Managing ServicesNo ratings yet

- GGGGGDocument35 pagesGGGGGMuhammad FaheemNo ratings yet

- Benchmarking AnalysisDocument9 pagesBenchmarking AnalysisMounaim 123 Hourmat AllahNo ratings yet

- HMT: Relaunch Strategy by Rohan ChackoDocument35 pagesHMT: Relaunch Strategy by Rohan Chackorohanchacko67% (3)

- Gandhinagar MarketDocument27 pagesGandhinagar Marketkrunal vaishnavNo ratings yet

- Quiz - Fintech, FMCG, ECommerceDocument341 pagesQuiz - Fintech, FMCG, ECommerceShomyo RoyNo ratings yet

- FMCGDocument59 pagesFMCGakshay yadavNo ratings yet

- FY22 Salary Increments Benchmarking StudyDocument17 pagesFY22 Salary Increments Benchmarking StudyAbhijith PrabhakarNo ratings yet

- Cottle Taylor Case AnalysisDocument18 pagesCottle Taylor Case AnalysisHEM BANSALNo ratings yet

- Summer Tranning Report ArunDocument13 pagesSummer Tranning Report ArunArun SolankiNo ratings yet

- TSMG Tata Review-June 2006Document5 pagesTSMG Tata Review-June 2006dipangshu12No ratings yet

- Bhavesh PPT SipDocument14 pagesBhavesh PPT Sipyatin rajputNo ratings yet

- FASHION MM9 (Ultimate Version)Document17 pagesFASHION MM9 (Ultimate Version)PiyushNo ratings yet

- Di Combination Graphs IDocument3 pagesDi Combination Graphs IXYZ0% (3)

- Cottle Taylor Case AnalysisDocument18 pagesCottle Taylor Case AnalysisRALLAPALLI VISHAL VIJAYNo ratings yet

- Beauty Salon Business Overview & Trends, 2012Document4 pagesBeauty Salon Business Overview & Trends, 2012dprosenjitNo ratings yet

- Market Survey of Hero Honda and Their MarketingDocument21 pagesMarket Survey of Hero Honda and Their MarketingSwastikBasuNo ratings yet

- ilide.info-chapter-6-pr_8cb6ea0de29f105dceb44e446a0410c8 (1)Document11 pagesilide.info-chapter-6-pr_8cb6ea0de29f105dceb44e446a0410c8 (1)ANH NGUYỄN LÊ NGỌCNo ratings yet

- EN - Presentation SSG 24.05Document44 pagesEN - Presentation SSG 24.05K HARIKRISHNANo ratings yet

- MSP Benchmark Survey ReportDocument19 pagesMSP Benchmark Survey Reportchrisban35No ratings yet

- 3.2 Analysis From RetailersDocument13 pages3.2 Analysis From Retailerssgsachin4No ratings yet

- ANCEBMM Auto-Care Center - Vol. III - A Survey ReportDocument61 pagesANCEBMM Auto-Care Center - Vol. III - A Survey ReportAria RosarioNo ratings yet

- Mecklai FX Risk Management Survey findingsDocument8 pagesMecklai FX Risk Management Survey findingsanandkumarnsNo ratings yet

- Research Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedDocument16 pagesResearch Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedTanu SinghNo ratings yet

- An Analysis of Micro, Small and Medium Enterprises in India.Document33 pagesAn Analysis of Micro, Small and Medium Enterprises in India.Abdul MoizzNo ratings yet

- The Rise of Indian Luxury MarketDocument31 pagesThe Rise of Indian Luxury Marketabhiabhijain3012No ratings yet

- Watch Explainer: Errors & Omissions Liability (E&O) : You Exec Makes NoDocument13 pagesWatch Explainer: Errors & Omissions Liability (E&O) : You Exec Makes NoYahya AulyaNo ratings yet

- Netherlands - SBA Fact Sheet 2019Document18 pagesNetherlands - SBA Fact Sheet 2019warda arshadNo ratings yet

- Zuriac Franchise PlanDocument17 pagesZuriac Franchise PlanManmeet SinghNo ratings yet

- TATA Hexa Case Study: Go Getters Agnimitra Banerjee (1702010) Himanshu Gupta (1702070) Himanshu Kapoor (1702071)Document13 pagesTATA Hexa Case Study: Go Getters Agnimitra Banerjee (1702010) Himanshu Gupta (1702070) Himanshu Kapoor (1702071)Himanshu GuptaNo ratings yet

- Our Marketing Team Has Carried Out Market Research To Collect Primary Data Before Launching Our Product XXXDocument6 pagesOur Marketing Team Has Carried Out Market Research To Collect Primary Data Before Launching Our Product XXXayushsoodye01No ratings yet

- L'Oreal Nederland B.V. Product: Case PresentationDocument34 pagesL'Oreal Nederland B.V. Product: Case PresentationFaizan Ul HaqNo ratings yet

- A Study On Customer Satisfaction Towards Ruler Pipes PVT LTD, AndrapradeshDocument7 pagesA Study On Customer Satisfaction Towards Ruler Pipes PVT LTD, Andrapradeshsumanth shettyNo ratings yet

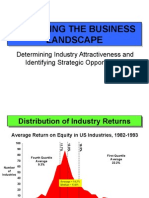

- Analyzing The Business Landscape: Determining Industry Attractiveness and Identifying Strategic OpportunitiesDocument18 pagesAnalyzing The Business Landscape: Determining Industry Attractiveness and Identifying Strategic Opportunitiesgirish8911No ratings yet

- DMART Investment Thesis - RKDocument54 pagesDMART Investment Thesis - RKRohit KadamNo ratings yet

- Problem Set - Answer KeyDocument6 pagesProblem Set - Answer KeyAlly TrizNo ratings yet

- Ashley's copy_191_Jan June WeChat Luxury IndexDocument47 pagesAshley's copy_191_Jan June WeChat Luxury IndexEric HoNo ratings yet

- CDI ASEAN-Retail May2015-EN PDFDocument4 pagesCDI ASEAN-Retail May2015-EN PDFMohd Farid Mohd NorNo ratings yet

- 2011 Economic Snapshot of The Salon IndustryDocument8 pages2011 Economic Snapshot of The Salon IndustryprobeautyassociationNo ratings yet

- Group 05 (Ad Compaign of Cola)Document9 pagesGroup 05 (Ad Compaign of Cola)vivek0020No ratings yet

- H MartDocument10 pagesH MartArya EdifyNo ratings yet

- COVID 19 Effects On MSMEs IraqDocument3 pagesCOVID 19 Effects On MSMEs IraqThanasis DimasNo ratings yet

- Business PlanDocument16 pagesBusiness PlanJewel RatillaNo ratings yet

- 763 (90) - Customer Relationship Management Pantaloons)Document96 pages763 (90) - Customer Relationship Management Pantaloons)Anagogic SapientNo ratings yet

- Assignment (BS Software Engineering) : Section Submitted To Project NameDocument9 pagesAssignment (BS Software Engineering) : Section Submitted To Project NameNajam Ul SaqibNo ratings yet

- The Rural Urban DivideDocument8 pagesThe Rural Urban DivideKomal JalanNo ratings yet

- Dealers Stock Share (0-10%) Total Number of Dealers:-106Document6 pagesDealers Stock Share (0-10%) Total Number of Dealers:-106Karan TrivediNo ratings yet

- Spain - SBA Fact Sheet 2019Document17 pagesSpain - SBA Fact Sheet 2019PNo ratings yet

- Beauty IndustryDocument10 pagesBeauty IndustryMehvish MukaddamNo ratings yet

- Final Project Report On LakmeDocument66 pagesFinal Project Report On LakmeJagdish SachdevaNo ratings yet

- Analyzing The Business LandscapeDocument18 pagesAnalyzing The Business Landscapedanic13No ratings yet

- Changing India:: A Consumer & Retail PerspectiveDocument50 pagesChanging India:: A Consumer & Retail PerspectivedhanmaliNo ratings yet

- Vibrant Gujarat: Micro Small and Medium Micro, Small and Medium Enterprises: Engine ofDocument45 pagesVibrant Gujarat: Micro Small and Medium Micro, Small and Medium Enterprises: Engine ofVandita KhudiaNo ratings yet

- Connect quality people through meaningful meetingsDocument24 pagesConnect quality people through meaningful meetingsharrysmith123No ratings yet

- Zero-Gapped: HOW TO RAISE YOUR BARBERSHOP PERFORMANCE USING TRIED AND TESTED GROWTH HACKING STRATEGIESFrom EverandZero-Gapped: HOW TO RAISE YOUR BARBERSHOP PERFORMANCE USING TRIED AND TESTED GROWTH HACKING STRATEGIESNo ratings yet

- Data Book: Automotive TechnicalDocument1 pageData Book: Automotive Technicallucian07No ratings yet

- Semiconductor Devices Are Electronic Components That Exploit The Electronic Properties of Semiconductor MaterialsDocument3 pagesSemiconductor Devices Are Electronic Components That Exploit The Electronic Properties of Semiconductor MaterialsNuwan SameeraNo ratings yet

- Machine Design ME 314 Shaft DesignDocument14 pagesMachine Design ME 314 Shaft DesignMohammed AlryaniNo ratings yet

- C - TurretDocument25 pagesC - TurretNathan BukoskiNo ratings yet

- Powercell PDX Brochure enDocument8 pagesPowercell PDX Brochure enFate Laskhar VhinrankNo ratings yet

- Training Estimator by VladarDocument10 pagesTraining Estimator by VladarMohamad SyukhairiNo ratings yet

- Srinivas ReportDocument20 pagesSrinivas ReportSrinivas B VNo ratings yet

- Tm3 Transm Receiver GuideDocument66 pagesTm3 Transm Receiver GuideAl ZanoagaNo ratings yet

- EI GAS - CompressedDocument2 pagesEI GAS - Compressedtony0% (1)

- 1800 Series Inverted Bucket Steam TrapsDocument2 pages1800 Series Inverted Bucket Steam TrapsIoana PopescuNo ratings yet

- PCBA MachineDocument62 pagesPCBA MachineSahara MalabananNo ratings yet

- DiMaggio Et Al 2001 Social Implication of The InternetDocument30 pagesDiMaggio Et Al 2001 Social Implication of The InternetDon CorneliousNo ratings yet

- Sony MP3 NWZ B143F ManualDocument82 pagesSony MP3 NWZ B143F ManualdummihaiNo ratings yet

- ExcelDocument258 pagesExcelsusi herawatiNo ratings yet

- Gpover Ip FormatDocument61 pagesGpover Ip FormatGaurav SethiNo ratings yet

- Dune Supreme/ Dune Vector: WWW - Armstrong-Ceilings - Co.Uk WWW - Armstrong-Ceilings - IeDocument2 pagesDune Supreme/ Dune Vector: WWW - Armstrong-Ceilings - Co.Uk WWW - Armstrong-Ceilings - IeMuneer KonajeNo ratings yet

- 107-b00 - Manual OperacionDocument12 pages107-b00 - Manual OperacionJuan David Triana SalazarNo ratings yet

- Cylinder Head Valve Guide and Seat Inspection and RepairDocument1 pageCylinder Head Valve Guide and Seat Inspection and Repairnetifig352No ratings yet

- H Value1Document12 pagesH Value1Sahyog KumarNo ratings yet

- 02 - MDS System and ControlDocument55 pages02 - MDS System and Controlchinith100% (1)

- TSB 18-114Document6 pagesTSB 18-114hoesy1No ratings yet

- Pundit Transducers - Operating Instructions - English - HighDocument8 pagesPundit Transducers - Operating Instructions - English - HighAayush JoshiNo ratings yet

- Analyzing Kernel Crash On Red HatDocument9 pagesAnalyzing Kernel Crash On Red Hatalexms10No ratings yet

- Portfolio - Lesson - Thinking HatsDocument2 pagesPortfolio - Lesson - Thinking Hatsapi-231993252No ratings yet

- Atheros Valkyrie BT Soc BriefDocument2 pagesAtheros Valkyrie BT Soc BriefZimmy ZizakeNo ratings yet